2722.HK Reported Results last month, holding both a conference call as well as a new product launch attended by the entire Cummins Senior Management team, including Chairman and CEO Jennifer Rumsey, highlighting the importance of CQ Cummins to the wider Cummins group:

The good:

The 2024 results were largely known, given the core earnings driver of 2722 is from CQ Cummins.

Operating income of the core Chongqing business was broadly in line with our expectations (¥44m vs. ¥37m)

However, this income included a ¥173m inventory provision, excluding which operating income would be closer to $¥200m.

As a result, operating cash flow conversion is much stronger than expected, taking the business from a net debt position of ¥269m in the half to a net cash position of over ¥1bn by the end of 2024.

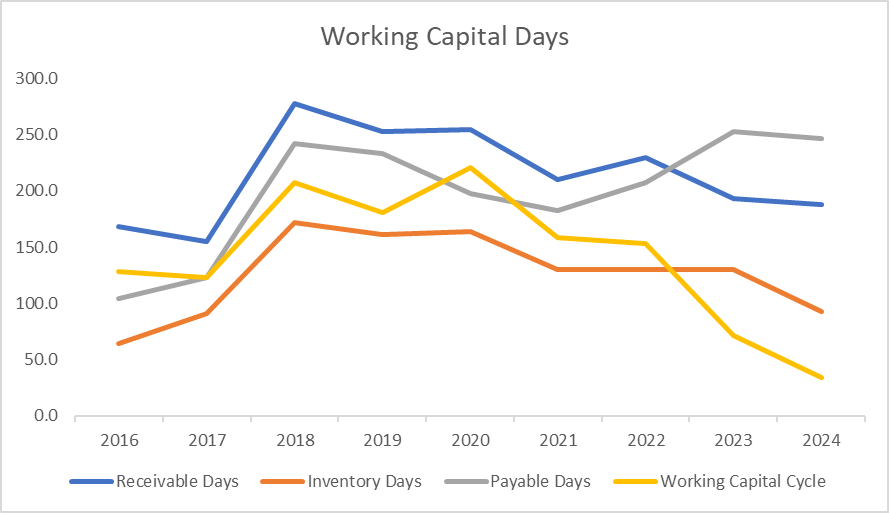

Working capital days continue to decline, setting up the business well into 2025 earnings, where management alluded to a significantly lower level of write-downs and provisioning.

For CQ Cummins, the company continues to ramp production at its new plant, with an annual production capacity of 23,000 units. This contrasts with its 2024 production of ~16,000 units, highlighting a significant volume upside opportunity.

The opportunity for growth in large domestic diesel engines remains big and will benefit all players we have covered, including CQ Cummins and CYD.

With increasing U.S. Tariffs, we have observed an increase in prices for imported engines, and as a result, the domestic industry fundamentals remain optimistic for 2025.

The interesting:

At the CQ Cummins press event, John Iain Barrowman, previously the Vice President of High Horsepower Operations of Cummins group, highlighted that CQ Cummins has the most advanced high horsepower plant of Cummins and the best engine factory in all of China.

Since Yufu has taken over 2722’s parent company, the asset manager is still working through its plans to restructure the wider group, suggesting more changes.

The not so good:

Dividend payout ratio stood at ~30%, which detracted from a more immediate stock price re-rate thesis that we were hoping for. Nevertheless, today's 6 %+ forward dividend yield remains attractive and sets a price floor for the stock.

Tencent, one of Cummins’ key partners, did not significantly increase its capex guidance for 2025 at its own 2024 full-year results, another distraction for a near-term re-rate for 2722. Nevertheless, we believe there is potential for Tencent to revise capex guidance upwards in the following months, which could result in increased demand for CQ Cummins’ products.

Final Thoughts on 2722:

Overall, the valuation of 2722 remains significantly attractive, with a strong industry backdrop and supported by a 6%+ dividend yield at the current market price.

Market Volatility

We have been taking advantage of price dislocations to rebuild positions in core businesses we like, including CYD and H22. Given the wild intra-day price swings and the industry backdrop, it should not be difficult for CYD to re-test its previous highs once the market stabilises. While we like the fundamentals of the industry and are very happy to be long volatility, equally, it should be possible for astute investors to build a profitable arbitrage strategy between the two securities and achieve significantly lower portfolio volatility.