AXT’s Tongmei Problem: Great Asset, Fragile Economics

A deep dive into one of the most controversial stocks listed on NASDAQ

Overview

For years, AXT was a sleepy compound semiconductor name. Today, investors increasingly view its Beijing Tongmei subsidiary as a scarce upstream asset in the indium phosphide value chain, with leverage to AI optics, transceivers, and eventually co-packaged optics, with the share price having increased over 3000% over the past 12 months. At the same time, short interest in the stock is near record levels. What explains this vast divergence of opinions?

A great deal of the recent enthusiasm around AXT appears to treat Tongmei as a pure strategic winner from optical demand growth. In our view, that is too simplistic. The business is not just a story about AI optics. It is also a story about transfer pricing, export permissions, capital intensity and technology diffusion.

This note provides a deep dive into Tongmei’s business model and explains why we believe the risk/reward in investing in AXTI today is heavily skewed to the downside over the medium term.

Why Tongmei Matters

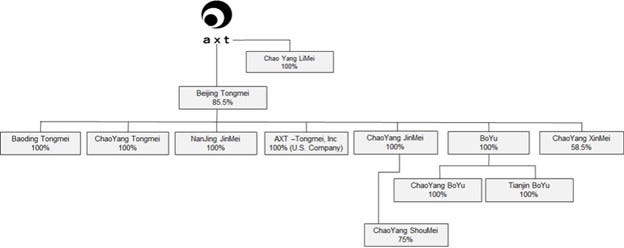

Beijing Tongmei is the crown jewel inside AXT. AXT owns 85.5% of the business, and Tongmei is the group’s key exposure to indium phosphide and other compound semiconductor substrates. At the same time, minority investors retain a put right over 7.06% of Tongmei for roughly $49 million — a detail that matters more than the market seems to appreciate if liquidity tightens or the long-delayed China IPO never reactivates.

As of March 31, 2026, the Shanghai Stock Exchange still shows Tongmei’s listing as paused, pending updated financial materials as shown below. There appears to have been no meaningful progress since 2022, with the last major filing activity dating back to July of that year. More importantly, the exchange’s earlier feedback focused on exactly the issues investors should care about today: dependence on the parent, the relatively limited size of the addressable substrate markets, and the depth of Tongmei’s underlying R&D capabilities. Each of these topics we will explore in greater detail, having analyzed thousands of pages of public Chinese regulatory documents.

Tongmei and it’s relationship with AXT

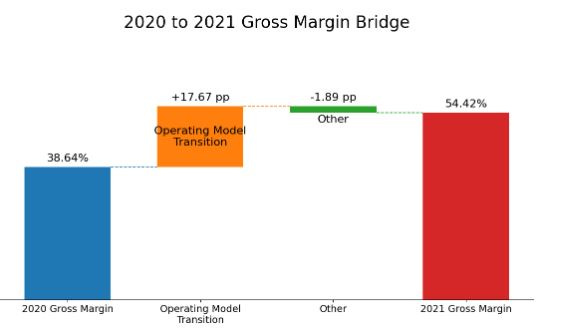

Tongmei’s 408 page prospectus1 states that the improvement in gross margin between 2020 and 2021 was materially helped by a “change in business operations,” which added 17.67 percentage points to gross margin.

In 2020, AXT created a Delaware entity called AXT-Tongmei, which was later transferred to Tongmei. From mid-2021 onward, international sales were routed through that entity. Before that, Tongmei sold products to AXT on a cost-plus basis, and AXT captured the offshore resale spread.

The prospectus makes clear how meaningful that spread was. Between 2019 and 2021, the gap between Tongmei’s transfer price and AXT’s external selling price was extremely large. In the first half of 2021 alone, AXT bought substrates from Tongmei at roughly RMB 662 per unit and resold them at about RMB 1,375.

The 2021 earnings improvement was not just the result of stronger industry conditions. It was also the result of moving the profit pool closer to Tongmei.

That distinction is fundamental because it leads to the central question of the entire valuation:

Can Tongmei continue to access offshore customers and offshore pricing at scale?

If yes, the economics may be attractive. If not, much of the current excitement becomes far harder to justify.

Tongmei’s Real Business Model: Not Just Making InP, but Monetizing Geography

At a high level, Tongmei manufactures indium phosphide substrates through a three-stage process:

polycrystalline synthesis

single-crystal growth

processing and finishing.

Step 1: Polycrystalline synthesis - raw materials are geopolitically sensitive

Polycrystalline synthesis involves combining liquid metal Indium with Phosphorus vapor to create a solid, high-purity polycrystalline ingot. While some players rely on third parties (including IQE), Tongmei is vertically integrated and can produce its own InP polycrystals.

In 2026, the acquisition of these two primary raw materials is subject to significant supply chain and geopolitical friction.

Tongmei’s upstream position benefits from China’s role in critical inputs, especially indium. China accounts for the majority of global refined indium production, giving domestic players a clear sourcing advantage over foreign competitors. We do not believe there are any significant bottlenecks in Chinese Indium refining capacity to support significantly higher levels of growing opto demand. According to USGS data2, China accounts for nearly 70% of the world’s production capacity. With the US being 100% reliant on imports.

Since February 2025, China has imposed export licensing requirements on several critical minerals, including indium. AXT itself has disclosed that Tongmei’s substrate product lines now require approval from the Ministry of Commerce before export, with recent delays affecting the business. Management has suggested approvals should be obtainable because indium phosphide is not typically viewed as a military end-market material.

In practice, export controls reflect a blend of security, industrial policy, and geopolitics. Most recently, China has imposed numerous export restrictions on refined chemicals, despite their having no military applications and an oversupplied domestic market.

That matters enormously because, as we highlighted in the previous section, Tongmei appears able to earn supernormal economics only when it can export.

Step 2: Crystal growth is important — but probably not impregnable

Polycrystals are grown into single crystals using one of several methods: The mainstream Chinese production route is Vertical Gradient Freeze, or VGF. Tongmei is currently the largest domestic operator, in part because of its yield and process know-how. But the market should be cautious about confusing current operating advantage with durable structural scarcity.

Capex for VGF expansion does not appear prohibitive. Not only has AXT highlighted a doubling of capacity this year, but domestic peers, including Yunnan Germanium (002428), are also rapidly expanding. If demand remains strong, capacity can come in faster than many investors expect, as we see no meaningful capacity constraints for domestic equipment.

That can be a dangerous setup in industrial markets. Once the industry sees high margins, incremental capital follows. The question is rarely whether capacity can expand. It is how long the margin umbrella survives after it does.

Tongmei’s know-how may still keep it ahead of local peers for some time. But history suggests that process advantages in Chinese manufacturing ecosystems do not remain exclusive forever.

In 2022, the Chinese securities regulator questioned3 why the company did not disclose that one of Tongmei’s ex-employees was being investigated in a trade secret dispute in its prospectus. This ex-employee was subsequently convicted and sentenced in June 2025.4

Concurrently, the Shanghai Stock Exchange5 questioned Tongmei’s R&D and “Know-how” capabilities, including examining the “Cross License and Payment Agreement (交叉许可和互不起诉协议)” AXT signed with a third-party “Company M,” which ends in 2029. The licensing arrangement stipulates that AXT must pay royalties to M, while M is exempt from royalties. The scope of the license covers the manufacturing, use, import, and sale of gallium arsenide and indium phosphide crystals and substrate products. Industry speculation suggests “Company M” is Sumitomo. As the current cross-license agreement is a fixed-cost cross-license and not a variable-cost cross-license that is based on revenue or units, this structure could change materially in the future, given the significant expected increase in industry size.

Step 3: Processing & Finishing:

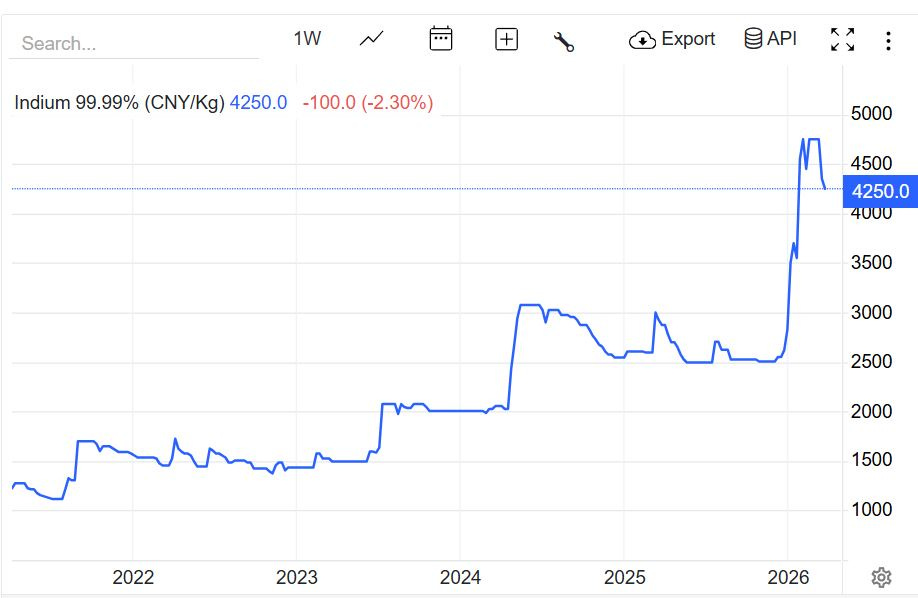

The grown crystals undergo cutting, edge grinding, lapping, polishing, and cleaning before being vacuum-packaged as finished substrates and sold to end customers. We don’t believe there are any major bottlenecks in this process. However, due to Japanese players’ current inability to source Chinese Indium under current export controls, the price of Indium and by extension InP substrates has increased significantly, with international price increases outpacing domestic price rises.

The real bottleneck is downstream, not necessarily at Tongmei

Tongmei’s substrate business sits upstream. But channel checks suggest that one of the real bottlenecks in the broader InP ecosystem is epitaxy — particularly MOCVD deposition at larger wafer sizes. That is a very different part of the value chain, and one where Aixtron remains the dominant equipment supplier with over 70% market share. Unlike VGF, there are few Chinese-equivalent tools for InP readily available; channel checks suggest Aixtron is now beginning to shift its supply chain from SiC/GaN tools to InP due to current backlog lead-time constraints.

That has two implications.

First, the industry’s ultimate growth rate may be constrained by downstream bottlenecks rather than substrate availability alone.

Second, investors may be overcapitalizing upstream substrate players while underappreciating where the hardest technical bottlenecks still sit.

Valuing Tongmei, and Why the Market May Already Be Paying for the Best-Case Outcome

The current enthusiasm around AXT increasingly resembles a capitalization of possibility rather than probability.

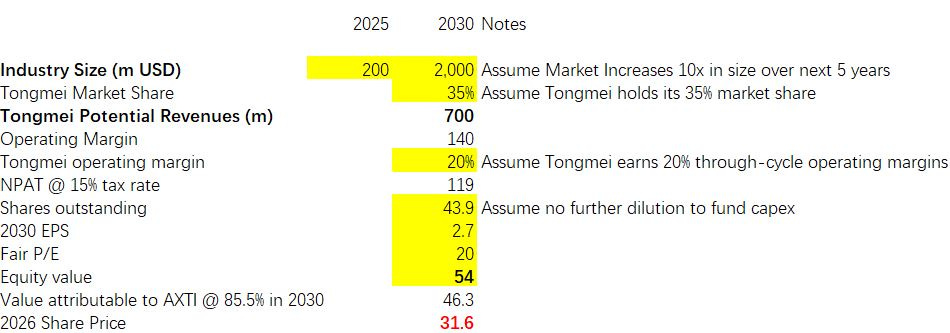

To justify a more optimistic valuation above its current share price, investors must implicitly assume more aggressive set of assumptions than below:

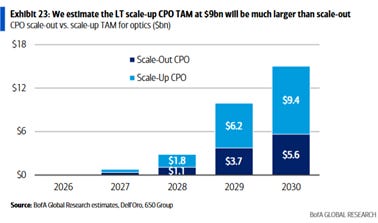

The InP substrate market is expected to expand beyond $2 billion by 2030,

Tongmei takes more market share than the current 35%

Long-run operating margins are higher than 20%

Investors are willing to ascribe a higher multiple than 20x earnings

Using this set of assumptions, one can arrive at an implied 2030 value equivalent to $45 per share (roughly the current share price)

1. The market becomes very large, very quickly

The Tongmei prospectus framed the global InP substrate market as roughly $96 million in 2020, growing towards around $200 million by 2026. Even allowing for stronger recent demand, this remains a small market today.

Sumitomo, the largest industry player with ~45% market share, provided a strategy deck in November 20256. The deck provides a good reference point for the company’s plan to increase InP substrate production capacity by 2.4x over 2023 levels by 2028.

We will make an even bolder assumption: the InP substrate market grows 10x to a $2 billion TAM by 2030. We think a $2bn InP industry TAM is more than justified, given that the entire Co-packaged optics industry (which has been the primary driver of the recent increase in share price of the sector) is only expected to reach around ~$10bn by 2030, according to the most recent analyst forecasts. As highlighted above, the InP substrate production is only the first of many stages in the production of optical solutions.

2. Tongmei keeps its current share in a much larger market

That is also not a trivial assumption, given Tongmei’s current ~35% market share.

Nvidia’s recent multi-billion-dollar investment in the optical supply chain is focused on diversifying risks away from China, not on supporting its further expansion. Recent industry actions already point in that direction, with Lumentum announcing it has expanded manufacturing of indium phosphide (InP)-based optical devices in America. The political economy of the supply chain is moving toward redundancy and regionalization.

That does not mean Tongmei loses relevance. It does mean the market should hesitate before underwriting a stable share in a 10x-larger market, as though geography were irrelevant.

3. Margins remain attractive despite expanding domestic competition

We assume Tongmei will be able to support 20% long-term operating margins. This may be the most underestimated risk. As explained in the previous section, we do not believe there are significant bottlenecks to Chinese domestic capacity expansion in single-crystal growth using the VB method, beyond industry know-how to improve yields.

When a Chinese industrial segment shows high returns and modest incremental capital requirements, new supply tends to appear quickly. Tongmei may still earn good returns. But the burden of proof should be on anyone assuming that today’s economics remain intact after multiple years of capacity growth, especially at a margin level the company has never achieved.

The financial statement below depicts a Chinese lab-grown diamond manufacturer and illustrates how a typical Chinese industrial company perform through the cycle: During the post-COVID boom, the rapid rise in popularity of lab-grown diamonds drove a significant increase in demand and wholesale prices, resulting in significant margin expansion for manufacturers. The industry expanded capacity very quickly, with very few barriers to expansion and slowing US demand, supply quickly exceeded demand, and the entire industry became unprofitable very quickly.

For Tongmei to achieve a 20% steady-state operating margin, it would likely require a scenario in which the company secures a disproportionate share of export licenses at the expense of other domestic competitors. As we highlighted previously, the current geopolitical environment for export licensing remains highly volatile and uncertain.

4. The licensing and IP environment stays supportive

Tongmei’s prospectus itself raises questions about R&D independence and references a cross-licensing arrangement with a third party, reportedly set to expire in 2029. Whether or not that becomes a direct problem, it is another reminder that Tongmei’s current position may be less self-contained than the equity story often suggests.

5. The capital structure stays clean

This is not a trivial footnote. AXT has already raised capital, Tongmei has minority put obligations, and the stalled IPO removes a potential source of balance-sheet flexibility. If capex continues to rise into 2028 and beyond, investors may discover that the path to scale is far more dilutive than the current narrative assumes.

The Right Way to Think About Tongmei

Tongmei should not be dismissed. It is clearly a real asset.

It has scale. It has customer relevance. It has a strong domestic position in a strategically important area of the semiconductor stack.

But investors should also be precise about what kind of asset this is.

Tongmei is not best understood as a pure scarcity asset where each new dollar of demand drops cleanly to the bottom line. It is better understood as a strategic industrial asset whose earnings power is highly sensitive to market structure:

whether exports remain feasible,

whether offshore pricing remains accessible,

whether domestic competition compresses returns,

whether capital requirements rise faster than expected,

and whether today’s process edge remains durable.

That makes it investable. It also makes it fragile, and at current share price levels, we do not believe investors are being fairly compensated to take on the risks.

https://static.sse.com.cn/stock/disclosure/announcement/c/202208/001065_20220801_0CSP.pdf

http://www.sdenews.com/html/2025/8/377800.shtml

https://static.sse.com.cn/stock/disclosure/announcement/c/202204/001065_20220418_IH2H.pdf