Back to The Future

Investing in China's most well funded LLM at a 93% discount to its latest round

Disclaimer: We hold a long position in 133.HK at the time of publication and may adjust our position at any time without notice. This article is for informational purposes only and does not constitute investment advice. All views expressed are the authors’ own and are based on publicly available information and fieldwork conducted by Maius Partners. We do not represent that the information is accurate or complete, and it should not be relied upon as such. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decision.

Kimi/Moonshot AI Overview:

On May 7th 2026, Moonshot AI — developer of China’s leading agentic AI model Kimi — closed a $2 billion Series D at a $20 billion valuation1, led by Meituan’s venture arm. Total cumulative funding now exceeds $4 billion, surpassing MiniMax and Zhipu AI to make Moonshot the best-funded LLM startup in China (for now).

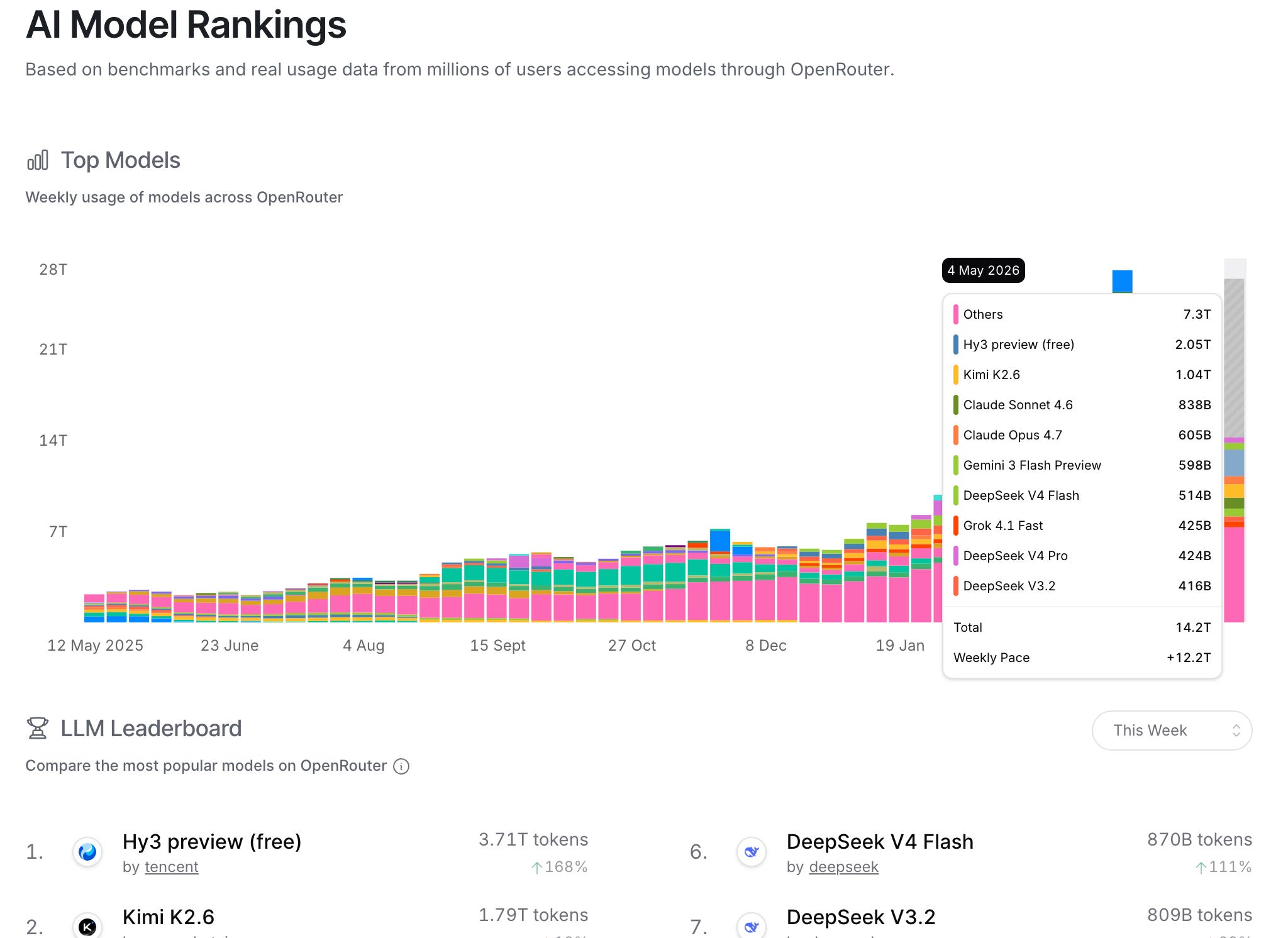

Public reports suggest Kimi’s annualized recurring revenue hit $200 million in April, doubling from $100 million just one month prior. On OpenRouter — a reasonable, if imperfect, proxy for developer adoption — Kimi’s K2.6 model has surpassed 1 trillion tokens in weekly call volume, ranking second globally across all models.

Token rankings on a routing platform don't pay the bills, so the quality and composition of Kimi's client base matter. Beyond a growing roster of Chinese enterprise customers, one of Kimi's most prominent Silicon Valley supporters is Cursor AI. Cursor's most powerful "Composer 2" model was built on top of Kimi K2.5 as its base, allowing the company to reach “frontier-level performance at a fraction of the cost of other models.”2 More recently, SpaceX reportedly acquired an option to buy Cursor for $60bn while Cursor trains its latest models on xAI’s infrastructure.3

The fact that leading American AI labs are publicly selecting a Chinese base model over every Western alternative available to them is, in our view, a meaningful commercial validation.

We also evaluated the Kimi consumer app; the attached document is a one-shot research report generated using the Kimi 2.6 Deep Research function. We believe the quality of Kimi’s output is on par, if not better than, comparable leading Western consumer app deep research output.

As a result of Kimi’s recent success, Kimi’s valuation has increased by nearly 10x over the last 2 years. But what if one could turn back time? What if one could turn back time 2 years and invest in Kimi at a $2.5 bn valuation instead?

Welcome to 2024, Marty!

The Setup: A Valuation Frozen in Time

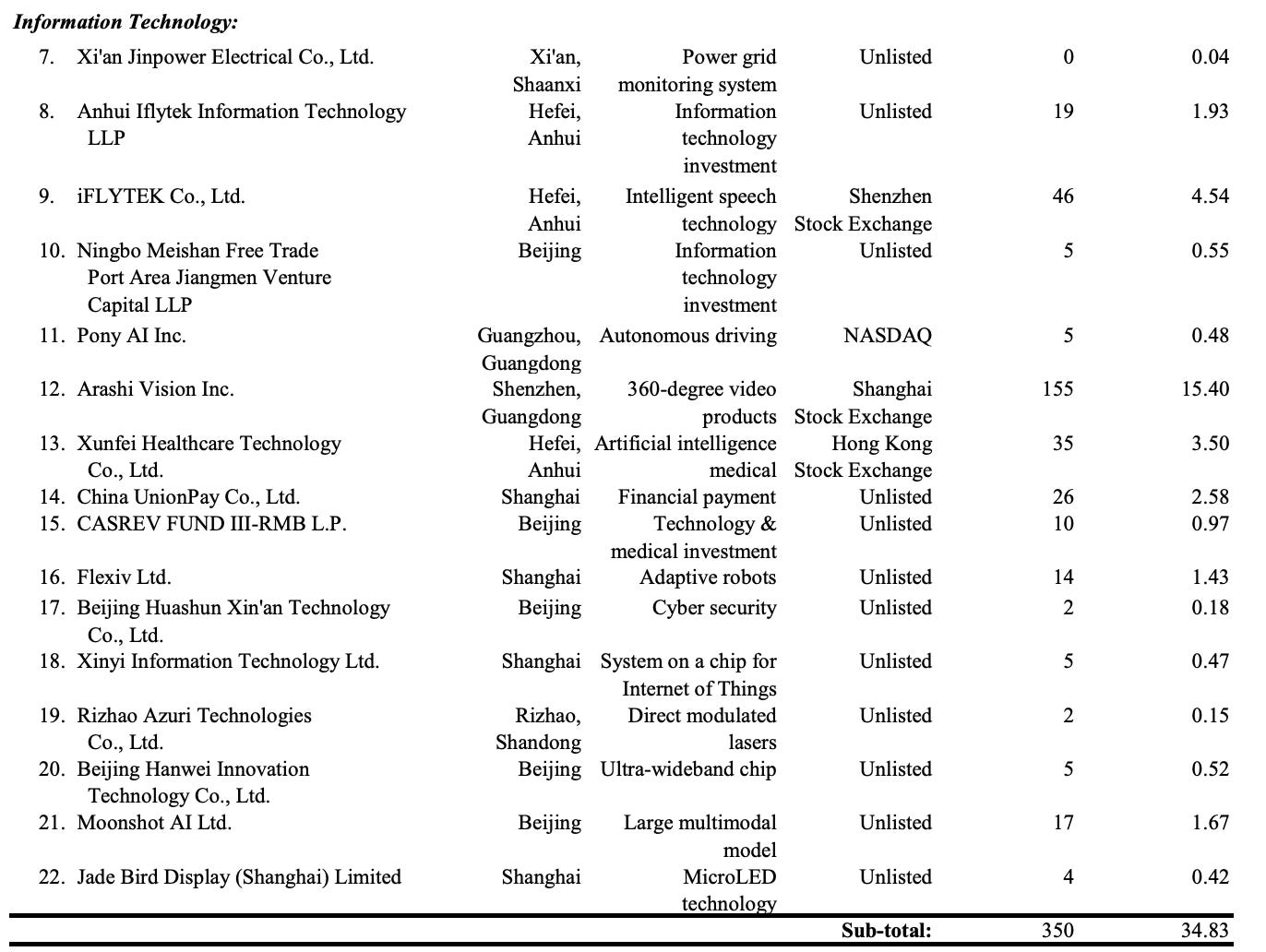

While institutional investors competed to fund Moonshot at $20bn, one of its earliest backers quietly sits on the Hong Kong Stock Exchange: China Merchants China Direct Investments (CMCDI): 133.HK.

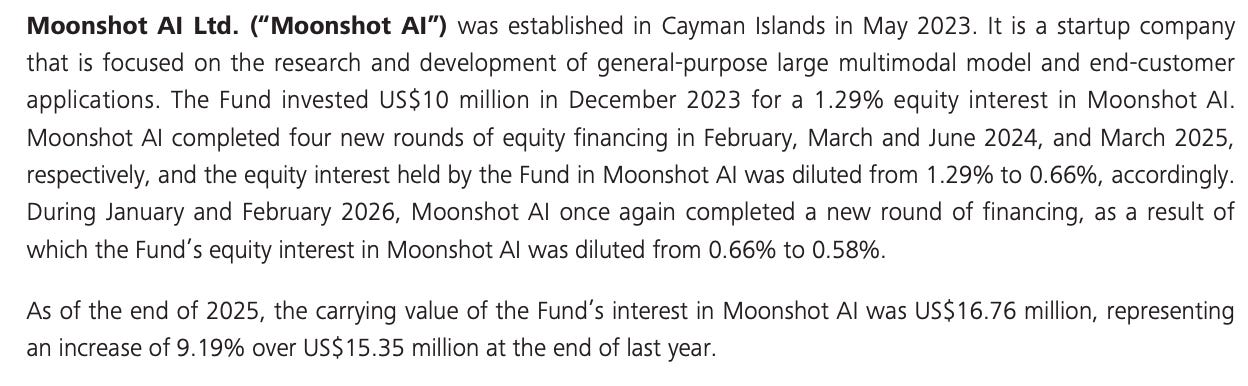

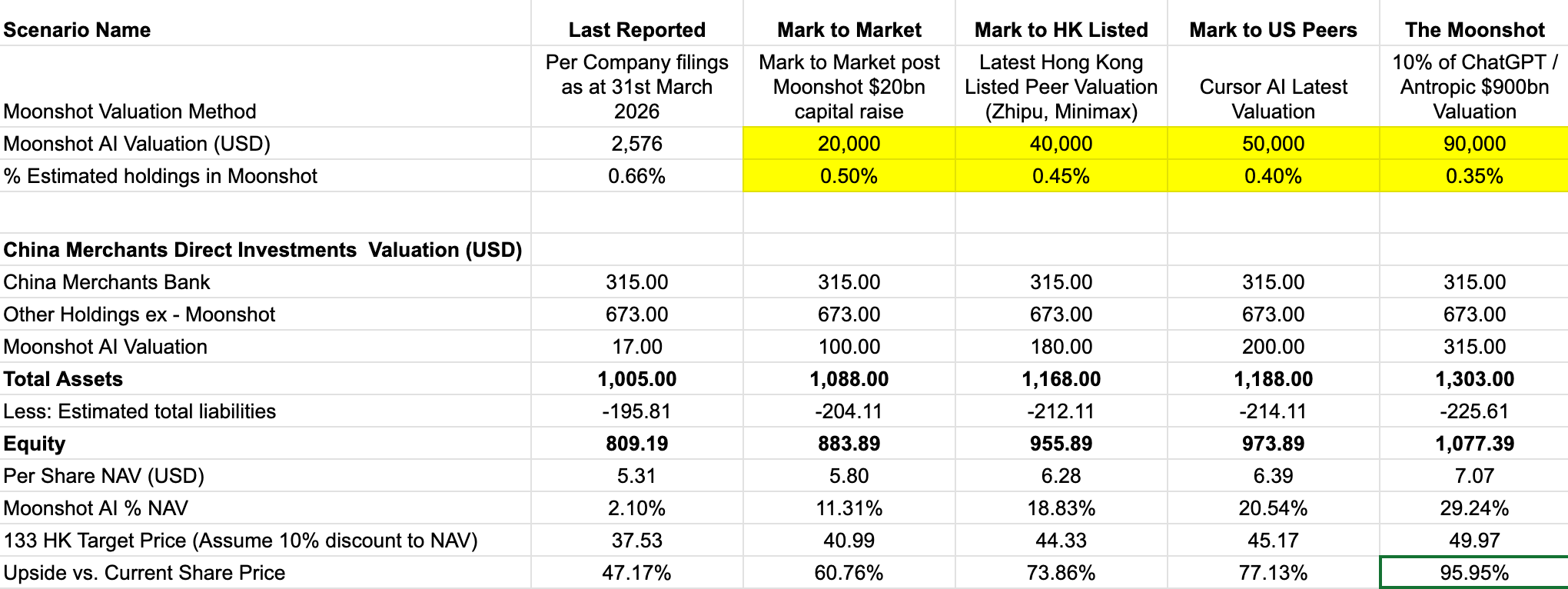

As of 31 March 2026, CMCDI’s balance sheet carries a $16.76 million book value in Moonshot AI.

Although a ~2% of NAV stake in Moonshot AI may seem insignificant, Pg 29 of CMCDI’s 2025 annual report provides more detail on exactly how this stake is valued: it is not marked to market.

As of December 31st, 2025 (and hence reported as of 31st March 2026), CMCDI’s reported $16.76m investment in Moonshot is based on a $2.5bn valuation ($16.76/0.066%) and does not reflect its more recent valuation uplift.

A mark-to-market assessment at the latest $20bn valuation would suggest that Moonshot currently accounts for over 10% of CMCDI’s NAV.

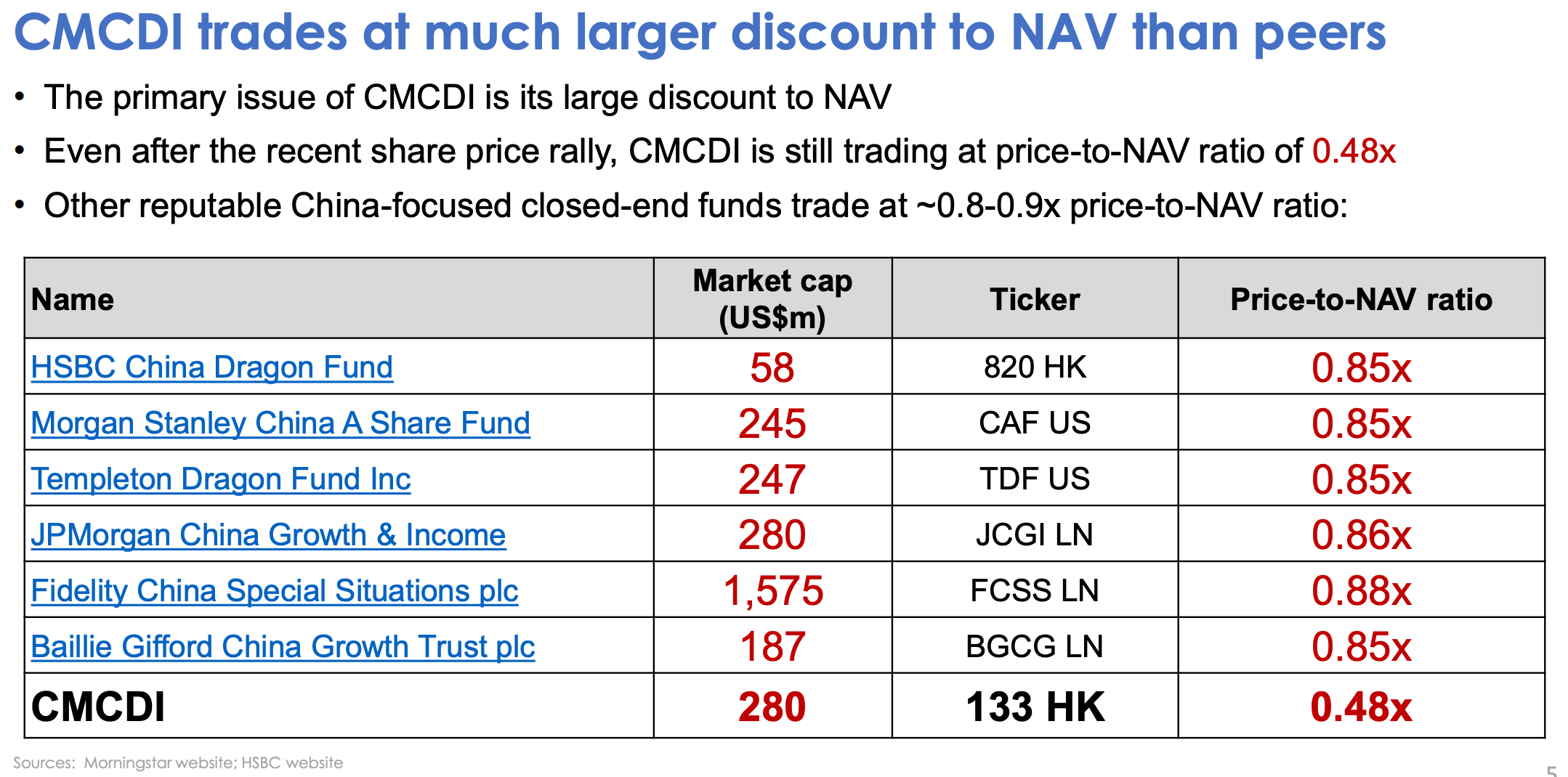

The Discount on the Discount

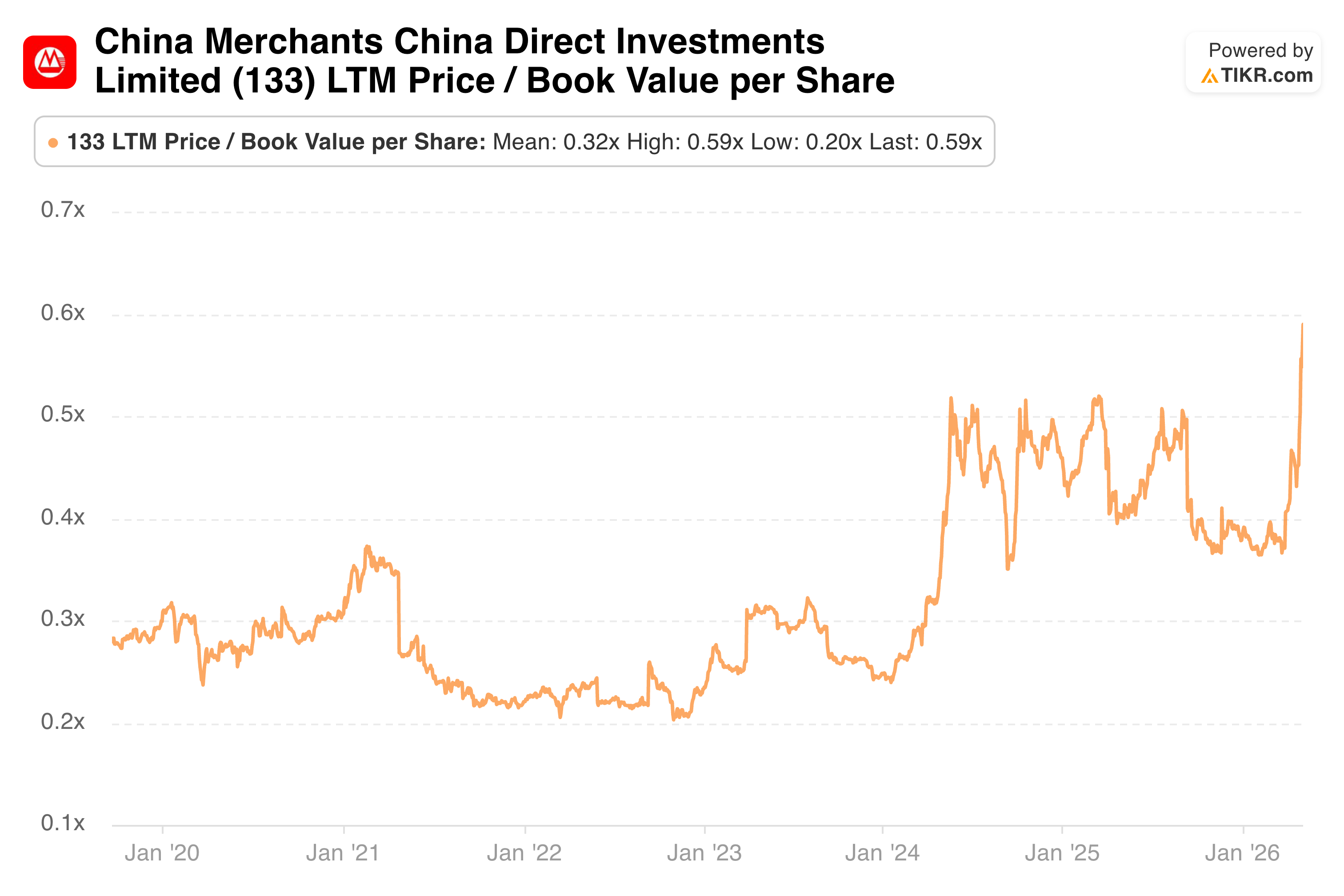

CMCDI currently trades at a significant discount to NAV, at roughly 0.6x NAV, implying that the market values CMCDI’s Moonshot EV at only $1.5bn. A 93% discount to its most recent mark.

This is heavy, Marty!

The historical bear case on CMCDI centered on governance: a captive external manager, an opaque fee structure, and limited accountability to minority shareholders. That picture has changed materially.

Following activist engagement (background here), the prior external management agreement expired. A transitional arrangement is now in place (January 2026 announcement) that explicitly ties manager economics to exit outcomes — a structure that meaningfully aligns incentives with shareholders for the first time.

As a further sign of that alignment, CMCDI recently declared a US$0.25 per share dividend, payable in July 2026, equating to a near 8% current yield at today’s price while long-term investors wait for the discount to close.

Financials:

The table below provides indicative NAV estimates under different scenarios (making reasonable assumptions about dilution and taxes), and including a blue-sky “Moonshot” scenario that could see CMCDI’s current stake in Kimi valued at over 30% of CMCDI’s NAV.

For additional context on the activist history and where the discount stands relative to peers, the prior campaign materials remain the best public reference:

Investors need not speculate about how markets value minority holdings in frontier AI models. SK Telecom — which holds a stake in Anthropic valued at $3–4 billion — has seen its market capitalization expand by over $6 billion year-to-date, as markets have begun pricing its AI exposure into the parent company. CMCDI offers a structurally similar dynamic: a listed vehicle with an understated, illiquid AI asset, trading at a discount that implies the market has not yet done the same math.

Are you ready to go back to the future, Marty? Your future is whatever you make it. So make it a good one.

https://www.scmp.com/tech/article/3352751/kimi-developer-moonshot-ai-valued-us20b-it-navigates-chinas-new-ipo-rules

https://cursor.com/blog/spacex-model-training

https://techcrunch.com/2026/04/21/spacex-is-working-with-cursor-and-has-an-option-to-buy-the-startup-for-60-billion/