CYD and H22 Results First Take:

Much Better Than the Optical Numbers Suggest, Chairman and CEO buying the dip

CYD & H22 both reported results, with both stocks taking a whacking after the monstrous run over the past few weeks, CYD closing down 15.4% and H22 declining 9% over the past 24 hours.

While we were correct to de-risk and switch from CYD to H22 ahead of results, the recent turbulence at Hong Leong’s property empire, City Developments Limited (currently in trading halt), may have contributed to idiosyncratic share price volatility for H22. We do not believe the newsflow at City Developments has any impact on the day-to-day operations for H22.

Rightfully, investors focused their attention on the outlook for the data centre business on the CYD conference call. While management didn’t delve much into financial details, their positive outlook aligns with our original thesis.

CYD’s reported FY24 revenues and earnings missed our estimate by 3% and 16% respectively, while optically disastrous, it is essential to understand the fundamental reason: CYD appears to be strategically exiting low-returning businesses and making significant write-offs during the process:

While revenue was lower than expected, gross margins were much better, with like-for-like gross margins improving 200bps in 2H, much greater than the 70bps we had expected.

Further, management took ~¥200m one-off costs above the line in 2H24, including ¥31m R&D impairment cost and ¥175m in receivable provisions, resulting in cash-costs % of revenue increasing from 6.65% in 1H to 10.77% in 2H.

As the full accounts of CYD have not been released and management didn’t delve into the details on the conference call, this analysis is based on H22’s published 2024 preliminary accounts, which are denominated in Singaporean Dollars.

Adjusting for these two above the line items, net income attributable to shareholders would be closer to ~¥430m in 2024 (vs. ¥286m in 2023), representing 50% yoy growth and a significant 12% beat vs. our original estimate of ¥386m.

Although earnings may lie, cashflow doesn’t, with the business generating significant cashflows, we estimate CYD’s operating cashflow’s increased ~40% yoy (vs. 23% eps growth) and CYD’s net cash balance increased from ¥3bn at the beginning of the year to nearly ¥4bn at the end of 2024. Unfortunately, management did not initiate any further share buyback programs.

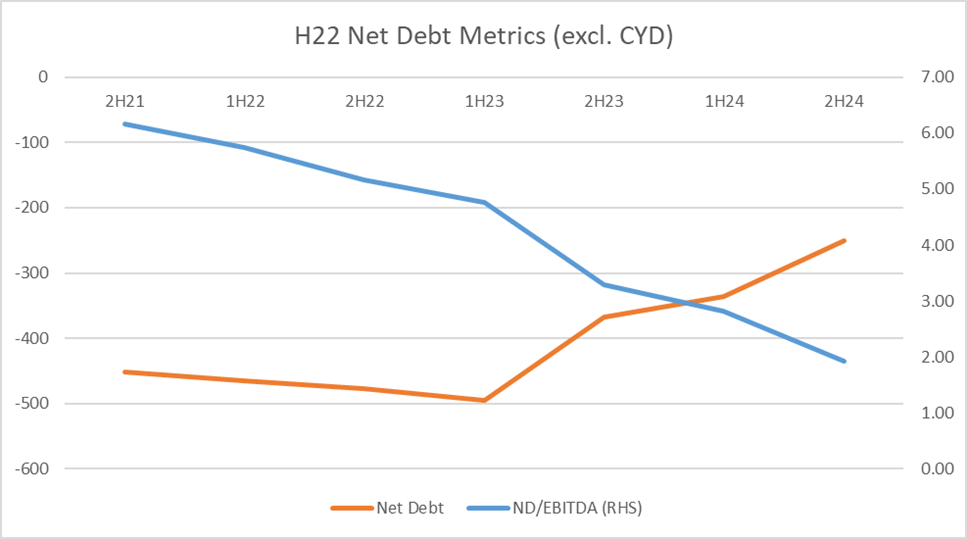

At the H22 level, building materials growth slowed into 2H, with revenues down 2.5% in the half. However, cashflow is the standout, with the company’s net debt outside of CYD decreasing from S$496m to S$250m over the past 12 months.

Given the strong cashflow generation, management declared a final dividend of 3 cents per share, taking full year dividends to 4cps and up 100% vs. 2023, representing a payout ratio of 35%.

Realistically, there is a significant opportunity to increase dividends much further (100% payout) as capex is materially lower than depreciation expense. With net leverage now below 2x at the H22 level, it is yet to be seen if the company takes a more proactive approach towards capital management.

For now, we are happy to collect the nearly 6% forward dividend yield (assuming similar 35% payout in 2025) as we wait patiently for the stock to re-rate.

Financials:

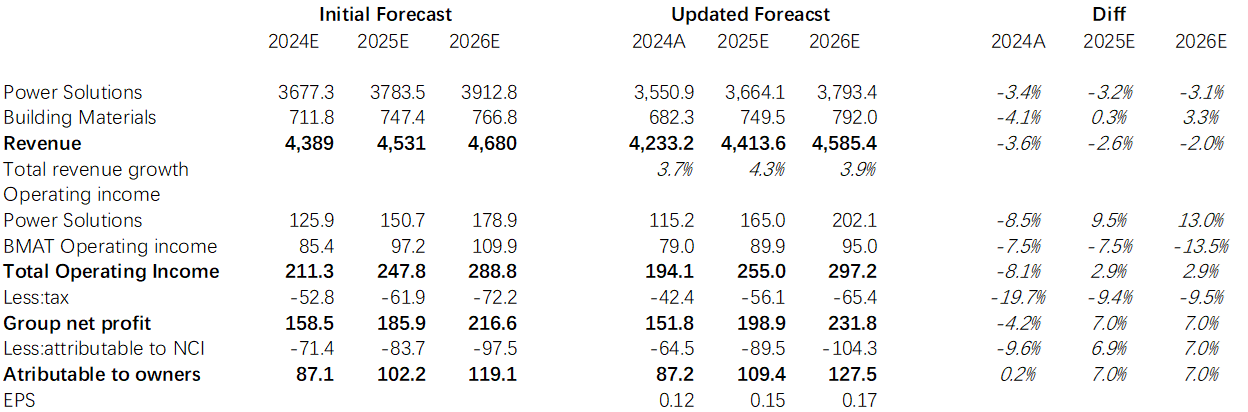

Given our understanding of the one-off costs for CYD, we have further upgraded the FY25 and FY26 numbers, as shown below, with forecasts now roughly ~20% ahead of sell-side consensus at the EPS level.

H22 P&L Estimates:

Valuation:

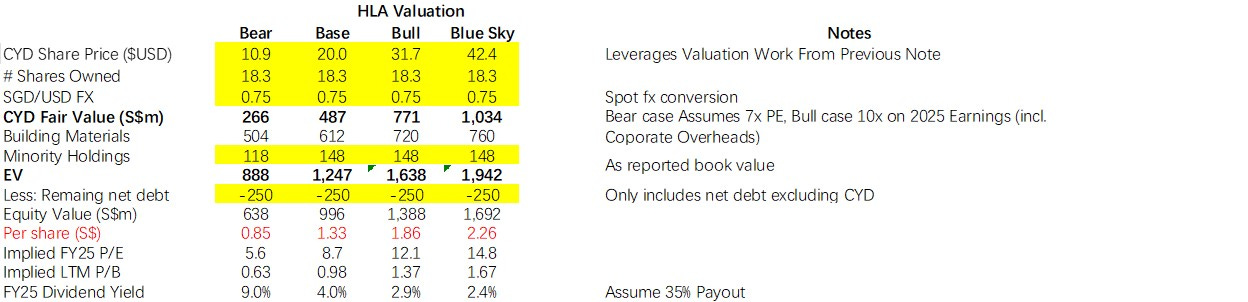

H22’s valuation remains very attractive relative to CYD, as shown in the sum of the parts analysis below, and we will continue to hold for now after switching from CYD ahead of yesterday’s result.

Update 2025/03/06:

Overall, the company’s executives appear to have agreed on our initial take on valuation assessment and over the past few days we can see a flurry of insider transaction activity, including the Chairman and CEO both materially increasing their holdings in the company.

Our channel checks suggest the industry fundamentals appear to be getting better since we published the initial take, with 2025 data center diesel engine industry shortfall projected to be larger than we had initially expected, due to strong data center capex from clients, this is driving both increasing price and longer orderbook. Further, Yuchai is also likely expanding production capacity faster than our initial forecasts.