Hong Leong Asia: Unveiling Undervalued Gems in CYD’s Parent Company

Is SGX: H22 the Better Play? Sense-checking CYD’s parent and uncovering industrial growth opportunities.

Summary

In my previous post (link), I profiled CYD. I concluded that it is likely significantly under-valued based on the future growth outlook potential, with a base-case scenario of nearly 100% upside from the data center opportunity alone. This analysis covers CYD’s parent company, Hong Leong Asia (HLA), listed on the Singapore stock exchange under H22.

The key conclusion is while HLA equally remains undervalued (+40% base case upside), it is to a lesser extent than CYD given its recent share price increase (+65% from lows vs. +35% for CYD). However, as there appears to be more liquidity on the Singapore line, H22 may be more appropriate for those looking to acquire a more meaningful position, while also benefiting from a more diverse business operation.

Corporate Overview

HLA is a subsidiary of the Hong Leong Group, a conglomerate with interests spanning financial services, manufacturing, property development, and hospitality. The Hong Leong Group was founded in 1941 by Kwek Hong Png, who immigrated to Singapore from Fujian, China, in 1928. Starting as a general trading firm dealing in ropes, paints, and ship supplies, the company expanded into various sectors over the decades.

Mr. Kwek's entrepreneurial spirit laid the foundation for the group's growth. His son, Kwek Leng Beng, currently serves as the executive chairman of the Hong Leong Group in Singapore. Under his leadership, the group has further diversified its operations and solidified its presence in multiple industries. Hong Leong Asia Ltd. (SGX: H22) operates as the group's industrial manufacturing and distribution arm, focusing on sectors such as diesel engines, building materials, and rigid packaging.

In 1993, HLA expanded into the Chinese market by acquiring a controlling stake in China Yuchai International Limited, a Bermuda-registered company listed on the New York Stock Exchange under the symbol CYD. China Yuchai, through its subsidiaries, holds a 76.4% equity interest in Guangxi Yuchai Machinery Company Limited (GYMCL), a leading engine manufacturer in China. GYMCL produces a wide range of light, medium, and heavy-duty engines for various applications, including trucks, buses, passenger vehicles, construction equipment, marine vessels, and agricultural machinery, however as mentioned in my previous report, the largest opportunity is the datacenter opportunity.

However, not everything has been perfectly smooth between HLA and Yuchai historically, as HLA held a special share that granted substantial control over Yuchai, including the authority to appoint key executives and veto shareholder resolutions. This structure led to disputes between HLA and other stakeholders within Yuchai, as HLA's control was perceived as a constraint on the company's strategic decisions.

Today, the company appears to have moved on from its previous governance issues, and there are many recent positive governance signs worth noting:

At the HLA level:

Recent insider transactions: Purchase of 145,000 shares by Mrs. Kwek in August 2024.

At the CYD level: This is discussed in more detail in my previous report

Share incentive scheme for the Data Centre business completed in June 2024

$40m buyback completed in October 2024

Activist Shareholder switching from a 13D to 13G filing

Building Products Business Overview

Outside of CYD, HLA’s primary business consists of its Building Materials division, which includes cement, pre-cast concrete products, ready-mix concrete, and quarry products that supply customers in Singapore and Malaysia. The group also owns a ~20% stake in BRC Asia, Singapore’s leading steel reinforcement solutions provider in Singapore.

Overall, construction demand in the past few years has been strong, with the Building and Construction Authority (“BCA”) projecting another robust year in construction activities for 2025 and currently expecting construction demand to rise to S$50bn in 2025, up from S$44bn in 2024, representing a 10% increase. (1)

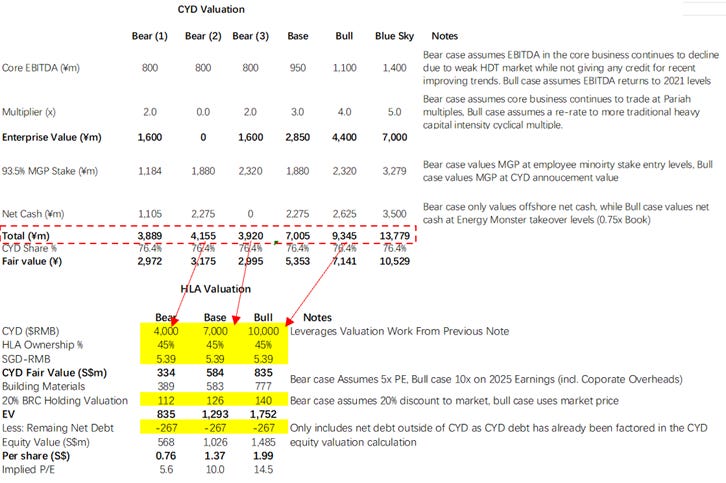

Valuations

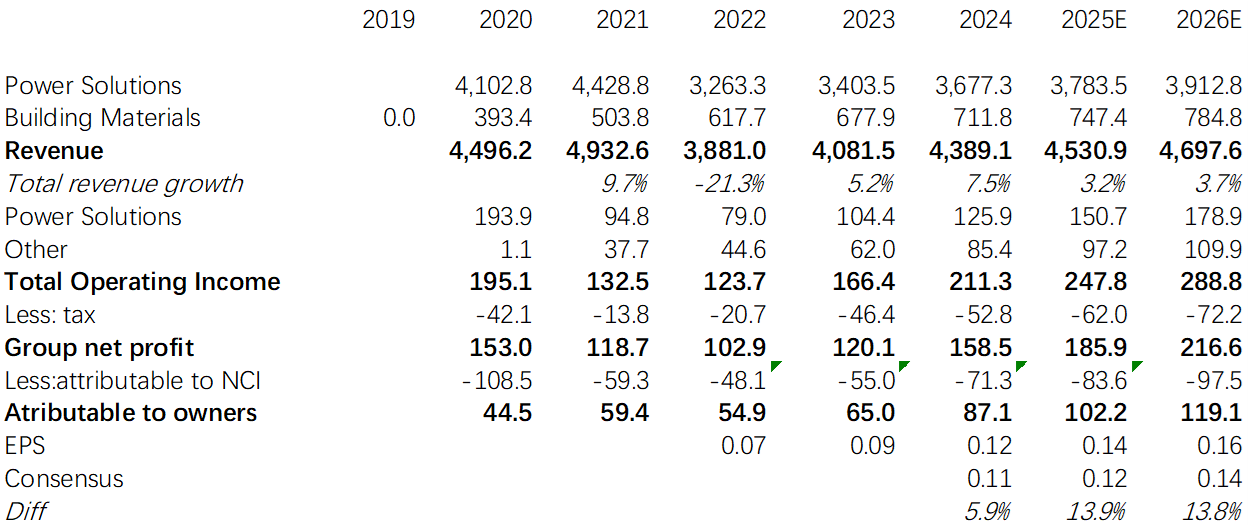

Financials

Source: