Monster in the Middle: Unpacking the High-Stakes Buyout Battle

An overview of one of the best risk-reward merger arb opportunities we currently see across the entire market

Author’s note: We initially were not planning to write this piece, as we had already flagged the opportunity on X. However, given the extremely compelling risk-adjusted opportunity set (~20% returns over a 3 to 6-month period), we would share our views in greater detail as a bonus for the influx of new subscribers.

Introduction: The Setup

The journey of Smart Share Global / Energy Monster (Nasdaq: EM 0.00%↑ ) from a celebrated market debutant to a contentious buyout target encapsulates the volatile narrative of China's sharing economy champions. In April 2021, the company, backed by heavyweights like Alibaba and SoftBank, listed on Nasdaq at $8.50 per American Depositary Share (ADS), commanding a valuation of $2.2 billion amidst investor enthusiasm. Less than four years later, with its stock languishing below $1.00, the stage was set for an opportunistic management-led buyout. This, however, is not merely another story of a fallen growth stock. It has become the arena for a proxy war over fair value, pitting insiders against a formidable, well-capitalized shareholder.

The core conflict is a study in contrasts. On one side stands an insider consortium, led by CEO Mars Cai and private equity firm Trustar Capital, with an initial offer of $1.25 per ADS—a price that appears to be a classic "take-under" designed to capitalize on a cyclical low point. On the other side is Hillhouse Capital, a sophisticated investment firm and a major shareholder, which has crashed the party with a publicly disclosed, fully funded, and 42% higher offer of $1.77 per ADS.

The central thesis of this analysis is that Hillhouse's intervention has shattered the illusion of a smooth, management-friendly privatization. It has injected genuine competition, acute legal pressure, and intense public scrutiny into what was shaping up to be an insular process. The market, while having priced in some of the potential upside, appears to underestimate still the probability of a final transaction price near or even above Hillhouse's competing bid. The investment opportunity here is not just a bet on a higher price; it is an investment in the likely breakdown of a flawed governance process under the weight of superior economics and legal force.

We believe this has created an incredibly compelling, highly asymmetric risk/reward opportunity for minority shareholders that can expect to generate ~20% returns over a 3 - 6 month period with relatively modest levels of risk.

The Engine Room: Understanding Energy Monster's Business

The Business Model at a Glance

At its core, Energy Monster, known in China as 怪兽充电, operates a ubiquitous yet straightforward service. It is one of China’s largest mobile device charging providers, with a vast network of 9.6 million rental power banks distributed across 1.28 million locations, including cafes, malls, bars, and public venues. The user proposition is straightforward: scan a QR code on one of the company's bright green cabinets to release a portable battery, use it to charge a device, and return it to any station in the network. The cost is typically around ¥3 (approximately $0.50) per half-hour.

The Great Pivot: From Blitzscaling to Survival

Energy Monster's corporate history can be divided into two distinct strategic eras, each with profound financial implications.

Initially, the company pursued a landgrab strategy built on an "asset-heavy" model. Energy Monster purchased its charging cabinets and power banks, deploying them directly into venues and sharing a portion of the rental income with the host location. This approach required significant upfront capital expenditure and high ongoing operating costs related to hardware depreciation and maintenance. However, it allowed the company to capture the largest possible share of each rental fee. This was the growth story that powered its early success and its IPO, leading to rapid revenue expansion to ¥2.8 billion by 2020 and notable profitability, including a net profit of ¥166.6 million in 2019.

Beginning in 2021-2022, the operating environment changed dramatically. The lingering effects of the pandemic reduced foot traffic, and a broader slowdown in the Chinese economy created significant headwinds and competition increased from competitors including Meituan. In response, management executed a crucial strategic pivot to an "asset-light" model. Under this new framework, third-party partners—such as vending machine operators or the venues themselves—own and deploy the charging hardware. Energy Monster's role has shifted to providing the technology platform, branding, and maintenance support in exchange for a smaller percentage of the revenue.

We believe the current business model is capable of generating around ¥ 200m EBITDA per annum with limited capex requirements; however, due to high legacy D&A costs, EM 0.00%↑ continues to be unprofitable on a statutory basis. Hillhouse highlights that “under our estimate, the Company will resume growth in 2026 and its Non-GAAP operating income will turn positive in 2027 as a result of steady operation growth”.

The Architect and The Agitator: Management, Mr. Gan, and Shareholder Alignment

The Incumbent Bidders: CEO Mars Cai and Trustar Capital

The group that initiated the go-private transaction consists of the company's founder and CEO, Mars Cai, backed by the private equity firm Trustar Capital (an affiliate of CITIC PE). Their primary incentive is clear: to acquire full control of the company at the lowest possible price. By leveraging their deep insider knowledge of the business's trough performance and their structural control over the company's voting shares, they are positioned to execute this strategy effectively. Their offer of $1.25 per ADS was likely calculated as the minimum price necessary to appear as a significant premium to a deeply depressed stock price, while remaining comfortably below their internal assessment of the company's long-term intrinsic value.

Jiawei Gan: The "Iron Man" in a Conflict

At the center of this takeover drama is Jiawei "A-Gan" Gan, a legendary figure in China's technology sector whose presence adds layers of complexity and credibility to the situation.

Mr. Gan's operational pedigree is impeccable. He was employee #67 at Alibaba, eventually rising to become the company's Sales VP. He is perhaps best known for his tenure as the Chief Operating Officer of Meituan, where, after being recruited by founder Wang Xing, he built the firm's formidable offline "iron army" of sales agents. This organization was instrumental in Meituan's victory in the "Thousand Groupons War," a brutal period of hyper-competition that saw thousands of competitors fall by the wayside. His involvement with Energy Monster—as an angel investor, advisor, and board member—lent immense credibility to the company during its IPO and signaled a focus on disciplined, ground-level execution.

The Web of Connections

Mr. Gan's alignment in the current conflict is complicated by his multiple, overlapping roles:

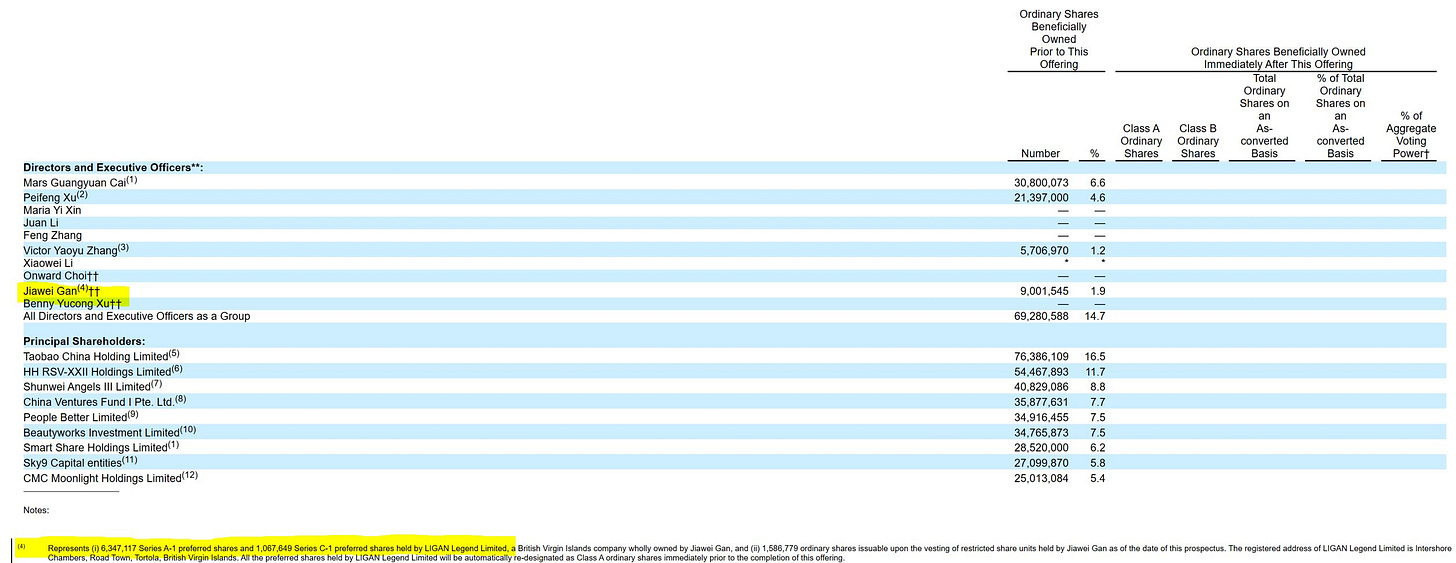

Angel Investor: He was an early, personal investor in Energy Monster through his investment vehicle, LIGAN Legend Ltd., holding roughly 1.9% of shares at the time of the IPO. This position aligns his interests with long-term value creation for all shareholders.

Source: Energy Monster 2021 Prospectus (link) Independent Director: He joined the Energy Monster board in 2021 and chairs both the compensation and nominating committees. In this capacity, his fiduciary duty is explicitly to protect the interests of all shareholders, particularly the minority investors who lack the voting power of the founders.

Hillhouse Operating Partner: His current professional affiliation is with Hillhouse Capital, the very firm that has now launched a competing, superior bid to acquire the company.

We believe, Mr. Gan's profound conflict of interest is not merely a corporate governance headache; it is the central pivot point of the entire investment thesis. His presence simultaneously validates the underlying value of the asset and exposes the flawed process that allowed the lowball bid to emerge in the first place. When the initial Trustar proposal was received, the Board formed a Special Committee of three independent directors—including Mr. Gan—to evaluate it; however, the Special Committee chose not to entertain Hillhouse when it expressed its dissatisfaction with the initial offer in a February letter addressed to the board, this suggests Mr. Gan may have been sidelined throughout the initial Special Committee review process.

However, after Hillhouse's competing bid emerged, the company announcements indicated this same committee would continue its evaluation. Placing Mr. Gan in the extraordinary and deeply conflicted position of being a committee member tasked with impartially evaluating a superior bid from his own firm. Rather than being sidelined, he is likely now at the very center of the decision-making process, creating a significant governance paradox. His fiduciary duty to all shareholders is now in direct conflict with his professional affiliation. This dynamic puts immense pressure on the other two committee members and the committee's independent advisors to ensure a fair process, as any decision they make will be scrutinized in light of Gan's presence.

The Battle Unfolds: A Timeline of the Takeover

August 1, 2025: The Opening Salvo

The takeover battle commenced when the Trustar-led consortium signed a definitive merger agreement to acquire Energy Monster for $1.25 per ADS. A critical component of their strategy was securing the support of founders and key management figures, who together controlled approximately 64% of the company's voting power through their ownership of high-vote Class B shares. This voting bloc brought them tantalizingly close to the two-thirds majority (66.7%) required for merger approval under Cayman Islands law, making the deal appear almost unstoppable from the outset.

August 13-20, 2025: Hillhouse Drops the Gauntlet

The dynamic of the deal was irrevocably altered in mid-August.

On August 13, Hillhouse Capital submitted its preliminary non-binding proposal to acquire the company for $1.77 per ADS directly to the board. The timing of this proposal is critical: Before a definitive agreement, Hillhouse is reluctant to table an offer as management could stonewall; however, by waiting until a definitive agreement is signed, the board was formally obliged to consider alternatives.

After likely receiving a tepid or non-committal response during the last few days, Hillhouse escalated its campaign. On August 20, it went public by filing a Schedule 13D. This filing disclosed its 14.4% ownership stake and, crucially, attached the full letter sent to the board (link), making the superior offer and Hillhouse's grievances known to all shareholders and the market at large. This was a deliberately aggressive and strategic move designed to force the board's hand and prevent the offer from being quietly dismissed behind closed doors.

The Governance Paradox: Gan's Enduring Role

The emergence of Hillhouse as a competing bidder created an immediate and profound conflict of interest for Jiawei Gan. However, contrary to standard governance expectations, public announcements indicate that the Special Committee—which includes Mr. Gan and was formed in January 2025—will continue to evaluate all proposals. This leaves the committee in a precarious position. The director most aligned with the superior offer from Hillhouse is not an outside agitator but an inside participant, whose every action and vote will be viewed through the lens of his dual loyalties. This unusual situation intensifies the scrutiny on the committee's process and its eventual recommendation.

The timeline of these events reveals a potential strategic miscalculation by the Trustar consortium and the Special Committee. They appear to have underestimated Hillhouse's resolve and its willingness to engage in a public fight. The Trustar group likely viewed Gan's presence on the board as a manageable issue, perhaps assuming he would object internally but would ultimately be powerless against their near-majority voting bloc. They did not seem to anticipate that his affiliation with Hillhouse would be leveraged to launch a full-fledged, public competing bid.

The Special Committee's failure to run a market check or engage with a known major shareholder like Hillhouse—which was also an early investor in the company—looks, in hindsight, either negligent or deliberately biased toward the management bid. Hillhouse's decision to go public via the 13D filing was a direct and forceful response to this insular process. They understood that a private letter could be ignored. Still, a public filing creates a legal and reputational crisis for a board of directors if they fail to engage seriously with a manifestly superior offer. The timeline shows a reactive board being forced into a corner by a proactive and legally sophisticated shareholder.

Legal Hardball: Hillhouse's Strategy and the Board's Dilemma

Hillhouse's approach extends far beyond simply offering a higher price; it is a masterclass in applying legal and procedural pressure to force a fair outcome.

The "Superior Proposal" Gambit

The letter from Hillhouse to the Energy Monster board is a piece of precise legal craftsmanship. By explicitly labeling its $1.77/ADS offer a "Superior Proposal," Hillhouse is invoking a specific legal term of art defined within the existing merger agreement with Trustar. This language triggers specific clauses that compel the Special Committee to formally evaluate the offer in good faith to determine if it meets the agreement's definition—typically an offer on terms more favorable to shareholders. A failure by the committee to conduct this evaluation properly would constitute a breach of the merger agreement itself, in addition to a violation of their broader fiduciary duties.

Weaponizing Fiduciary Duty

The letter further states that Hillhouse is "gravely concerned" that the board may disregard shareholder interests in favor of the inferior insider deal. This is a thinly veiled warning shot, laying the groundwork for future shareholder litigation. Energy Monster is incorporated in the Cayman Islands, and under Cayman law, directors have a fiduciary duty to act bona fide (in good faith) in what they believe to be the best interests of the company, which in a sale context translates to securing the best value reasonably available for shareholders. Ignoring a 42% higher, fully-funded, all-cash offer would be an almost textbook violation of this duty, exposing the directors to personal liability

The Nuclear Option: Cayman Appraisal Rights (Section 238)

This is Hillhouse's ultimate point of leverage. Should the board and the insider consortium somehow manage to force through the $1.25 deal, Hillhouse has a powerful legal remedy. With its 14.4% stake, it can formally dissent from the merger vote and then petition the Grand Court of the Cayman Islands to conduct a judicial proceeding to determine the "fair value" of its shares under Section 238 of the Cayman Islands Companies Act.

This represents a nightmare scenario for the buyer group. Cayman appraisal cases can be lengthy, expensive, and unpredictable. Crucially, in recent years, the court has shown a willingness to award fair values significantly above the merger price, especially in cases where the sale process is shown to have been flawed, non-competitive, or tainted by conflicts of interest. The mere threat of such a proceeding is a powerful deterrent. It forces the Special Committee and the Trustar group to weigh the cost of increasing their bid against the certainty of incurring massive legal fees, significant delays, and the substantial risk of a court forcing them to pay a higher price anyway.

Hillhouse is not just making a higher offer; it is systematically dismantling the legal and procedural defenses of the incumbent buyout group. The Trustar deal was built on three pillars: 1) a signed definitive agreement, 2) a nearly locked-up voting majority, 3) a compliant board. Hillhouse's "Superior Proposal" language attacks the signed agreement, using its own terms as a weapon against it. The public nature of the bid and the explicit invocation of fiduciary duties attack the notion of a compliant board, placing the directors under an intense legal and reputational microscope where simply rubber-stamping the lower deal becomes toxic. Finally, the potent threat of appraisal rights attacks the economic calculus of the voting majority, demonstrating that even if they "win" the shareholder vote, they could still lose in court. This multi-pronged legal strategy transforms the situation from a simple vote into a complex negotiation where both the board's process and the deal's ultimate price are effectively on trial.

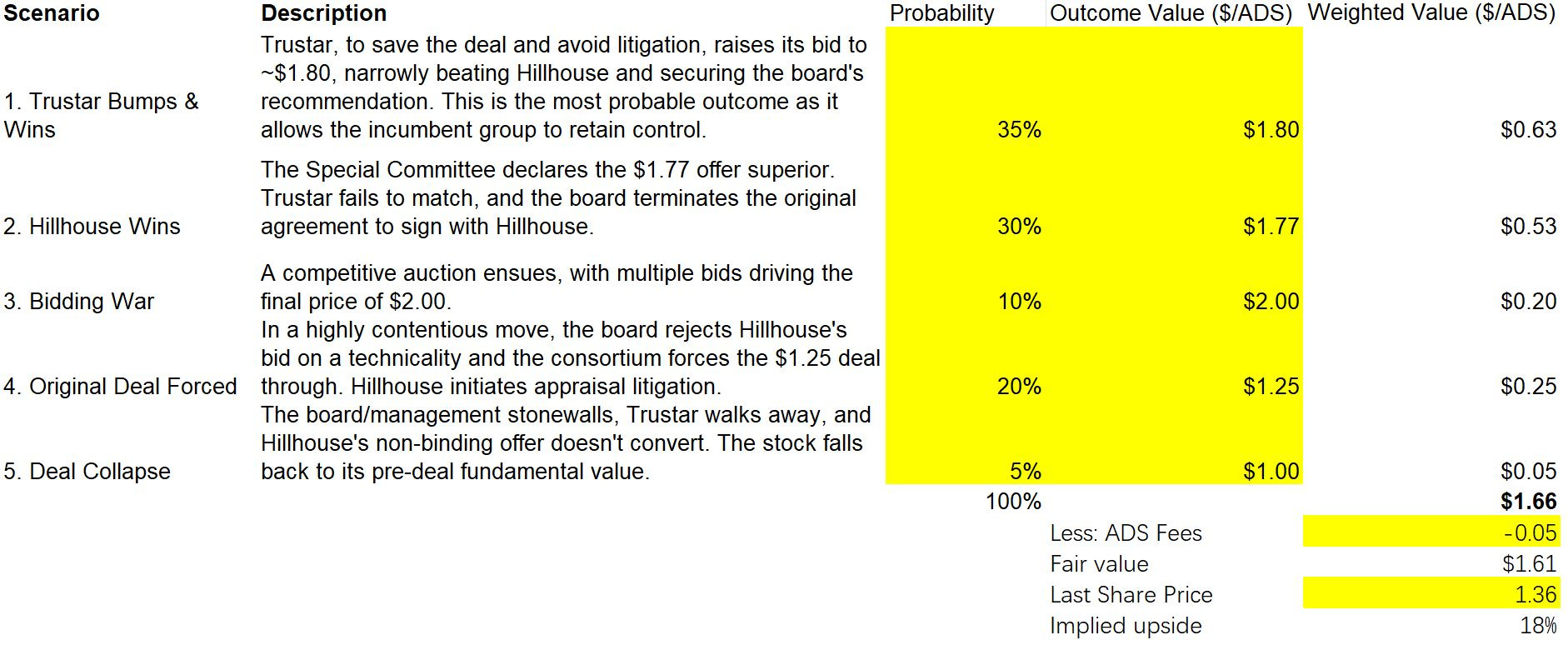

The Arbitrageur's Calculus: Scenario Analysis and Valuation

The following table synthesizes our perspective on potential outcomes, assigning subjective probabilities to each based on our qualitative and quantitative understanding of the situation.

The Bear Case: Key Risks to the Thesis

While the risk/reward profile appears highly favorable, several significant risks could derail the investment thesis.

Management Entrenchment: The most significant risk to a superior outcome is the potential for management entrenchment. CEO Mars Cai and the founding team may prefer to partner with Trustar for non-economic reasons, such as retaining greater operational control or a more favorable management equity package in the privatized entity. They could refuse to cooperate with Hillhouse—whose offer is conditional on management rollover—thus making the competing bid non-viable. They could then pressure the Special Committee to find a pretext to reject the Hillhouse offer and proceed with the original deal, leveraging their 64% voting bloc as a formidable weapon.

Deal Collapse / Stalemate: A bidding war could turn hostile, leading to a stalemate where neither party is willing to proceed. If Trustar were to terminate its agreement in frustration and Hillhouse could not secure the necessary cooperation from management to sign a new one, both deals could collapse, leaving shareholders with no M&A catalyst at all.

Any updated thoughts following the SC 13E3 filing?

thanks for sharing !

In my opinion, the stalemate/ deal collapse should probably be valued as less than you calculated.

the founder might open a similar business (that requires little capital to setup, as you mentioned) and you'd be left owning a company with a slightly more intense competition it had before Aug 1st, and with a leadership change.

still probably a good short term bet.