North American Data Centers AND Aerospace Exposure at 9x PE?

Avoiding Buffett's 'Big Mistake' while Making America Great Again

Buffett's Big Mistake

In his 2020 letter to shareholders, Warren Buffett made a rare and candid admission: he had made a "big mistake". The mistake was overpaying Precision Castparts (PCC) in 2016, a world-class manufacturer of aerospace components headquartered in Portland that Berkshire Hathaway acquired for a staggering $37 billion at 12x EBITDA. Buffett was clear: PCC was a "fine company — the best in its business," but he had been "too optimistic about PCC's normalized profit potential" and, consequently, was "wrong in my calculation of the proper price to pay".

The episode is a masterclass in one of investing's core tenets: even the best business can be a poor investment if you pay too much. The table below depicts the difference between the 2015 management internal forecasts and PCC’s actual P&L over the past decade:

But what if you could get a second chance? What if you could invest in a similar high-quality, mission-critical industrial powerhouse, but at a price that doesn't require Buffett-like optimism? What if that company was not only navigating the cyclical downturns that plagued PCC but was also pivoting to become a key supplier to the two most powerful secular growth stories of our time: the AI revolution and the aerospace supercycle?

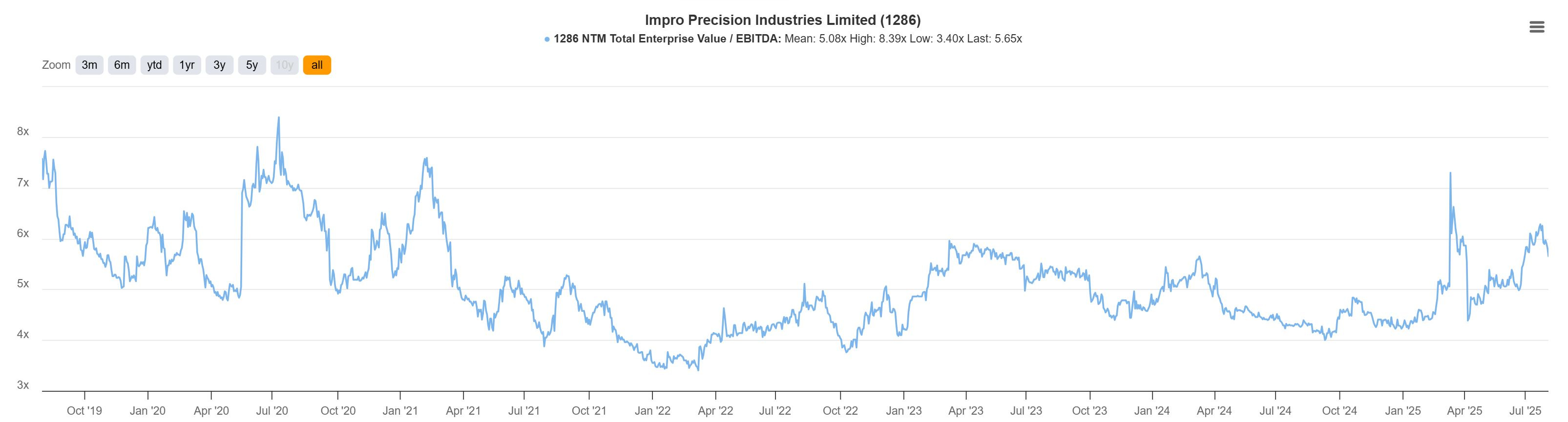

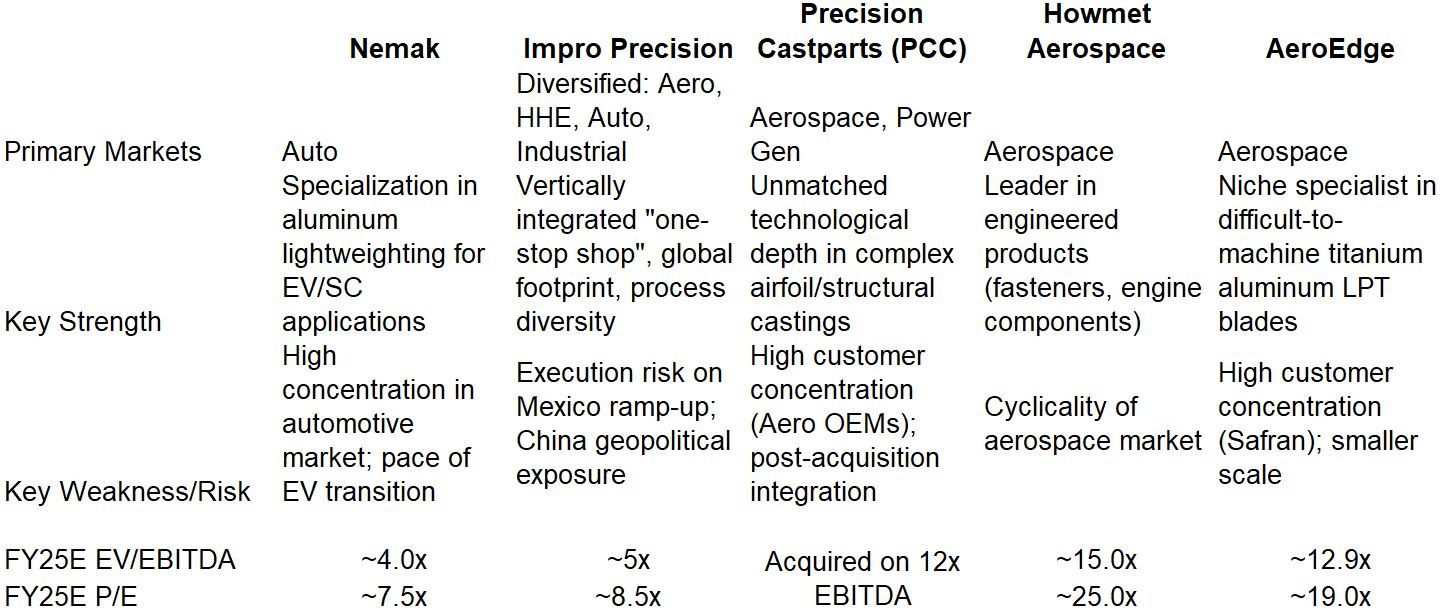

That opportunity exists today in a little-known, Hong Kong-listed company: Impro Precision Industries (1286.HK). The market is valuing Impro like a run-of-the-mill cyclical, completely missing its transformation. While Buffett paid for 12x EBITDA on peak earnings / ROIC for PCC, we believe one can currently buy Impro Precision Industries on less than 5x EBITDA on trough earnings / ROIC.

And the one person with the most information on the planet—the founder and CEO who owns ~72% of the company—is screaming that it's undervalued, deploying over HK$420 million of his cash to buy up shares on the open market (link) over the past 2 years.

The Big Picture: A Business in a Two-Speed World

At first glance, Impro looks like many other global industrial manufacturers. It's a top-10 global player in high-precision, high-complexity cast and machined components, with a diversified business spanning automotive, construction, agriculture, and more. This diversification has been a source of strength, allowing it to weather downturns in any single industry.

But look under the hood, and you'll see a company operating in a two-speed world. While its legacy markets like construction and agriculture are facing predictable cyclical headwinds—corroborated by commentary from key customers like Caterpillar —two of its segments are hitting escape velocity, powered by secular, multi-year tailwinds.

The AI Data Center Revolution (High Horsepower Engine Segment)

The Aerospace Supercycle (Aerospace Segment)

These two engines of growth are fundamentally reshaping Impro's earnings profile, making it higher quality, more predictable, and deserving of a much higher valuation multiple.

Company Overview: A Vertically Integrated, One-Stop Solution

Impro Precision is a global top-10 manufacturer of high-precision, high-complexity, and mission-critical casting and machined components. Founded in 1998, the company has evolved into a sophisticated and globally diversified industrial technology leader with an A-tier list of clients and award wins, including Caterpillar, Cummins, Honeywell Aerospace, Boeing, and Airbus (link).

The core of Impro's competitive advantage lies in its "one-stop solution" business model. Unlike smaller competitors that may specialize in a single process, Impro offers a fully integrated suite of capabilities that spans the entire production lifecycle. This includes initial research and development, tooling design and manufacturing, casting (both investment and sand), secondary precision machining, heat treatment, and surface treatment. This comprehensive offering allows Impro to deliver fully finished, ready-to-use products directly to its customers' assembly lines. This integration simplifies the supply chain for its clients, reduces logistical complexity, ensures quality control across the entire process, and ultimately creates a much stickier, long-term partnership that is difficult for competitors to displace.

The foundation of Impro's global competitive advantage lies in its extensive and highly advanced operations in China. The company is a dominant force in the industry, recognized as the world's fifth-largest independent investment casting manufacturer and the largest in China. We believe this offers a unique set of cost advantages versus many of Impro’s key international competitors, which historically are German-based. Faced with declining demand for European automobiles, combined with high labour and energy costs (typically 30-40% COGS), key competitors including Gienanth, have gone bankrupt, directly resulting in increasing orders to Impro.

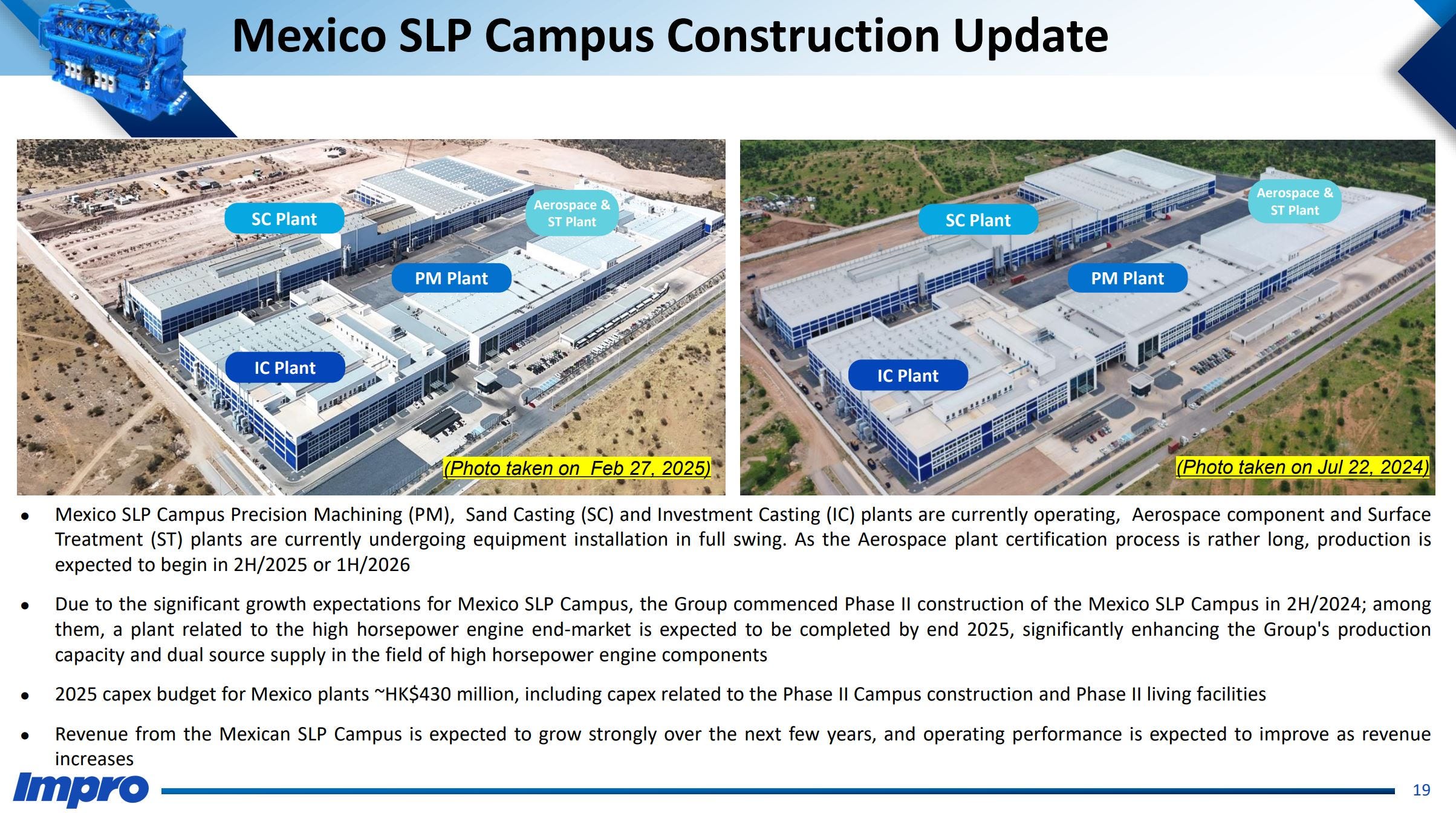

Further, progressively expanding Impro's global footprint is a key tenet of its strategy. The company operates 21 production facilities and nine sales offices strategically located in China, Turkey, Germany, the Czech Republic, and Mexico. The most significant of which is Impro's massive investment in its San Luis Potosi (SLP) campus in Mexico. Situated on a sprawling 68-acre site, the SLP campus was conceived from the ground up as a fully integrated, "one-stop solution" for the North American market. The campus is a comprehensive manufacturing hub, featuring five distinct plants: a Precision Machining Plant, a Sand Casting Plant, an Investment Casting Plant, an Aerospace Components Plant, and a Surface Treatment Plant.

Dual Pillar Strategy

The true power of Impro's strategy lies in the deep operational synergy between its Chinese and Mexican pillars. The SLP campus was explicitly designed to be a beneficiary of the company's global expertise. The company notes that the campus is "built upon the cumulative operational wisdom of Impro employees and best practices of Impro plants worldwide". This is not merely a statement of philosophy; it is a documented operational reality. Impro has executed a deliberate program of talent transfer, relocating experienced personnel in critical disciplines such as plant management, process engineering, quality assurance, and logistics from its established foundries in China to its new operations in Mexico. These individuals serve as "cultivators of Impro culture and operating genes," ensuring that the company's decades of operational excellence and stringent quality standards are replicated faithfully within its North American hub. This demonstrates a long-term vision to create a seamless global production system where institutional knowledge and best practices flow freely across continents.

This dual-pillar structure creates a formidable competitive moat. A purely Chinese-based competitor remains fully exposed to US tariffs and the geopolitical risks of the US-China relationship. A purely North American competitor, on the other hand, faces significant disadvantages. While President Trump continues to push his MAGA directive, the reality is: The U.S. domestic casting and forging industry has been contracting for years, leading to capacity constraints, a critical shortage of skilled trade professionals, and a general hesitancy among suppliers to invest in new capacity after recent boom-and-bust cycles. According to the National Defence Industrial Association,” Over the past two decades, more than 241 forging plants have closed or consolidated, and more than 21,000 jobs have been lost, mostly due to foreign competition. ”

By integrating its operations, Impro circumvents these challenges. It leverages the unparalleled scale and technical expertise of its Chinese foundries for the most challenging upstream processes while utilizing its Mexican hub for tariff-advantaged, logistically superior final production. This "best of both worlds" model allows Impro to offer a value proposition of quality, cost, and reliability that is exceedingly difficult for rivals rooted in a single region to match.

2.2. Analysis of Top Three Key Revenue Growth Drivers (Fast Growers represent ~40% of Group Revenues in FY25)

While Impro's diversification has historically provided stability, the company's future growth is now being disproportionately driven by three powerful, secular, and interconnected trends. These drivers are fundamentally reshaping the company's earnings profile from cyclical to structural growth.

Fast-growth segments (which include high horsepower engines, aerospace, and medical accounts) grew at 14% p.a. between 2019 and 2024, now account for 1/3 of the revenues, and will likely exceed 50% of revenues by 2026.

2.2.1. Driver 1: The AI Data Center Revolution (High Horsepower Engine Segment ~20% Group Revenues)

The standout performer in Impro's portfolio has been the High Horsepower Engine (HHE) segment. In FY2024, this segment's revenue surged by an astonishing 58.6% year-over-year to HK$785.8 million, growing from 10.8% to 16.8% of the Group's total revenue, with positive growth acceleration in 2H, from 43% to 75%.

In contrast to CYD 0.00%↑ and $2722.hk, which we have written about extensively in our previous research, Impro’s AI exposure differs significantly in two aspects:

Impro serves both International and Chinese domestic clients, with America accounting for 50% of group revenues. By contrast, Chinese domestic revenues only account for 17.5% of the group’s total revenues in 2024.

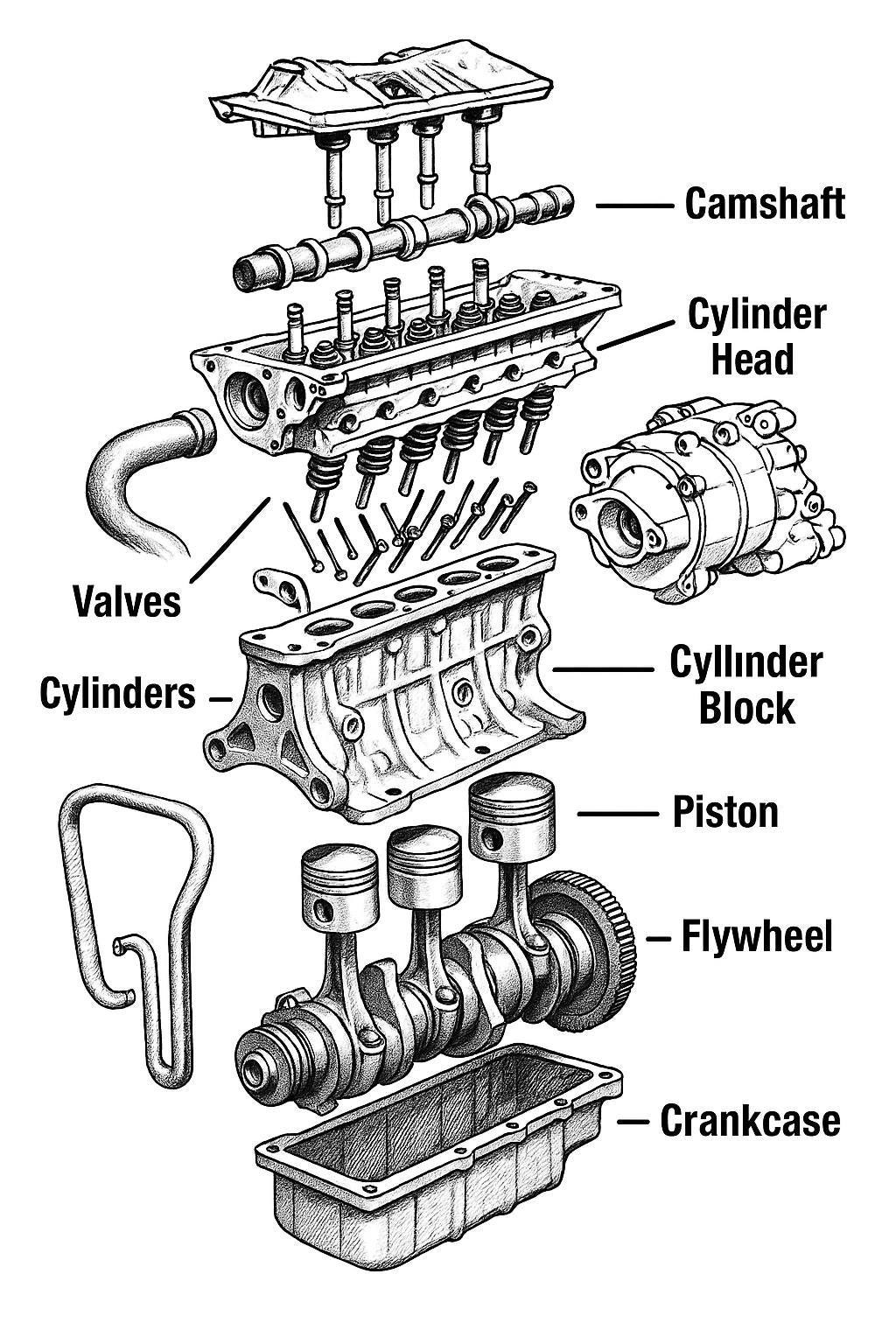

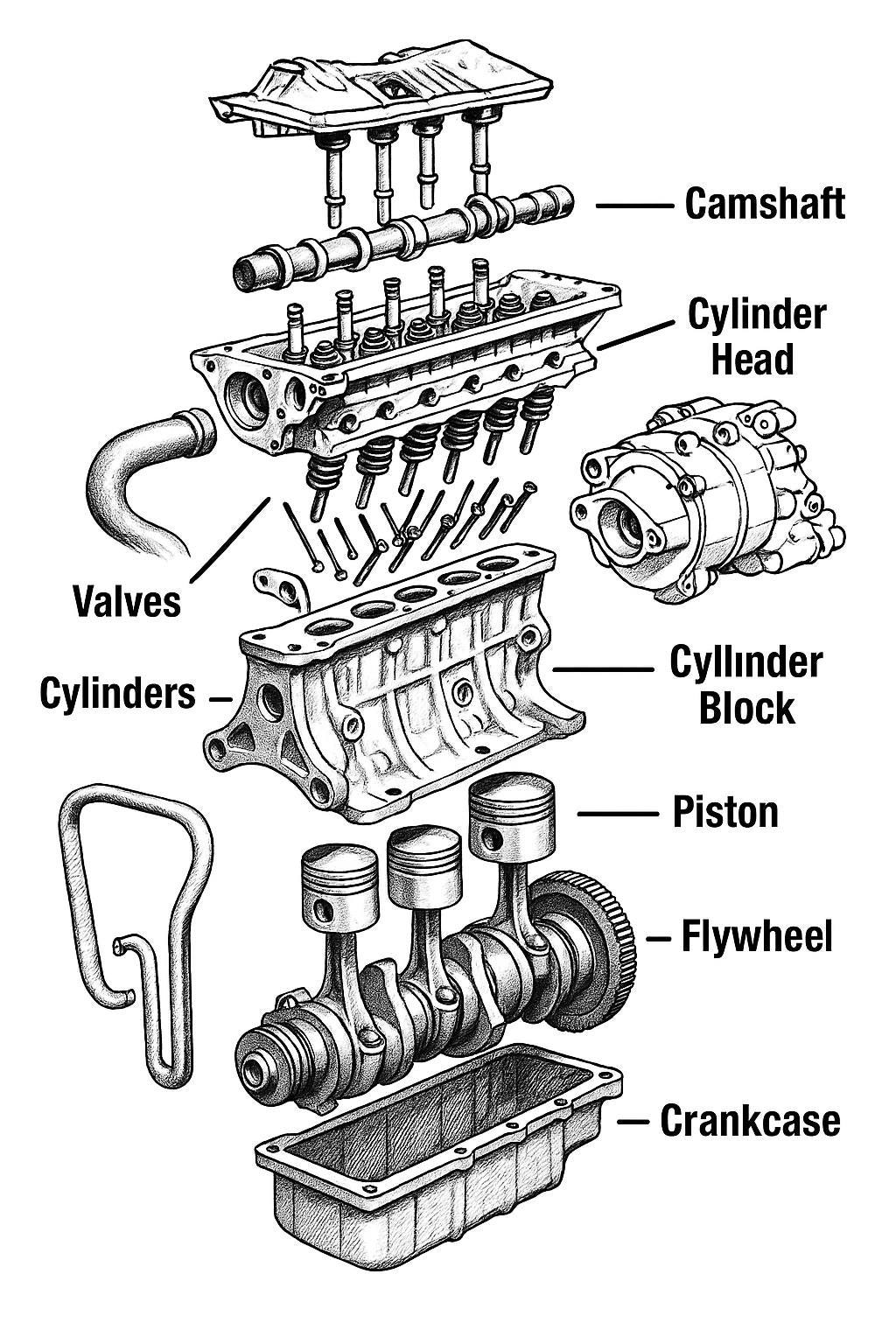

Rather than directly manufacturing/assembling engines, Impro produces a range of key components used in the assembling of engines, including: Cylinder Block, Cylinder Head, and flywheels for leading manufacturers, including Cummins, MTU-Yuchai, and Weichai.

2.2.2. Driver 2: Riding the Aerospace Recovery Wave

Impro's Aerospace segment delivered decent performance in FY2024, with revenue growing 26.8% year-over-year to HK$538.6 million and accounting for 11.5% of total sales. This robust growth was achieved despite well-publicized production issues at its key downstream customer, Boeing, which impacted demand in the second half of the year, indicating the powerful underlying momentum in the business. Overall, with a resumption in Boeing Max deliveries, this bodes well for the second half of the 2025 outlook compared to the cautious tone of management at the end of 2024.

The commercial aerospace market is amid a multi-year supercycle. After the pandemic-induced trough, a combination of pent-up travel demand and the need to replace aging fleets is driving unprecedented demand for new aircraft. Global aerospace industry revenues are projected to grow 12% in 2025, with aircraft deliveries forecast to surge by 23%. Both Boeing and Airbus are sitting on massive, multi-year backlogs that will take the better part of a decade to clear, suggesting that demand will continue to outstrip supply for years to come.

2.2.3. Driver 3: The Nearshoring Advantage (Mexico SLP Campus)

A cornerstone of Impro's long-term strategy is its "Global Footprint" initiative, the most significant manifestation of which is the ongoing development of a large-scale manufacturing campus in San Luis Potosí (SLP), Mexico. This is a major strategic investment, with the company committing to spending over US$300m on the project's completion and expansion. Phase I of the campus, comprising five plants, is now largely complete, and Phase II construction has already commenced to meet the burgeoning demand for high-horsepower engine components in North America.

The strategic rationale for this campus extends far beyond simple labor arbitrage or logistics savings. It is a direct response to the shifting sands of global trade and the increasing premium that North American OEMs place on supply chain resilience and regionalization. The trade tensions between the U.S. and China, compounded by the severe disruptions experienced during the COVID-19 pandemic, have fundamentally altered the risk calculus for major industrial companies.

By establishing a state-of-the-art, multi-process manufacturing hub in Mexico, Impro is transforming its value proposition to its North American customers. It is evolving from a "China-plus" supplier into a genuine "local-for-local" manufacturing partner for clients like Caterpillar and Cummins. This move serves as a critical geopolitical hedge, insulating a growing portion of its business from potential tariffs and logistical bottlenecks associated with its Chinese operations. More importantly, it allows for deeper integration into its customers' North American R&D, product development, and just-in-time production cycles. This strategic proximity and alignment can unlock opportunities for new, higher-value business that might have previously been inaccessible to a purely China-based supplier due to country-of-origin requirements or internal risk assessments. The Mexico campus is therefore a powerful de-risking agent for the business and a catalyst for future growth that should command a higher valuation multiple for the revenue streams it generates.

However, as Mexico remains in the ramp-up phase, this business is currently loss-making on an EBITDA and operating profit basis, depressing wider group earnings.

2.3. Navigating the Cycle in Legacy Markets (~60% of group revenues in FY25)

While the secular growth drivers are reshaping the company, Impro's legacy segments remain exposed to traditional economic cycles. Between 2019 and 2024, slow-growth segments grew topline at 2% CAGR.

The Construction and Agricultural Equipment segments are currently facing a cyclical downturn, with revenues declining by 6.7% and 23.0%, respectively, in FY2024. This weakness is corroborated by commentary from key customer Caterpillar, which reported a 19% sales decline in its Construction Industries segment in its most recent quarter, citing changes in dealer inventories and softening demand. Broader industry forecasts predict that the global construction equipment market will experience another year of negative growth in 2025 before a recovery begins to take hold in 2026, with the key North American market expected to decline by as much as 11% in 2025.

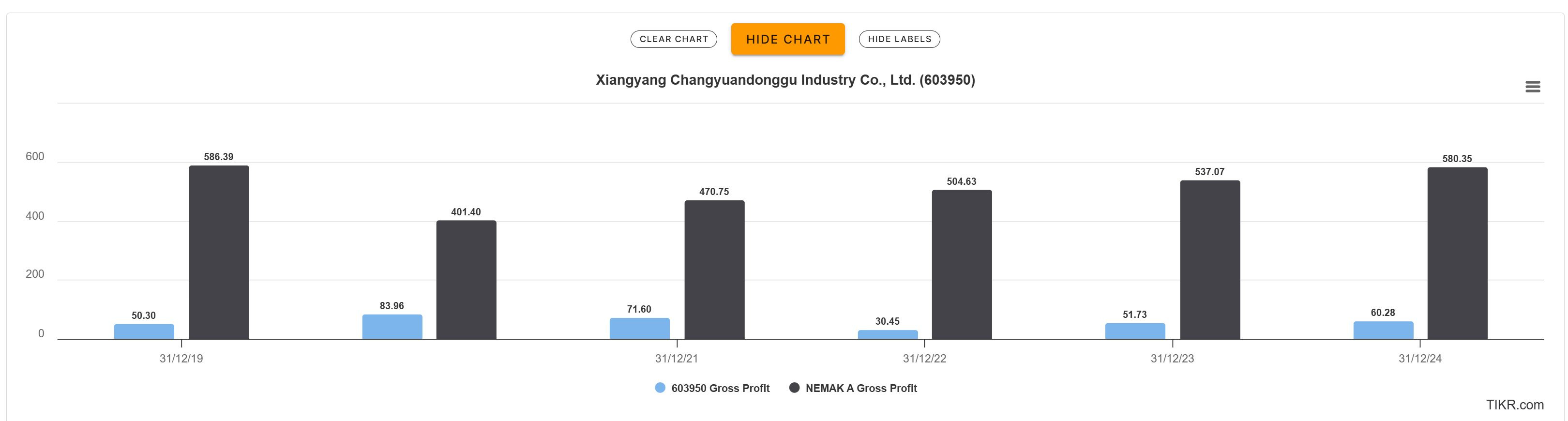

The Automotive segment, Impro's historically most significant end-market, accounting for 1/3 of group revenues, saw a modest 3.2% sales decline in FY2024, with a 2.0% increase in passenger car components being offset by an 8.3% drop in the commercial vehicle market. This segment is navigating a complex environment characterized by macroeconomic uncertainty, high interest rates impacting consumer demand, and the ongoing, capital-intensive transition from internal combustion engines (ICE) to electric vehicles (EVs). However, despite the well-publicized demise of the auto industry, we believe leading peers, including Impro, pure-play Chinese peer Changyuandonggu, and Mexican pure-play Nemak, have all managed the transition responsibly well, reporting stable gross profits despite significant headwinds from EV adoption.

Section 3: Management and Corporate Governance: Founder's Conviction Signals Deep Value

3.1. Management and Board Structure

Impro Precision is a founder-led organization, a characteristic often associated with long-term strategic vision and a deep commitment to the business. Mr. Lu Ruibo, who founded the company in 1998, continues to serve as both Chairman of the Board and Chief Executive Officer.

The company acknowledges in its corporate governance report that this dual role represents a deviation from the Hong Kong Stock Exchange's Corporate Governance Code, which recommends the separation of these positions to ensure a balance of power and authority. The Board justifies the current structure by highlighting Mr. Lu's foundational role and extensive experience in guiding the Group's growth, which it believes is in the best interests of the company. This risk is mitigated by a strong board structure, which includes a majority of independent non-executive directors on its key committees, and a board composition of four executive directors and three independent non-executive directors, ensuring a significant independent element to provide oversight and challenge.

3.2. Capital Allocation and Shareholder Returns

Impro's capital allocation strategy reveals a strong and direct commitment to delivering shareholder value, though it manifests in a manner that is distinct from many of its peers.

The company has demonstrated a robust and consistent dividend policy. For FY2024, a total dividend of 16.0 HK cents per share was declared, which equates to a dividend payout ratio of approximately 49% of the adjusted profit attributable to shareholders. This commitment is not a recent development. Since its IPO in June 2019, Impro has distributed cumulative dividends of approximately HK$1.16 billion. Remarkably, this figure exceeds the total proceeds of HK$1.15 billion that the company raised from its public offering, signaling a powerful commitment to returning capital to its owners.

While the company has a general mandate from shareholders authorizing the repurchase of up to 10% of its outstanding shares, there is no public record of the company having executed any corporate share buybacks. This is a notable point of divergence from many publicly listed companies that utilize buybacks as a primary method of returning capital.

However, the absence of corporate buybacks is overwhelmingly compensated for by a far more powerful signal of intrinsic value: massive and repeated insider purchases by the Chairman and CEO. Through his personal holding company, Mr. Lu Ruibo has engaged in a significant program of acquiring additional shares on the open market. Since the beginning of 2022, he has executed seven separate purchase transactions, accumulating a total of 200 million shares for a total consideration of over HK$420 million. This aggressive buying has increased his ownership stake to approximately 71.9%, representing an investment of a substantial portion of his net worth.

Section 4: Valuation: Undervalued and Misunderstood

Our valuation analysis indicates that Impro Precision remains significantly undervalued. The market currently assigns the company a multiple reflective of a low-growth, cyclical industrial business, failing to account for the structural shift in its earnings towards secular growth drivers and its strengthening competitive moat. We believe the half-year results, slated for the 12th of August, could catalyze potential re-rate.

Section 5: Key Investment Risks

An investment in Impro Precision is subject to several key risks that must be considered:

Geopolitical and Regulatory Risk: With a significant portion of its manufacturing assets still located in China, the company is exposed to the ongoing trade and political tensions between the U.S. and China. While the Mexico facility mitigates this risk, it is not eliminated. Further, the United States government and regulatory bodies are increasingly aware of and concerned about Mexico's role as a potential "backdoor" for Chinese goods to enter the US market and circumvent tariffs. Trade data clearly shows a surge in Chinese investment in Mexico and a corresponding increase in Mexican imports of Chinese intermediate goods, particularly in the automotive sector. This trend will undoubtedly be a central focus of the USMCA's scheduled joint review in 2026. At that time, the Rules of Origin or provisions related to investment from non-market economies could be significantly tightened.

Execution Risk: The successful and timely ramp-up of the Mexico SLP campus is a critical component of the investment thesis. The project is large and complex, and any significant construction delays, equipment installation issues, quality control problems, or cost overruns could negatively impact the company's financial results and delay the realization of the facility's strategic benefits. Furthermore, currently the facility is under specific regulatory inquiry initiated by the United States regarding labor practices at the Mexico facility, which represents a tangible near-term risk that could result in financial penalties, reputational damage, or operational disruptions (link).

Key Person Risk: The company's strategy and vision are heavily influenced by its founder, Chairman, and CEO, Mr. Lu Ruibo. His deep industry knowledge and entrepreneurial drive are significant assets. Furthermore, his ~72% ownership stake gives him effective control over the company's strategic direction. His unexpected departure would create a leadership vacuum and significant uncertainty for the business.