Reporting Season Alpha: Where Governance Meets Multi-Billion-Dollar Alpha

From Yonex’s rally to CQME’s hidden billion-dollar JV, we unpack the signals most investors are missing

Overall, reporting season has been smooth for the majority of companies we’ve profiled on this platform. But beneath the surface, governance tailwinds and overlooked assets are quietly reshaping value.

Yonex (link) delivered +40% MTD and +70% total return since we first featured it in February. A textbook case of how strong governance and pricing power can unlock outsized performance. While our thesis flagged pricing power as the key driver, the sheer magnitude of earnings upgrades—and market recognition—caught even the bulls off guard.

CQME (link) surged +28% MTD, +50% since June, validating our call to double down back in June (link). The company guided for double-digit earnings growth, delivered +50%, and beat across every major segment—including joint ventures. Importantly, CQME reinstated an interim dividend for the first time since listing—a signal of governance reform with teeth.

We also note a pending share incentive scheme, awaiting State approval, that would further align management with minorities. For political watchers: Chongqing Party boss’s self-assessment scorecard in Study Times mapped almost point-for-point to CQME’s business fortunes. Yet most domestic investors remain fixated on minutiae (e.g. Cummins JV engine mix) instead of the bigger picture while international investors struggle with basic concepts like whats a Chongqing.

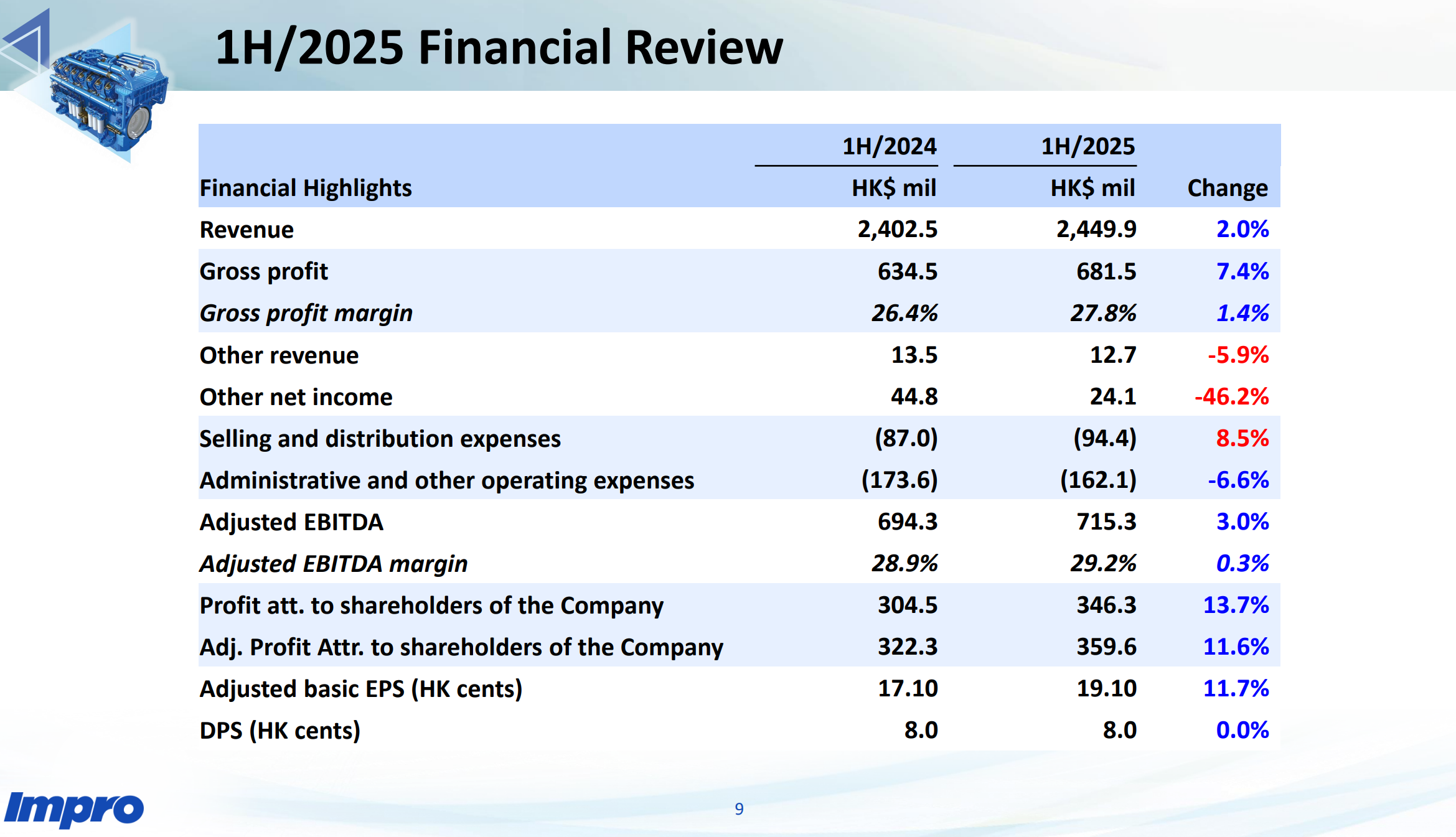

Impro Precision (link) +25% MTD despite volatility around Mexican tariff risk. The reality: Impro is positioned to pass through tariffs given supply tightness, evidenced by a 50% hike in 2025 capex at its Mexican facility (~HKD600m). Execution risk remains the key debate.

Thakral Corporation (link) added +13% MTD in line with expectations. What mattered: the company immediately resumed buybacks post-results. YTD, buybacks equal 0.8% of SO (0.2% in July, 0.6% in August). For the first time, management explicitly flagged buybacks as a top capital allocation priority.

CYD/H22 (link) +46% MTD, a testament to its core turnaround, data center growth optionality, and IPO prep—all significantly ahead of our February projections.

Portfolio Updates:

We have added to CQME and CYD, funded by a full exit from Impro Precision.

CQME & CYD both trade below book with multiple catalysts for earnings acceleration.

Impro now sits at 1.3x book, with slower growth and tariff execution risk. Congratulations to those who rode Impro—bragging rights: you’ve officially outperformed Buffett in castparts.

Why CQME Still Gets Better 📈

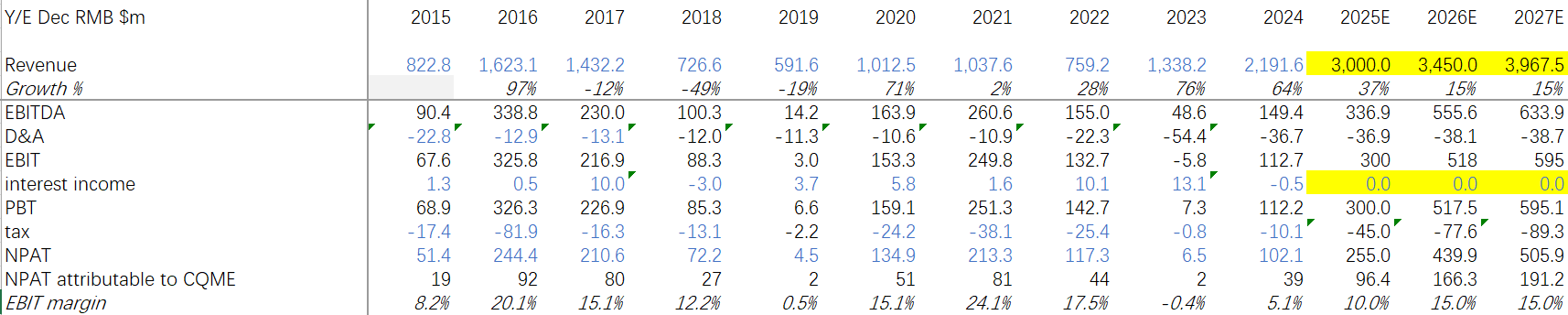

A key overlooked driver: Hitachi/ABB Chongqing JV. Historically CQME’s largest earnings contributor, it received ¥850m in 2020 govt. support to build a new plant (completed 2023). With Hitachi’s 2023 acquisition of ABB’s energy division, expansion accelerated again in 2024, positioning the JV for >¥5bn revenue capacity.

CQME owns 37.8% of this business.

We forecast ¥100m NPAT attributable to CQME in 2025, inflecting higher as capacity ramps.

Over 50% of products are exported—a rarity for a Chinese industrial, underscoring demand strength.

Historically, Hitachi/ABB Chongqing was the biggest joint venture earnings driver for CQME, with CQME owning 37.8% of the business. The business was so succesful that in 2020, the Chongqing government provided ¥850mn in funding (link) for the company to establish a larger factory that was complete in 2023. With the acquisition of ABB’s energy division by Hitachi in 2023, Hitachi choose to further expand the capacity in 2024 (link) which we understand will be able to support a revenue base of over ¥5bn once complete. However as the company is in expansion phase, this has temporarily depressed earnings and dividend payments (the the JV appears to have paid out the ¥850mn funding as a special dividend in 2020 and then used construction debt to fund the expansion), which is why we failed to incorporate this business in our initial assessment.

The table below depicts the historical financial performance of the business and what conservative forecasts may look like: With over ¥100m NPAT attributable to CQME alone in 2025, before earnings further inflect as capacity ramps (we understand over 50% of its current products are exported, an extremely high proportion for any Chinese business highlighting the strong demand), its not hard to envision why this businesses valuation starts with a billion. Further, we believe the business could be a significant beneficiary to China’s recently annouced $170bn Moutou Hydropower project (link) over the longer term given its historical track record in Three Groges Project. While the market currently values this business at near 0, it’s not hard to envision a scenario where this businesses valuation alone supports the current entire market cap of CQME. (¥5bn revenues, 17.5% net margins, 20x PE equates to ~HKD7bn valuation attributable to CQME vs. similar current market cap).

Closing

This earnings season reinforced one theme: corporate governance reform is no longer abstract—it’s translating into hard cash and multi-bagger potential.

Yonex, CQME, CYD, Thakral: four case studies of how Asia’s legacy companies can be re-rated when governance catches up with fundamentals.

Hey - any updates to Chongqing M&E? See share prices has taken a hit, even before this AI pullback started.