Return of the Power King

Ride the Momentum, Pursue Long-Term Success: A 75-Year Odyssey from a Labor Reform Camp to a Global Power King

Summary

The story of China Yuchai International Limited CYD 0.00%↑ is among the most compelling—and persistently misunderstood—sagas in the universe of U.S.-listed Chinese equities. For more than three decades, the company has reigned “King” of China’s internal combustion engine (ICE) market, commanding a leading share across heavy-duty trucks, buses, and off-road machinery through its core operating subsidiary, Guangxi Yuchai Machinery Company Limited (GYMCL).

Yet for most of its public life, CYD has traded at valuations implying terminal decline. This discount was not driven by operating irrelevance, but by a toxic mix of corporate governance complexity, the infamous “Golden Share” structure held by Hong Leong Asia, and a persistent conglomerate discount that trapped investor perception in the early 2000s.

As investors look toward 2026, however, the foundations underpinning this narrative are shifting. The “King” is attempting a return—not by defending legacy diesel franchises alone, but by executing a strategic pivot under its “1235 Strategy,” repositioning Yuchai from a domestic engine manufacturer into a globalized powertrain and green-energy solutions provider.

The convergence of governance normalization, AI data center power demand, global expansion, and the commercialization of new energy technologies has created the most credible re-rating setup CYD has seen over the past two decades.

This report traces Yuchai’s evolution, dissects the governance battles that suppressed historical earnings and valuations, contrasts its conservative trajectory with Weichai Power’s aggressive capital strategy, and frames the operational roadmap that underpins our constructive 2026 outlook.

Part I: The Genesis of the King (1951–2002)

To understand the magnitude of Yuchai’s current transformation, one must first appreciate the depth of its roots. The company’s history is a microcosm of China’s own industrial evolution—from a provincial factory to a global powerhouse navigating the complexities of international capital markets.

From the Rice Fields of Guangxi

Yuchai’s origins date back to 1951 in Yulin, Guangxi, where it was established with a 20,000-yuan grant as a labor-reform workshop producing agricultural tools. Known then as the Yulin Qiantang Industrial Society, the facility reflected China’s early post-war industrial priorities rather than any grand commercial ambition.

By the late 1950s, the factory had pivoted toward internal combustion engines, trial-producing early diesel models with minimal external technical support. The 1970s marked a structural inflection: labor-reform inmates were removed, and the enterprise was renamed Yulin Diesel Engine Plant—signaling its transition into a professionalized industrial manufacturer.

The Wang Jianming Era: The Rise and Fall of the “Power King”

In 1985, Wang Jianming—a graduate of Shanghai Jiao Tong University—was appointed director. Under his leadership, Yuchai experienced a meteoric ascent:

1992 Shareholding Reform: Yuchai became an early adopter of China’s corporatization reforms, transitioning to a shareholding structure.

1994 NYSE Listing: Yuchai became only the second mainland Chinese company to list on the New York Stock Exchange. Remarkably, it remains the longest-continuously listed Chinese company in the U.S., surviving the Asian Financial Crisis, Sarbanes-Oxley, and recent U.S.–China audit disputes.

Scale Leadership: By the mid-1990s, Yuchai had become China’s largest internal combustion engine production base.

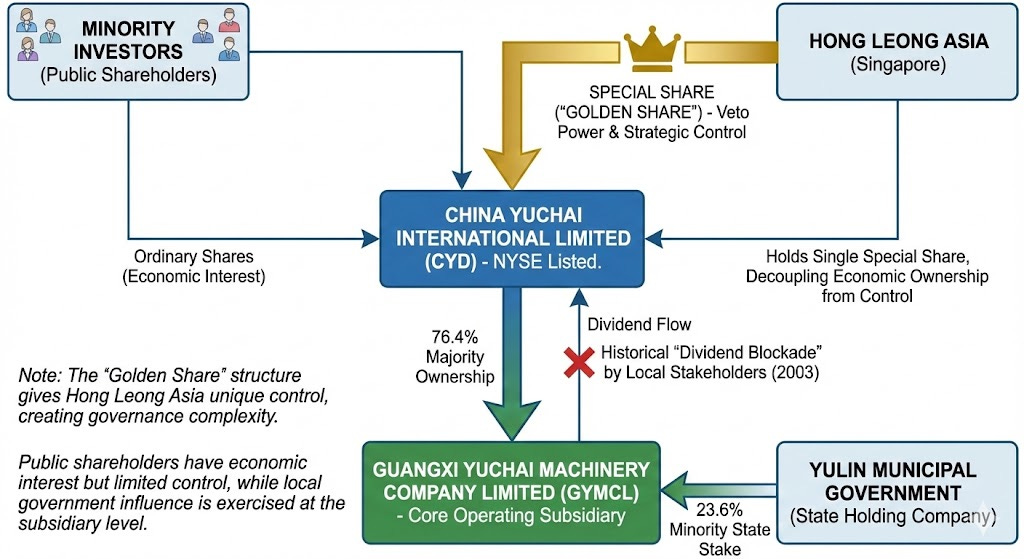

The IPO was not merely financial—it was geopolitical. Capital raised in New York was reinvested directly into modernizing Yulin’s production base. The structure established China Yuchai International (CYD) as the majority owner (76.4%) of GYMCL.

Part II: The Battle of Golden Share (2002–2005)

To facilitate the IPO, a latent control mechanism was embedded into the corporate structure: the “Golden Share.” This arrangement decoupled economic ownership from voting control by giving the holder powers, including:

Appoint 6 of 11 CYD directors

Appoint 5 of 13 GYMCL directors

Veto power over all shareholder actions

Public shareholders and the Yulin government bore the economic risk, while strategic control rested with Hong Leong. For nearly a decade, this tension was masked by growth and Wang Jianming’s ability to bridge foreign shareholders and local interests. As growth slowed and political priorities shifted, the fault lines widened.

The 2003 Dividend Blockade

The crisis was triggered on August 23, 2002, with the liquidation of Diesel Machinery (BVI) Limited (DML). For years, DML had served as a neutral buffer, holding the “Special Share” (which carried board-control rights) in a joint venture between Hong Leong Asia and China Everbright. As Everbright pivoted away from industrial assets to build a domestic financial powerhouse, the liquidation of DML consolidated unilateral control of the Special Share directly into Hong Leong’s hands.

Sensing a loss of local influence, the Yulin City Government moved swiftly. In September 2002, acting through its offshore intermediary Goldman Industrial, it acquired Coomber Investments Limited from China Everbright. This gave the Yulin government a strategic 24.3% “stealth” stake in the NYSE-listed parent company.

The tension broke when Yulin sought confirmation that it would inherit Everbright’s historical rights, including the power to nominate two directors to the boards of both CYD and its operating subsidiary, Guangxi Yuchai Machinery (GYMCL). When Hong Leong declined to recognize an automatic transfer of these rights and refused to guarantee that factory dividends would be passed through to the NYSE listed parent, the dispute escalated into a full-scale regulatory blockade.

Claiming the “Special Share” mechanism allowed for unauthorized foreign control in violation of original 1994 approvals, GYMCL distributed dividends to its domestic shareholders while withholding and escrowing the RMB 245.7 million attributable to the NYSE parent. For CYD’s public shareholders, the message was stark: profits were being generated, but the cash was trapped onshore—leaving the listed entity an “economically hollow” shell despite its industrial dominance.

MOFCOM Intervention and the July Truce

In March 2003, the conflict reached Beijing. GYMCL petitioned the Ministry of Commerce (MOFCOM), which issued a correspondence in April advising that the ownership structure required “rectification.” This effectively validated the local government’s blockade and institutionalized the “governance discount” that would plague the stock for years.

A fragile truce was finally reached in July 2003. Under the resulting Reorganization Agreement:

The RMB 245.7 million in withheld dividends were released to the parent.

Two senior financial managers appointed by CYD, who had been locked out of the factory, were reinstated.

Governance reforms were promised to bring the subsidiary in line with international standards.

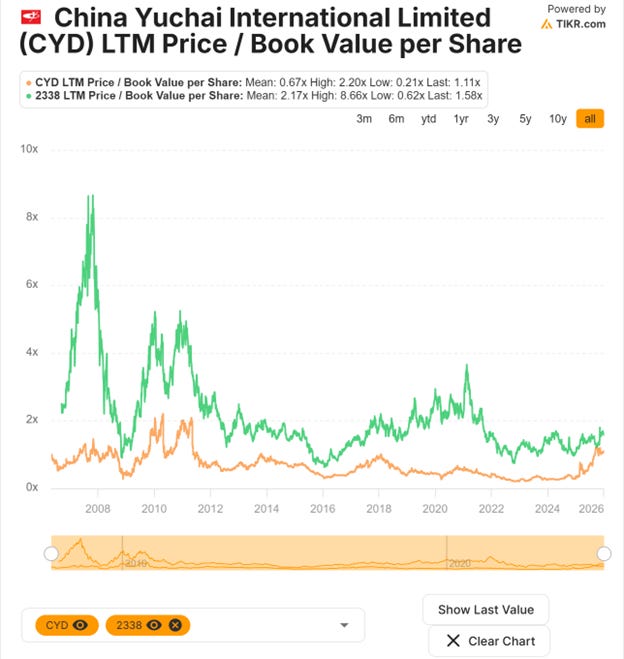

Yet, while the cash flowed again, the Golden Share survived, and with it, a persistent market distrust. For the next two decades, investors viewed CYD as a company where economic rights could always be subordinated to local political outcomes—cementing a perpetual significant valuation discount relative to its peer, Weichai Power (2338.HK) - until now.

The Removal of Wang Jianming

Caught between Hong Leong and local government interests, Wang’s reformist ambitions—relocating core business functions, attracting external capital, and reducing Yulin dependency—were increasingly viewed as threats. In October 2005, he was removed as Chairman and replaced by Yan Ping, marking the end of Yuchai’s most entrepreneurial era.

Part III: The Two Titans – Yuchai vs. Weichai (2005–2020)

The opportunity cost of Yuchai’s governance paralysis becomes stark when contrasted with Weichai Power (2338 HK).

While Yuchai navigated internal conflict, Weichai—under the leadership of Tan Xuguang—embraced capital markets, vertical integration, and aggressive M&A, markets have rewarded its bold move, returning more than 20% p.a. since its 2004 Hong Kong IPO (vs. 4% p.a. for CYD).

In 2005, Weichai overtook Yuchai in annual sales, and the acquisition of Torch Group secured control of Shaanxi Heavy Duty Truck and Fast Gear, creating a self-reinforcing industrial ecosystem. Subsequent international M&A (Baudouin, KION, Linde Hydraulics, Ballard, Ceres, PSIX, among others) transformed Weichai into a global industrial platform. By 2024, Weichai generated over RMB 200bn in revenue, versus ~RMB 20bn at the CYD listco level (or ~RMB 50bn at the broader group level).

Yuchai, constrained by governance, pursued a different strategy: neutrality. Without captive OEMs, it became the supplier of choice to Dongfeng, LiuGong, and China’s bus market—preserving relevance, but sacrificing scale. Yuchai also proactively forged alliances with international partners, including Rolls-Royce in 2017, to manufacture its Series 4000 power generation engines, with a phase II expanded partnership announced in August 2024 to also incorporate Series 2000 engines.

However, with Mr. Tan’s retirement from Weichai in 2024, this has important implications for the sector and Weichai’s strategy going forward, which we will discuss in further detail in a subsequent note.

Part IV: The Return of the King

In March 2021, a new era began as Li Hanyang assumed the role of Chairman. Unlike the purely administrative transitions often seen in State-Owned Enterprises (SOEs), Li’s background is that of a “grassroots engineer” with a sophisticated technical pedigree.

A 1993 graduate of Tsinghua University in Mechanical Design and Manufacturing, Li was a rarity for his time: a top-tier graduate who chose to leave the coastal hubs for the rugged industrial frontier of Guangxi. His rise within Yuchai is the stuff of company legend:

The Proactive Technician: Starting as a workshop technician, he earned the respect of veteran masters by working alongside them on the shop floor, reportedly even volunteering for menial cleaning tasks to prove his dedication to the “Yuchai spirit”.

The Technical Visionary: After studying CNC programming in the United States in 1994, he returned to modernize Yuchai’s production lines. As head of the Cold Working Plant, he slashed production costs by 15% and improved quality by 60% through performance-based pay reforms.

The Intrepreneur: In 2003, Li led a small project team to found Guangxi Yuchai Power with a modest initial capital of only RMB 2 million. Driven by the vision of creating a "Power Supermarket for Farmers," he identified a massive gap in the rural market for high-tech yet affordable small-bore multi-cylinder engines.

The modern era of China Yuchai began in December 2021 with the formal launch of the “1235” Strategy. This was not merely a slogan; it was a recognition that the old model of relying solely on domestic diesel sales was a dead end in a decarbonizing world.

At the core of Li Hanyang’s leadership is the “1235 Strategy,” a disciplined roadmap designed to transition Yuchai from a legacy manufacturer into a modern power systems leader:

“1” Singular Goal: To achieve the milestone of 1 million power units in annual sales by 2025, establishing a new baseline for global scale.

“2” Parallel Tracks: A commitment to a dual-track strategy where New Energy Power and Traditional Power advance in tandem, ensuring Yuchai remains relevant across all stages of the energy transition.

“3” Strategic Pillars:

Comprehensive: Achieving full coverage across products, markets, and customer segments. This includes expanding beyond legacy high-speed engines to capture the medium- and low-speed engine markets.

Innovative: Focusing on the New Energy frontier, specifically prioritizing hydrogen fuel cells and hydrogen-combustion engines.

Robust: Transforming traditional weaknesses into strengths. For example, Yuchai is aggressively optimizing its presence in the tractor unit (semi-truck) market—a segment where it has historically been underrepresented.

“5” Core Enablers: The strategy is anchored by five fundamental capabilities that ensure execution: R&D Excellence, Manufacturing Precision, Marketing Reach, Service Reliability, and Brand Equity.

Crucially, this strategic reset has been accompanied by tangible governance signals:

The announcement of a new share equity incentive plan at the subsidiary level in June 2024

A annoucement and completion of a $40 million share buyback in August 2024

The announcement of a new share equity incentive plan at the listco level in May 2025

Several high-profile changes in former leadership, beginning with the investigation of former Chairman in July 2025

The announcement of the potential IPO of one of Yuchai’s key subsidiaries, which we have previously written in detail about in August 2025 (link), and the significant growth opportunities this division has given its exposure to the AI data center growth

2025 Records and the 2026 Outlook

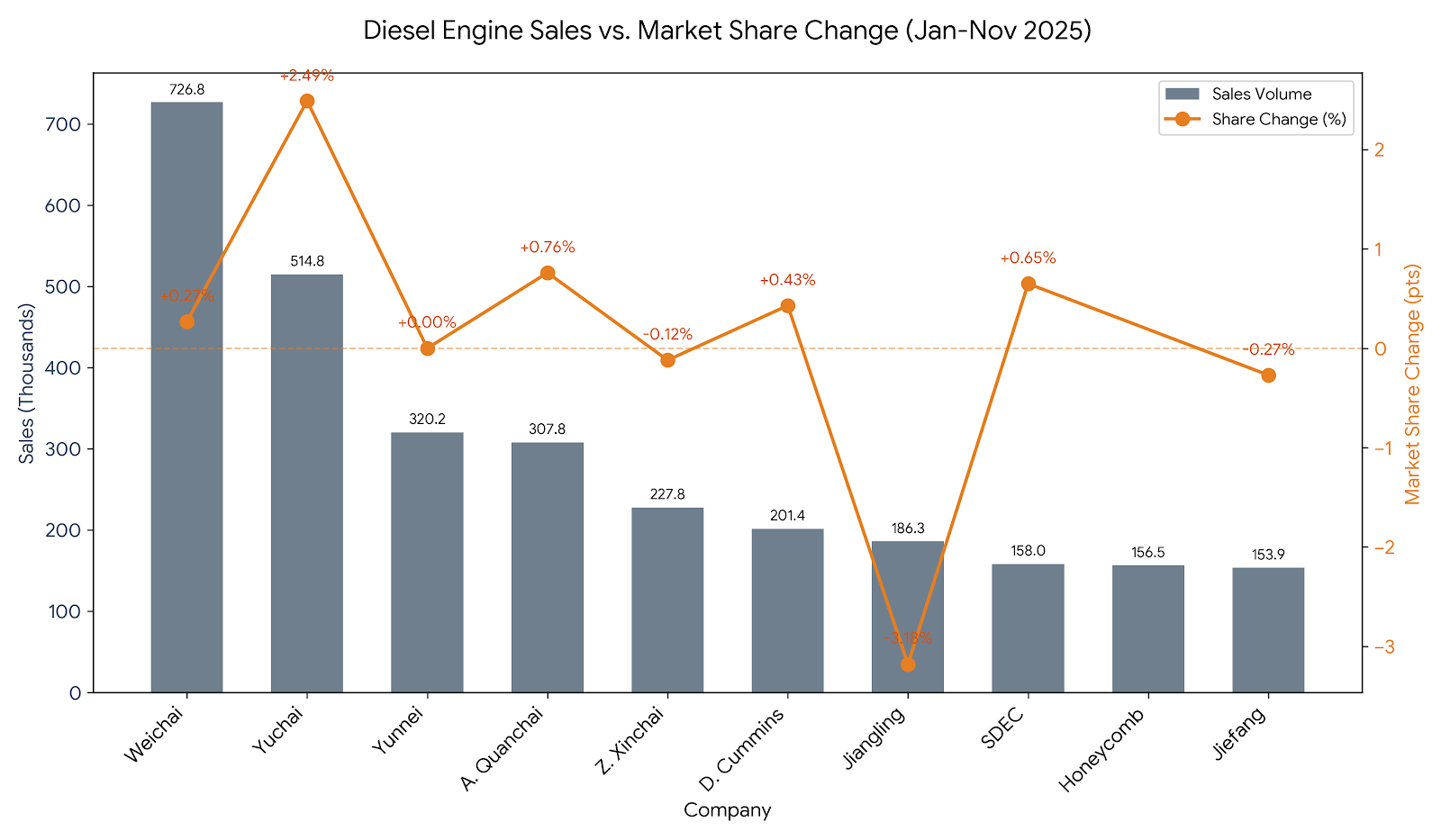

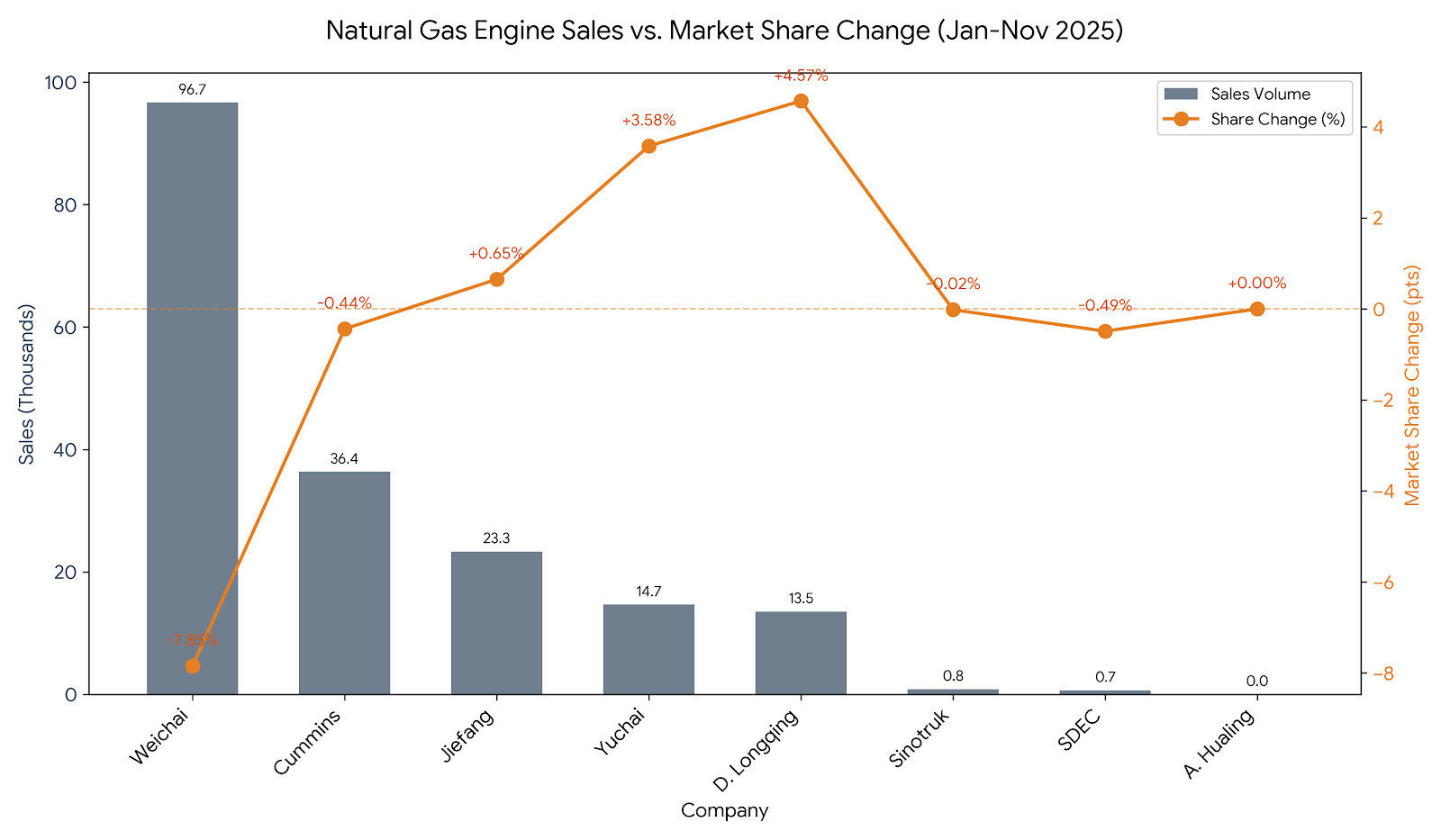

In his December 31, 2025 New Year address—“Ride the Momentum, Pursue Long-Term Success” (乘势而上 笃行致远) (link), Chairman Li declared all-time record highs across volumes, revenues, and profits at the group level. Mr. Li’s commentary is consistent with third-party industry data, showing that Yuchai is one of the largest market-share gainers YTD.

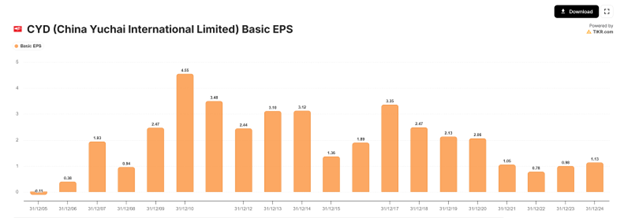

While the CYD listco represents ~40% of the group’s assets, the read-through is unmistakably positive. Consensus FY25 EPS of US$2.18 remains well below historical levels of US$3.00—and far below the US$4.55 achieved in 2010—suggesting earnings normalization alone could drive further upside as its full year results are released in late February.

With the stock having re-rated from ~0.3x to ~1.0x book value since we first profiled the company, we believe 2026 remains catalyst-rich, offering both multiple expansion alongside asymmetric earnings upside opportunities, and we look forward to riding the momentum while pursuing long-term investment excellence.