Trust the Ledger, Not the Legend

Our repeatable framework for avoiding the "Zero"—from Corporate Travel Management to Intellego.

Disclaimer

The following content represents the opinions of the authors and is provided solely for informational and educational purposes. It does not constitute an offer, solicitation, recommendation, or advice with respect to any securities, investment strategies, or investment products in any jurisdiction. This content is not investment advice.

At the time of publication, we hold no short positions in any of the securities discussed; however, we may establish, modify, or close positions at any time without notice.

Our analysis is based on publicly available information, statutory filings, and forensic research. The framework applied does not assert, imply, or allege equivalence of conduct, intent, culpability, or outcome between the case studies discussed. The inclusion of multiple issuers is solely to illustrate recurring risk indicators that have historically preceded permanent capital impairment across industries in different geographies.

We do not represent or warrant that the information presented is accurate, complete, or current, and it should not be relied upon as such. Readers are solely responsible for conducting their own independent analysis and due diligence and should consult qualified legal, financial, or other professional advisors before making any investment or related decisions.

The Asymmetry of Returns

There are two distinct disciplines in the pursuit of alpha:

Value: Buying assets below intrinsic value. We have already detailed a number of these opportunities in our previous research, including our first 2026 highlight (link).

Capital Preservation: Avoiding the “zeros”—the permanent impairment of capital. A less discussed topic in general by industry practitioners.

As Warren Buffett famously observed:

Rule No. 1: Never lose money. Rule No. 2: Never forget Rule No. 1

This note focuses exclusively on Rule No. 1, and on our process for identifying risks that can lead to permanent capital loss.

The Origin of Our Framework

Regular readers of this newsletter will recall our recent profile of Intellego Technologies (INT.ST) (link), a company whose CEO was subsequently arrested on suspicion of gross fraud.

What may be less well known is that the forensic framework applied in that analysis was developed over many years. Its origins trace back more than eight years to our research on Corporate Travel Management (CTM), where we independently identified a series of structural risk indicators that were examined in detail in VGI Partners’ 176-page public short report (link).

Fast forward to today: CTM is in a trading halt, unable to file its FY25 full-year accounts, with KPMG engaged to resolve a dispute with its auditor, Deloitte. Subsequent regulatory and audit processes have publicly reported that CTM overcharged UK clients, including government entities, by £77.6 million over a number of years—effectively recognising unearned revenue as profit.

Amid severe liquidity constraints, some institutional investors have reportedly begun marking down the value of their CTM investments, in certain cases to zero.

While operating in different sectors—industrials versus corporate services—CTM and Intellego exhibit a striking convergence of warning signs. The framework below reflects the questions we used to identify risk in both cases.

The Forensic Checklist

When analyzing a potential outlier, we ask three core questions:

Governance Gatekeepers

Is the valuation premium driven by a charismatic or “messianic” founder? If so, what checks and balances are in place? Are the board and senior management empowered to challenge decisions, or do key oversight roles function as revolving doors? Persistent turnover—particularly within the finance function—can signal discomfort among those closest to the ledger, even when external approvals remain intact.

Unit Economics

Does the company claim software-like margins in a fundamentally commoditised industry? If margins are “super-normal,” do cash flows corroborate those claims—or is the divergence widening?

The Physical Verification

Do statutory accounts reconcile with physical reality? When the digital narrative presented in investor materials conflicts with the observable footprint—offices, factories, staff, products—we default to the physical evidence.

Attentive readers may note that these are the same categories of questions posed to management in our prior report—questions that, to date, have not been substantively addressed.

Author’s note: Mr. Rosenqvist has ceased to be a Director of Intellego’s Chinese subsidiary, according to the latest Chinese regulatory filings. Separately, Swedish media have reported that Mr. Rosenqvist denies recent involvement with Intellego’s Chinese operations, having left the parent board in 2023.

Intellego has since engaged KPMG to conduct a forensic review of its accounting practices and capital-market communications. We hope this process will provide clear, verifiable answers for the company’s shareholders.

Case Study 1: Corporate Travel Management

ASX: CTD | USD $1.7bn Market Cap

1. The Charismatic Leader & The Revolving Door

Founder Jamie Pherous publicly positioned Corporate Travel Management (CTM) as a challenger to traditional corporate travel models, frequently emphasising the company’s technology capabilities alongside its service offering. This positioning coincided with a period during which the company traded at a valuation premium and was widely supported by Australian small-cap institutional investors.

Following the release of a short-seller report by VGI Partners in October 2018, CTM rejected the report’s conclusions, characterising the analysis as flawed and indicating that it would consider legal options. In response to market scrutiny, CTM disclosed that it had engaged Ernst & Young to conduct an independent review of certain issues related to its FY2018 financial statements. While the company publicly stated that the review did not identify material misstatements, the full EY report itself was never released, with only selected conclusions summarised in a November 2018 ASX market update.

Under our governance framework, we assess where critical judgment resides within an organisation. Risk can arise when highly subjective revenue and cost items are determined centrally rather than at the regional level. While such centralisation is not inherently improper, it can weaken the linkage between reported profitability and underlying local commercial activity, introducing opacity at the head-office level. In our experience, this dynamic often places sustained pressure on senior finance leadership to reconcile external guidance with operational realities. Across markets, this form of structural tension is frequently associated with elevated turnover in senior finance roles.

At CTM, these characteristics coincided with notable instability in the finance function:

Steve Fleming (Global CFO): The long-time global CFO moved to a regional role in 2019 amidst scrutiny, leaving the firm altogether shortly thereafter.

Neale O’Connell (Global CFO): Resigned after less than two years in the role.

Cale Bennett (Global CFO): Resigned after two years in the role, with James Patterson holding an interim position for one year before current CFO James Spence joined in late 2024.

2. The “Tech” Moat vs. Cash Flow Reality

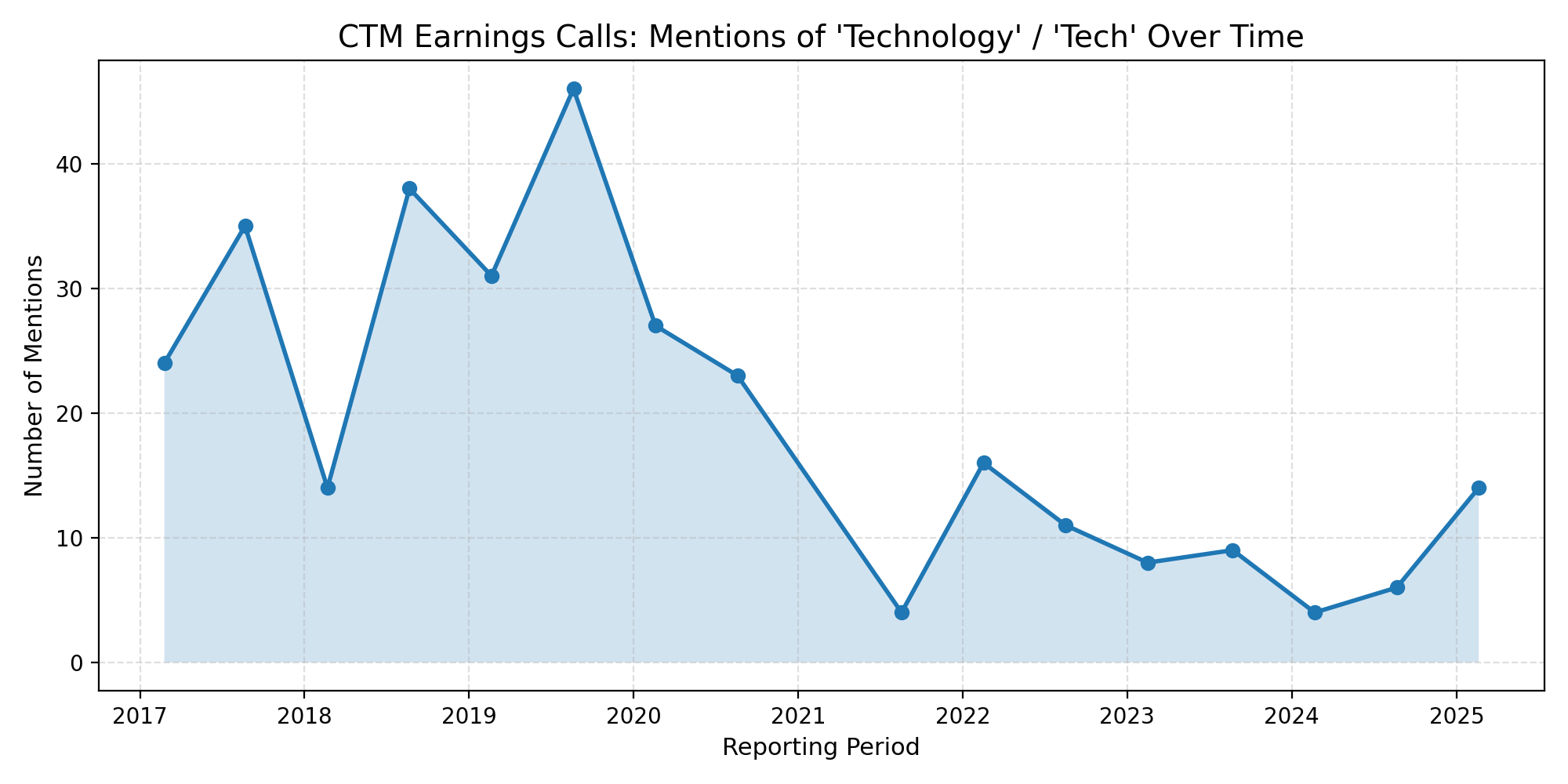

CTM consistently reported EBITDA margins of approximately 30%, nearly double those of peers such as Amex GBT, attributing this efficiency to technology and automation.

The Tech Reality:

VGI’s IP searches in 2018 found zero granted patents, and physical checks revealed regional offices using standard, white-labeled third-party software rather than a proprietary stack.

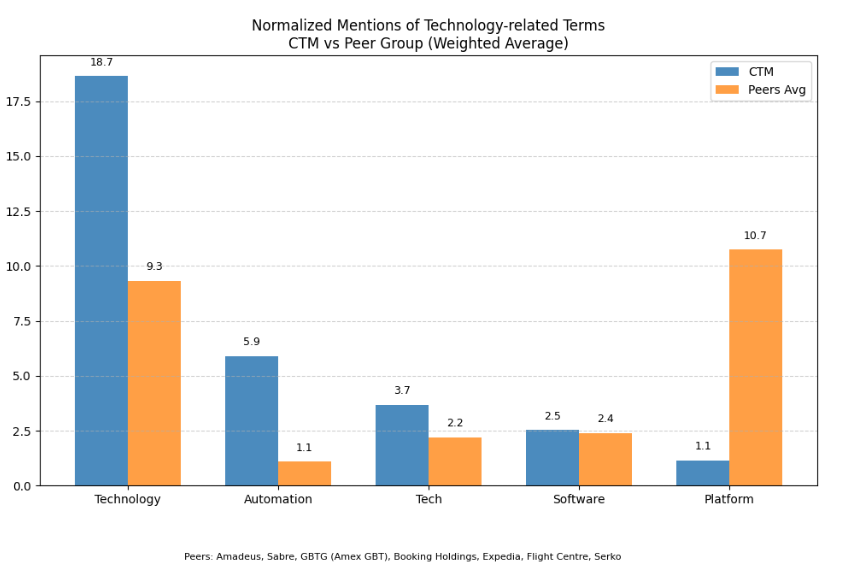

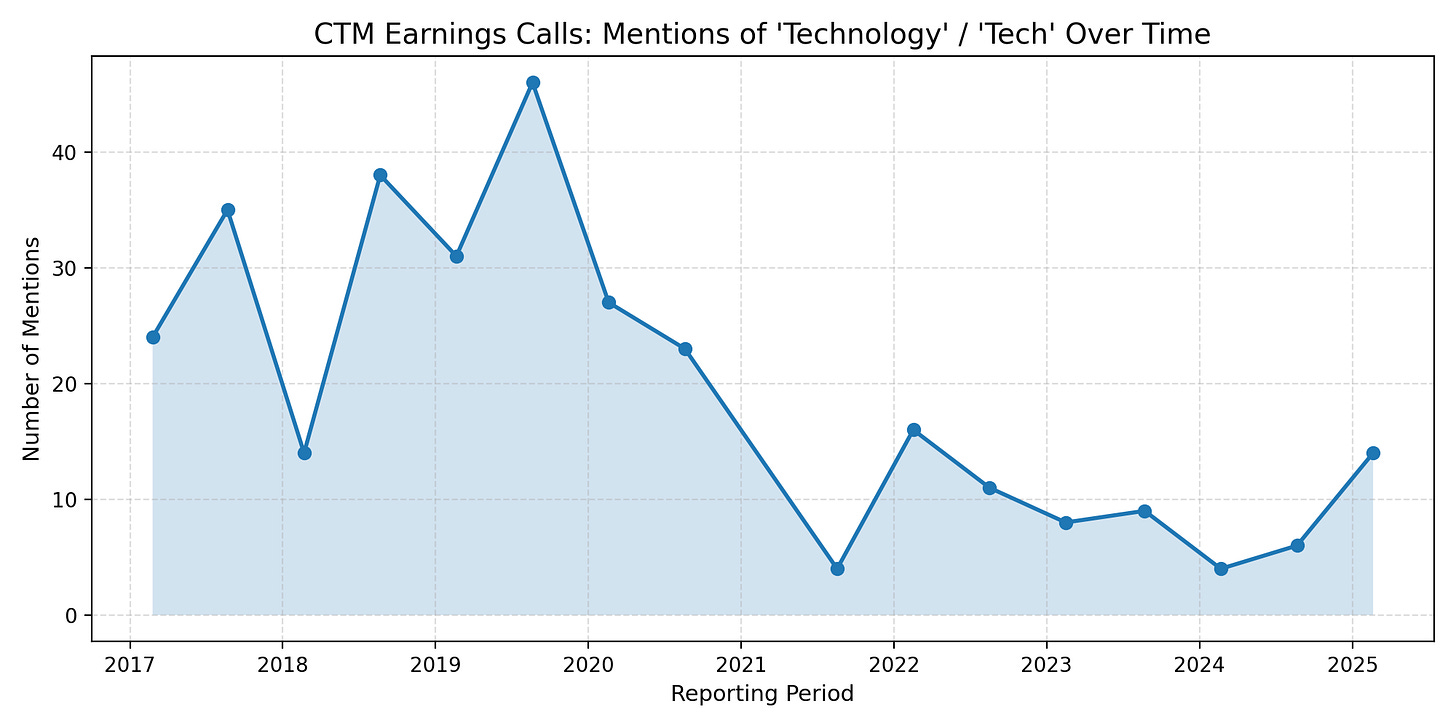

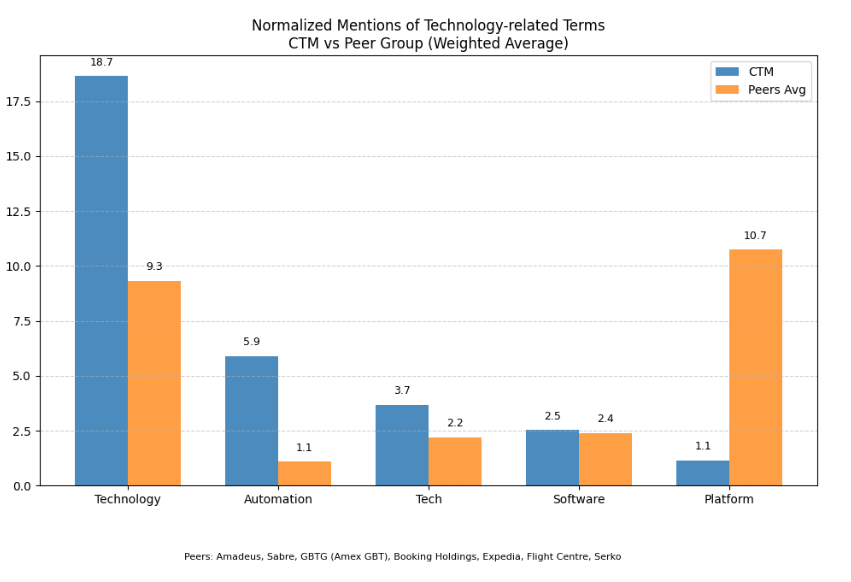

Our quantitative linguistic analysis of CTM’s earnings call transcripts shows that management’s emphasis on “technology” and “automation” was materially higher than that of industry peers and intensified during periods of margin scrutiny. By contrast, peer companies more frequently refer to “platforms,” reflecting sustained investment in multi-product technology architectures. This divergence in language is consistent with differences in business models rather than communication style alone.

The Margin Mirage:

While VGI’s analysis primarily examined CTM’s super-normal margin profile from a European and consolidated perspective, our research at the time focused more closely on the company’s Asian operations.

In 2018 and 2019, CTM reported EBITDA margins in Asia exceeding 30%—a highly competitive market where the largest local peers were earning roughly half that level of profitability. At the same time, many second-tier players were loss-making amid the disruption caused by China’s first tariff war and Hong Kong protests. Subsequent disclosures in FY19 indicated that more than 30% of reported Asia revenues were derived from volume-based incentives.

Cash Flow Divergence:

While a detailed technical discussion of principal-versus-agent considerations and IFRS 15 (Revenue from Contracts with Customers) accounting is beyond the scope of this report, these accounting frameworks are, by design, highly judgment-dependent and can materially influence the timing of revenue and earnings recognition.

In this context, VGI observed that despite reporting substantial cash balances at each reporting date, CTM consistently earned an implausibly low return on cash on hand. This pattern suggests that a material portion of reported cash may not have been freely available at the group level, even if the year-end cash balances are “consistent with the average monthly balance across the preceding 12 months”, as reported in EY’s conclusion.

In parallel, our analysis indicates that CTM’s Asian operations were structurally working-capital-intensive, requiring significantly more cash to support day-to-day business activity than their reported earnings contribution would imply.

Taken together, these factors complicate the interpretation of reported earnings and cash conversion and warrant careful consideration when assessing the sustainability of reported profitability.

Notably, CTM’s FY24 disclosures include expanded discussion of contract liabilities and revenue recognition judgments under IFRS 15, highlighting the continued sensitivity of reported results to accounting assumptions.

3. Irreconcilable Accounts & Ghost Offices

Among the most concerning findings documented by VGI was the disconnect between the digital narrative and physical presence.

Ghost Offices: Site visits to listed offices in Stockholm, Glasgow, and Paris revealed they were either non-existent or occupied by unrelated tenants. A “Dutch Harbor, Alaska” address traced back to a Safeway supermarket.

Statutory Mismatches: An analysis of statutory accounts showed significant changes to revenue recognition policies over the years.

Case Study 2: Intellego Technologies

Nasdaq First North: INT | USD $700m Peak Market Cap

1. The Charismatic Leader & The Revolving Door

Claes Lindahl founded Intellego in 2011, promoting a vision of transforming a Swedish nano-cap into a global leader. Following the publication of our forensic report on Intellego’s purported Chinese operations on October 10, 2025, the company did not engage with the underlying concerns. Instead, it publicly attacked the analysis as “factually incorrect” and alleged market manipulation on October 13, 2025.

According to Swedish financial media reporting, the board subsequently approved a multi-million-SEK bonus payment to Lindahl, which was paid around November 11–12, 2025, ahead of Lindahl’s planned trip to China. The company stated that the payment was authorised under its remuneration framework following what it described as strong performance and revenue growth during 2025.

The narrative unraveled on November 18, 2025, when Lindahl was arrested on suspicion of gross fraud (grovt svindleri). Institutional fallout followed swiftly. On November 26, 2025, EKN and SEK—agencies that had previously provided critical credit assurance—jointly filed a police report regarding suspected fraud, according to Dagens Industri. Public reporting has referenced invoices involving a Chinese counterparty among the matters under review.

On November 27, 2025, Deloitte informed the market that, during its audit of the FY25 accounts, it had identified grounds for suspicion of accounting fraud and was legally required to report the matter to prosecutors. Intellego subsequently engaged KPMG to conduct a forensic investigation of its accounting and capital-market communications. (CTM Déjà vu?). On January 15, 2026 Intellego highlighted that: “Based on what we have seen so far, we believe it is fair to say that most and perhaps all our revenue transactions and cash flow in 2025 are suspect.”

In the period preceding the arrest, the finance function experienced rapid senior turnover:

Petra Olofsson (CFO): Exited after less than 1 year.

Hans Denovan (CFO): Lasted approximately 2 months.

2. The “Tech” Moat vs. Cash Flow Reality

Intellego reported gross margins exceeding 80%—levels more typical of high-margin software businesses than industrial manufacturers. Management attributed these economics to a purportedly world-leading patented photochromic ink and to arbitrage opportunities, claiming the ability to source disinfection devices in one region and resell them in another at 4–5× markups.

The Commercial Reality: The company announced a $360 million+ contract with Chinese giant Yuwell. However, Yuwell explicitly denied the existence of a “minimum purchase” commitment, stating the deal was subject to actual business volumes.

At the same time, China’s regulatory trajectory under the Minamata Convention is accelerating the transition away from mercury-based products. Domestic regulations prohibit the manufacture of mercury thermometers from 1 January 2026, reinforcing the broader phase-out of mercury in healthcare applications. In UV disinfection and lighting, low-pressure mercury lamps are expected to be progressively displaced through the mid-to-late 2020s, as procurement standards and regulatory guidance increasingly favor mercury-free technologies. The replacement pathway is converging on UVC LEDs, pulsed xenon, and excimer (far-UVC) systems, with UVC LEDs currently the most commercially mature and scalable alternative.

Cash Flow Divergence: Receivables increased sharply, a pattern that warrants scrutiny under common revenue-recognition risk frameworks. The company also relied heavily on factoring to generate the appearance of positive operating cash flow.

3. Irreconcilable Accounts & Ghost Offices

Forensic diligence in China dismantled the operational narrative.

The Phantom Workforce: Chinese filings showed zero social-security contributions by Intellego’s subsidiary between 2021 and 2024. Under Chinese law, this indicates the absence of legally registered employees.

Physical Verification: The purported “operational headquarters” in Shanghai was found locked during business hours.

Conclusion: The Oxygen of Truth

Corporate failures are rarely sudden. They emerge through the accumulation of discrepancies.

For investors seeking long-term outperformance, verification must take precedence over trust. A “ghost office” may simply be the physical manifestation of “ghost revenue” on the financial statements.

When a charismatic management team asks investors to believe in a platform generating margins far above industry norms—while CFOs keeps quitting and reported cash earns no return—the prudent response is to follow the cash.

Earnings are opinion.

Cash is fact.

Everything else is narrative.

Trust the ledger, not the legend.

The Rarity of Validation

Each year, the financial industry produces vast volumes of research. Truly differentiated fundamental analysis—particularly work grounded in forensic analysis rather than narrative extrapolation—remains rare.

Our approach is informed by decades of institutional investment experience across multiple markets and geographies, with a particular focus on bridging Eastern and Western capital market insights. This perspective allows us to identify both structural opportunities and risks that are often obscured by jurisdictional complexity, accounting opacity, or market-specific norms.

In a limited number of cases, our publicly released research has been followed by material regulatory or legal developments involving the issuers examined. Outcomes of this nature are uncommon and serve to reinforce the central principle of our work: verification must take precedence over narrative.

We are open to confidential dialogue with qualified professional investors and allocators interested in our research process, forensic discipline, and its application to identifying asymmetric risk-reward opportunities.

To connect, please contact: admin@maiuspartners.com