What’s Really Behind Intellego’s China Growth Story?

A Forensic Look at Intellego’s Yuwell Partnership and the Reality on the Ground

Disclaimer:

We may hold a short position in Intellego Technologies AB at the time of publication and may adjust our position at any time without notice. This article is for informational purposes only and does not constitute investment advice. All views expressed are the authors’ own and are based on publicly available information and fieldwork conducted by Maius Partners. We do not represent that the information is accurate or complete, and it should not be relied upon as such. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decision.

Author’s note: This report should be read as background information for a better understanding of our research process and the level of on-the-ground insights we are capable of generating, while providing a glimpse into Intellego’s China business. It is not intended as a detailed investment thesis on the parent company, Intellego Technologies AB.

This Research note is divided into four parts. Firstly, we will give an overview of Yuwell, Intellego’s largest Chinese partner, followed by a detailed forensic analysis and site visit of Intellego’s China business. We will then test Intellego’s products against the competition. Lastly, based on our research, we have compiled a list of key questions that we believe long-term investors and other vested interests should ask Intellego’s management to gain a deeper understanding of the business.

Overview of Yuwell and Zhongyou Medical (Likang)

Yuwell (officially Jiangsu Yuyue Medical Equipment & Supply Co., Ltd., SZ:002223) is a leading Chinese medical device manufacturer, generating over US$1 billion in revenue in 2024. The company’s core business spans the research, development, manufacturing, and sales of medical devices and related solutions, with a broad portfolio encompassing respiratory treatment, diabetes management, and other healthcare products.

To broaden its portfolio, Yuwell expanded into infection control and disinfection by acquiring Shanghai Zhongyou Medical High-Tech Co., Ltd. (commonly referred to as Zhongyou by Yuwell, or Likang by Intellego) in 2017. Yuwell initially bought a 61.6% stake in Zhongyou for ¥863 million in November 2016 and completed a full 100% acquisition by May 2018 (purchasing the remaining 38.4% for ¥537 million). Zhongyou’s business became Yuwell’s “Infection Control Solutions (感染控制解决方案)” segment, which from 2020 to 2023 contributed between ¥7.56–11.84 billion in annual revenues (peaking at ~17% of Yuwell’s sales during the height of pandemic-related demand in 2022). However, this segment saw a sharp decline of 36% in 2023 (down to ¥7.56 billion, ~9.5% of revenue) as pandemic demand waned. In the 2024 annual report1, Yuwell changed its segment reporting, rolling the infection control business into a broader “Clinical Equipment and Rehabilitation Solutions (临床器械及康复解决方案)” category — highlighting the non-core nature of Zhongyou’s business.

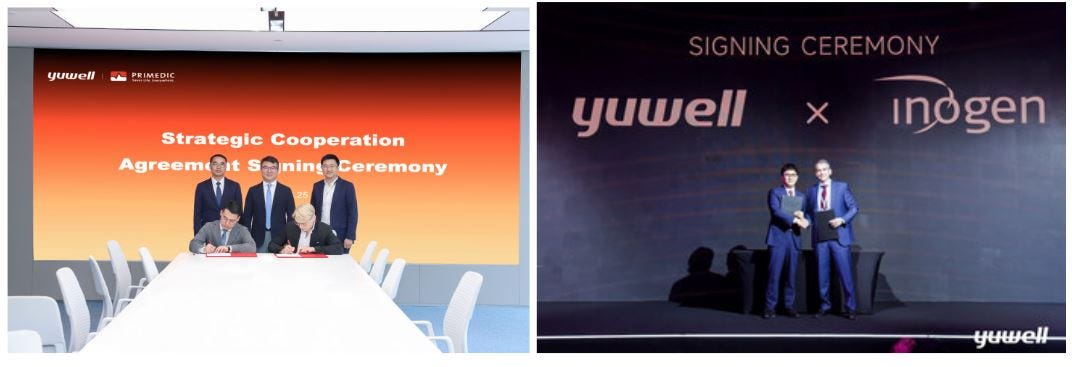

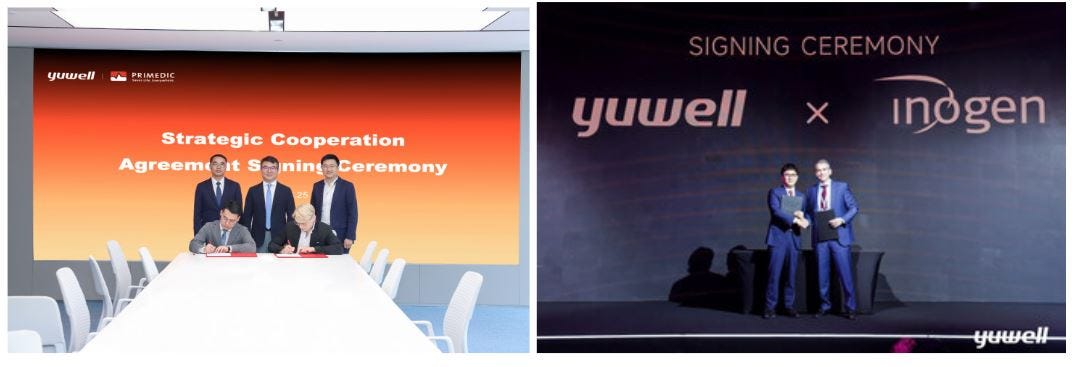

With China’s domestic market growth slowing and fierce competition arising from the government’s volume-based procurement strategy for medical equipment, Yuwell has increasingly focused on international expansion, particularly in the respiratory care space. For example, in January 2025, Yuwell announced2 a strategic partnership with U.S.-based Inogen (Nasdaq: INGN), including a 9.9% equity investment3, and in June 2025, highlighted a German partnership expansion4. This reflects Yuwell’s practice of openly disclosing significant partnerships and global initiatives.

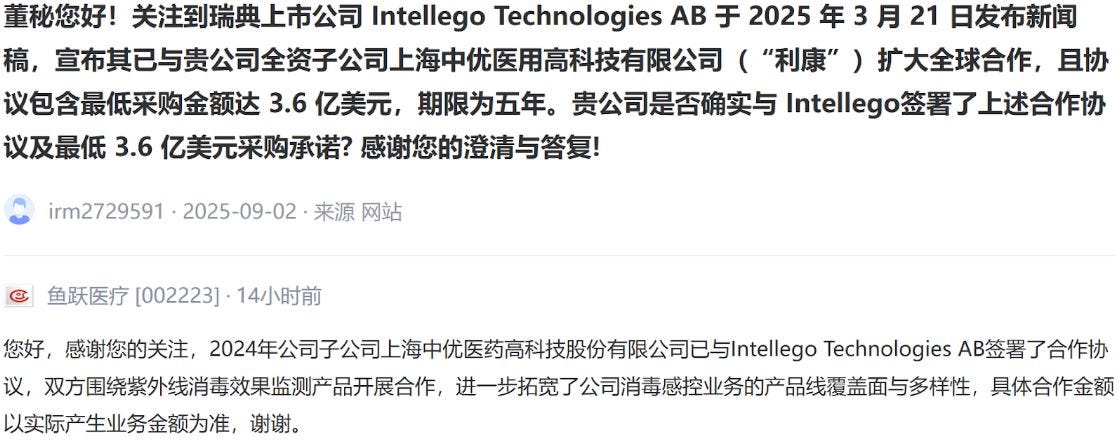

According to China’s Measures for the Administration of Information Disclosure by Listed Companies (上市公司信息披露管理办法), any information or major event likely to significantly impact a listed company’s stock price must be disclosed promptly. Intellego’s March 2025 press announcement5 of a contract valued at up to USD $1.4 billion would be monumentally significant even for Yuwell, which generated about USD $1 billion in total revenue in 2024. Such a deal would represent over 130% of Yuwell’s entire annual revenue, making it unequivocally material and subject to immediate disclosure by Yuwell if true.

To investigate this, we posed a direct question to Yuwell’s management via the Shenzhen Stock Exchange’s investor Q&A platform6: “Has Likang, a subsidiary of Yuwell, signed a 5-year US$360 million minimum purchase agreement with Intellego?”

Author’s note: This Q&A exchange is also accessible directly through Yuwell’s investor relations page7 by navigating to the “投资者交流” section and then the “深交所互动易” (Interactive Q&A) portal.

Yuwell’s official response was:

“In 2024, Yuwell’s subsidiary Shanghai Zhongyou Medical High‑Tech Co. had signed a cooperation agreement with Intellego Technologies AB, as a collaboration around UV disinfection‑efficacy monitoring products. The deal aims to expand Yuwell’s range and diversity of disinfection-related products. The specific cooperation amount is subject to actual business volumes rather than a predetermined figure.”

This reply provides significant insight into the Yuwell–Intellego relationship from Yuwell’s perspective:

Yuwell confirms the partnership: A cooperation agreement does exist between Yuwell’s subsidiary (Zhongyou/Likang) and Intellego, focusing on UV disinfection efficacy monitoring products.

No mention of a “minimum purchase” commitment: Yuwell’s answer pointedly omits any reference to Intellego’s touted USD $360 million minimum contract figure. Instead, it emphasizes that the scale of cooperation depends on actual sales volumes.

Only the 2024 deal is acknowledged: Yuwell references an agreement signed in 2024, with no indication of any expanded or new agreement in 2025. This stands in direct contrast to Intellego’s March 21, 2025, press release, which described a broadened partnership.

As a mainland-listed company, Yuwell is subject to rigorous disclosure obligations. In addition to publishing full statutory filings8, the company provides summaries of investor Q&A interactions and publishes all investor questions and answers online 9. Broker research summaries are also available10. In reviewing Yuwell’s public disclosures, we found multiple references to the Inogen partnership (despite its relatively small current financial impact), yet not a single mention of Intellego — despite Intellego’s reported Q1 2025 Asia revenues suggesting a major contribution to Yuwell’s infection control business.

On Zhongyou’s official website11, the subsidiary outlines its strategic plan for 2023–2027; tellingly, there is no mention of Intellego or ultraviolet disinfection technology. This omission is striking given that Intellego’s purported $360 million deal would imply adding billions of RMB in revenue to that division each year — a highly material addition to its current trajectory.

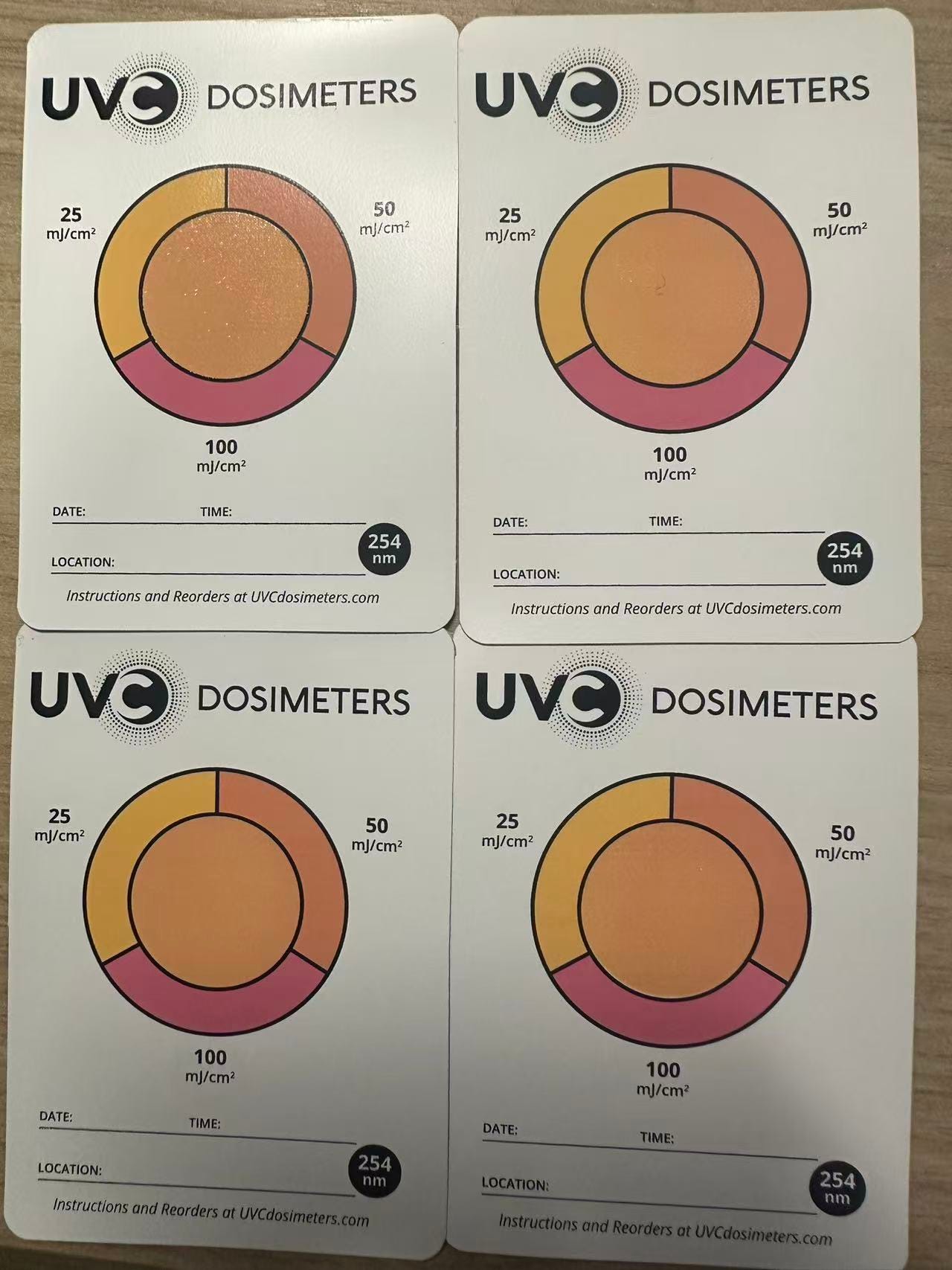

We did find Intellego’s products referenced in one context: they appear briefly in Likang’s 40-page product brochure (Intellego’s UV devices are shown on page 27). In fact, Likang markets two Intellego products in China, each serving a different purpose: Likang UV Intensity Indicator strips and Likang 254 nm UVC Dosimeter cards.

Both products respond to ultraviolet light but measure different things:

The UV intensity indicator shows the instantaneous power of a UV light source at a given moment, expressed in microwatts per square centimeter (µW/cm²). It provides a quick visual confirmation that a UV lamp is emitting at the expected intensity.

The UVC dosimeter, by contrast, measures the cumulative UV exposure (total UV energy over time), expressed in microjoules per square centimeter (µJ/cm²). It records the total dose of UV delivered over a disinfection cycle.

Source: Likang WeChat

In simple terms, intensity tells one how bright the UV is right now, while dose tells one how much total UV energy has been delivered over a period. If the UV intensity is held constant, the total dose can be approximated by the formula: Dose (µJ/cm²) = Intensity (µW/cm²) × Time (seconds). A dosimeter provides a more precise record of total exposure, whereas an intensity indicator is a one-time check of lamp output.

Intellego Technologies China Statutory Filings Analysis

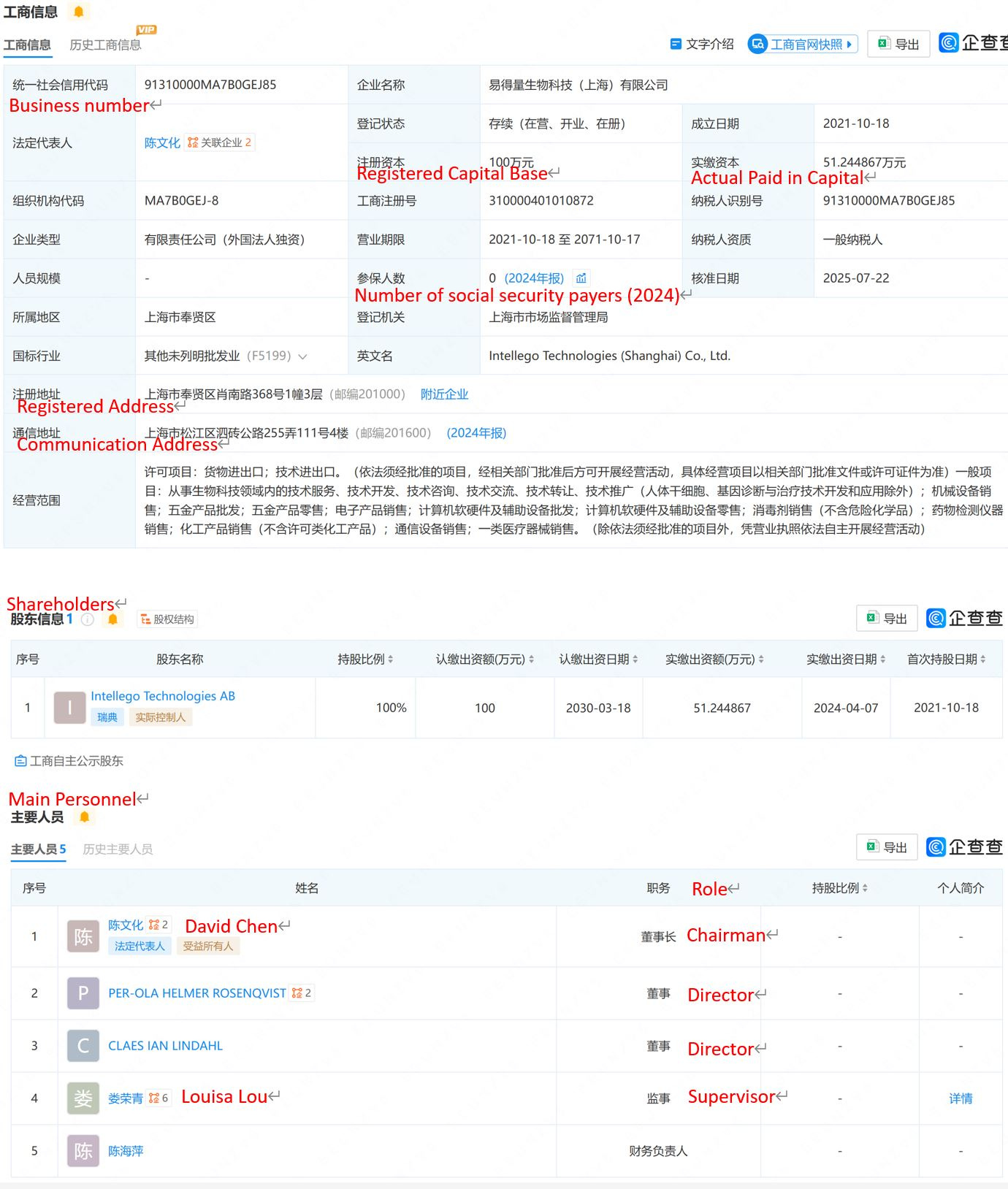

In Intellego’s annual report, the company identifies its primary Chinese subsidiary as Intellego Technologies Co., Ltd. (Shanghai) (上海易得量生物科技有限公司, business registration number 91310000MA7B0GEJ85). We verified this entity through Chinese corporate filings12. However, our analysis of Intellego’s China filings revealed several anomalies:

Board Composition

Mr. Per-Ola Helmer Rosenqvist – a name familiar to the Swedish investment community – is listed as a Director of Intellego Technologies (Shanghai). He also serves as Chairman of ARC Aroma Pure (Shanghai) Co., Ltd., an indirect subsidiary of OptiCept Technologies AB (formerly ArcAroma AB). Notably, Mr. Rosenqvist was a member of Intellego’s Swedish board from 2020 until mid-2023, when he abruptly resigned citing personal reasons13. This departure coincided with his exit from the board of another company (Plexian AB) amid Swedish media reports of an insider trading investigation involving his previous role at SensoDetect AB14. Specifically, Mr. Rosenqvist was accused of purchasing SensoDetect shares just before a major announcement in December 2020 about a distribution deal in China – the kind of price-sensitive information a chairman would likely know ahead of time. Most recently, Mr. Rosenqvist has sold shares in Intellego while appealing charges for gross insider trading (grovt insiderbrott)15. While that case did not involve Intellego directly, we note that Mr. Rosenqvist has also executed trades in Intellego’s stock that were subsequently unwound16. Given this history, we question whether his continued involvement on Intellego’s China board is in the best interest of shareholders from a governance perspective.

Mrs. Louisa “Lou”17 (娄荣青) is listed as a Supervisor (监事) of Intellego (Shanghai) and was, until July 22, 2025, the Legal Representative of the subsidiary. Publicly, Mrs. Lou presents herself as Intellego’s Director of Operations (运营总监), according to a 2023 media interview18. Chinese filings show that Mrs. Lou wears many hats: besides her Intellego role, she is a Director of ARC Aroma Pure (Shanghai) Co., Ltd.19 – again linking her to Mr. Rosenqvist’s business network – and she is the controlling shareholder of Shanghai EAG-METAL Industrial Co., Ltd.20 , a company we will discuss later. Putting aside the ArcAroma connection, one might ask how the COO of a supposedly high-growth Swedish company (with claimed multi-hundred-million-dollar deals in China) has the capacity to concurrently hold two other significant positions outside of Intellego.

It’s worth noting how powerful the “Legal Representative” position is in China. Unlike a Western chairman, the legal representative’s signature can bind the entire company, open and control bank accounts, and represent the firm in legal matters. This authority comes with personal risk: if the company violates laws or defaults, the legal representative can face penalties or travel bans. Thus, changes in this role are often telling. In Intellego’s case, it’s notable that the legal representative role was recently transferred from Mrs. Lou to Mr. David Chen (陈文化). Mr. Chen is publicly identified as Intellego’s Managing Director for APAC21 and is now listed as the Chairman of Intellego (Shanghai). According to his LinkedIn profile22, David Chen is a Chinese national who has been based in Shanghai since 2003. The shift of legal representative duties to Mr. Chen suggests a potential change in internal responsibilities or risk management approach within the China business.

Social Security Contributions

Despite Intellego’s much-publicized partnership with Likang, the statutory filings show that Intellego (Shanghai) paid zero social security contributions for any employees from 2021 through 2024. This is highly unusual.

Under China’s Social Insurance Law, every registered company — including wholly foreign-owned enterprises (WFOEs) like Intellego (Shanghai) — is legally required to contribute to social insurance for all its employees. This obligation isn’t optional and cannot be waived by any private agreement. Both David Chen and Louisa Lou have represented themselves as Intellego executives and appear in the subsidiary’s records. As Chinese nationals drawing income from Intellego’s China entity, their compensation (including, for instance, gains from Mr. Chen exercising stock warrants23 ) should be subject to mandatory social insurance and income tax withholding.

Intellego’s complete lack of social insurance payments for any China-based staff contradicts statements made by its CEO in a recent investor presentations24. Around the 4:40 mark of that presentation:

“We are a very global company... we have subsidiaries pretty much all over the world. Um, in the UK, the US, and in China, where we also have our own staff.” - Claes Lindahl

If Intellego indeed has “its own staff” in China, it is puzzling that none of them appear on the social insurance rolls. (For context, we checked companies associated with Intellego’s China leadership: both EAG-METAL and ARC Aroma Pure have each made social insurance contributions for at least one employee every year since 2017, according to their filings.)

Business Contact Analysis

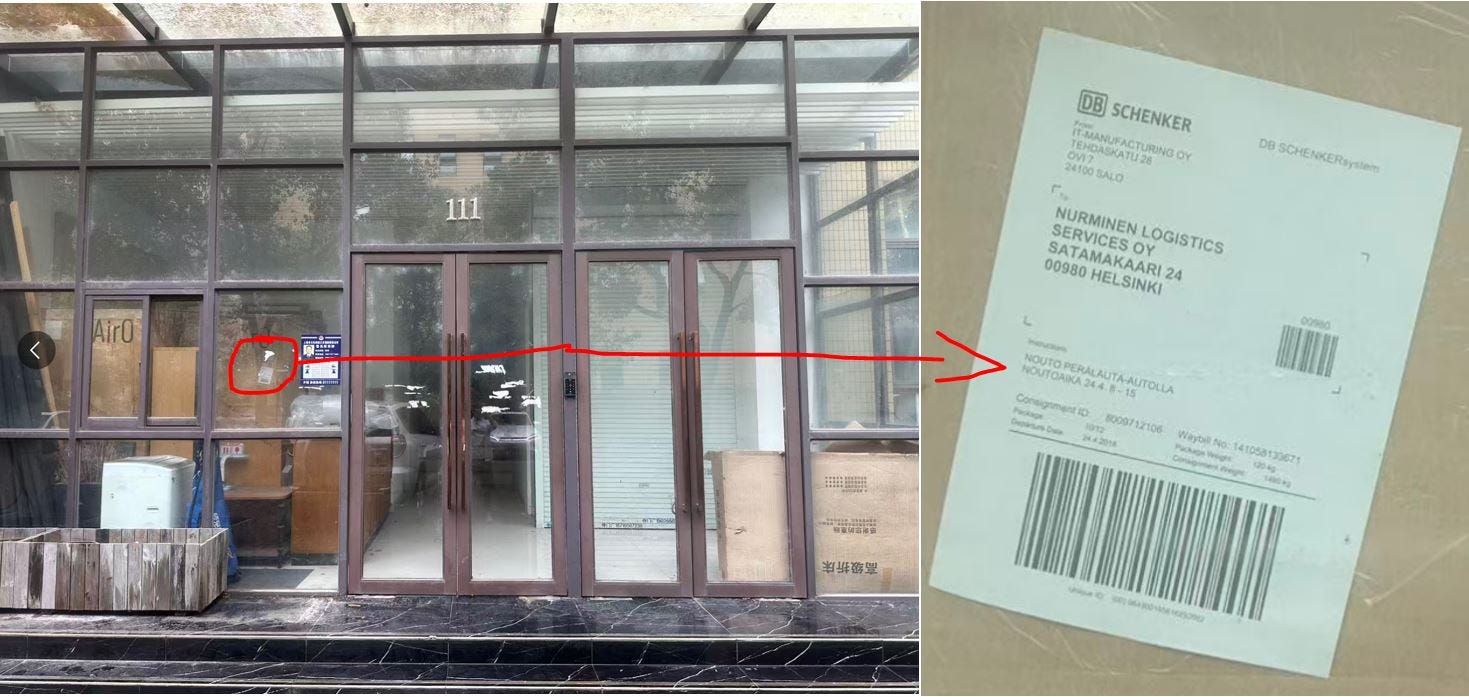

Intellego (Shanghai) lists two addresses in its corporate filings. One is the original registered address in Shanghai’s Fengxian District (肖南路368号, Building 1, 3rd Floor). The other is a communication address in Songjiang District (泗砖公路255弄111号4楼, which we’ll call the “111 address”). We found that the Fengxian “368” location is essentially a mass-registration site — over 10,000 companies are registered at that address. In contrast, Intellego appears to be the only company using the specific “111” address in Songjiang. This suggests that the “111” location is the actual operating office for Intellego’s Shanghai subsidiary.

Moreover, Intellego (Shanghai) shares the same contact phone number and email address with two other companies: ARC Aroma Pure (Shanghai) Co., Ltd., and Shanghai EAG-METAL Industrial Co., Ltd. All three list louisa@eag-metal.com as their contact email and have the same phone number on record. Historical records indicate that this email belongs to Mrs. Lou’s company (EAG-METAL) and started appearing in Intellego’s filings around the time the subsidiary was founded in 2021.

Although the eag-metal.com website is currently offline, an archived version25 identified Mrs. Lou as the Sales Director for a Finnish air purification startup called Air0. Regulatory filings for Air0 show it generated roughly €282,700 in revenue in 202426 and has been consistently loss-making. Air0’s official site still lists Louisa as a distributor in Shanghai27.

Our team visited the “111” Songjiang address during a normal workday. The office was locked, and through the glass we observed boxes of Air0 products (shipped from Helsinki) on the premises. This on-site observation underscores that Intellego’s key individuals in China are closely involved with other ventures (like Air0 and EAG-METAL), raising questions about their focus and potential conflicts of interest.

Registered Capital Base

Chinese company law distinguishes between Registered Capital (注册资本) and Paid-in Capital (实缴资本). Registered capital is the amount shareholders commit to contributing to the company (recorded with regulators), while paid-in capital is what has actually been contributed to date. If paid-in capital lags far behind registered capital, Chinese law typically requires the shortfall to be paid in within a certain period (often within 5 years of establishment), or the company and its owners can face penalties.

Intellego Technologies (Shanghai) was established on October 18, 2021, with a registered capital of ¥1 million (around SEK 1.3 million). As of the latest filings, only ¥0.51 million of that capital had actually been paid in, despite the subsidiary being nearly four years old and Intellego claiming substantial sales into China starting in 2023. In other words, almost half of the pledged capital remains unpaid, even as Intellego touts major business growth in China.

This minimal capitalization – and the failure to fully fund even that small amount – raises a red flag. It prompts a fundamental question: Why would any reputable partner (let alone a large, publicly listed Chinese company like Yuwell) commit to hundreds of millions of dollars in purchases from a local entity that has so little capital invested? The stark contrast between Intellego’s grand announcements (of massive China deals) and the modest reality of its China subsidiary (in terms of capital, staffing, and operations) is difficult to reconcile. For investors and stakeholders, this discrepancy warrants close scrutiny and healthy skepticism.

Reception of Intellego’s Products in China

Intellego has made appearances at major trade shows in China, including:

June 2023 (WIETEC, Shanghai): Intellego’s subsidiary Daro presented at the WIETEC environmental technology conference28.

November 2023 (China International Import Expo, Shanghai): Intellego participated in the CIIE trade fair29.

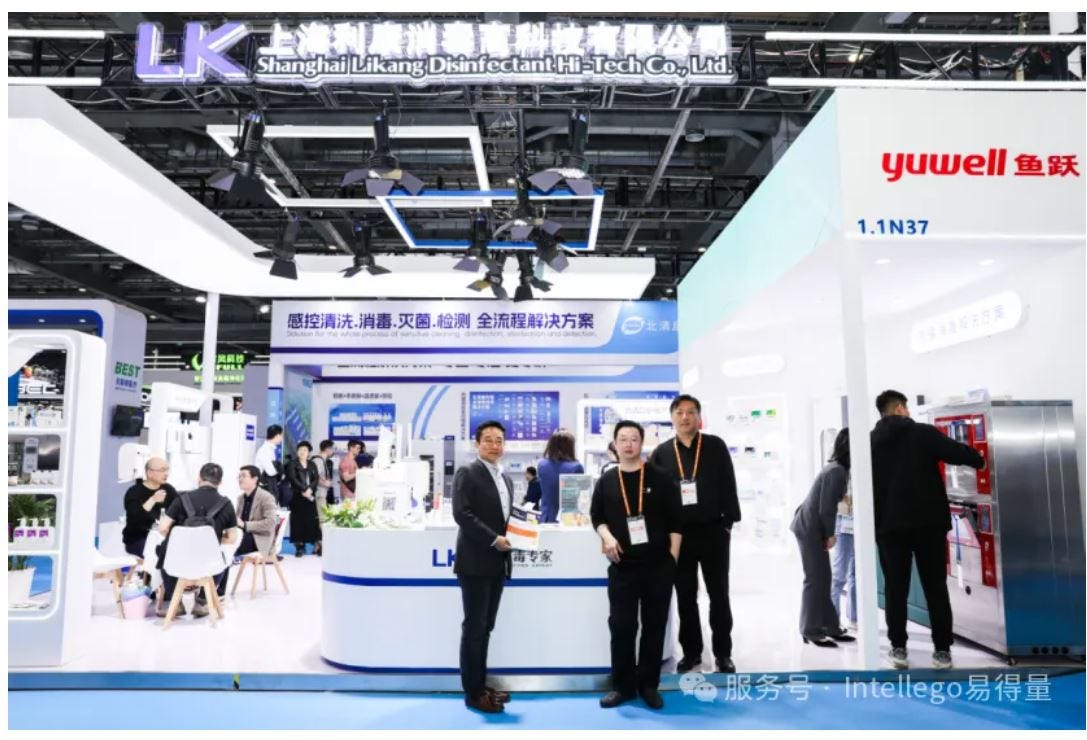

April 2025 (China International Medical Equipment Fair, Shanghai): Intellego’s products were showcased at CMEF, occupying a small part of Likang’s booth space30. Intellego’s CEO, Claes Lindahl, highlighted this event on social media; however, we view Intellego’s CMEF presence as a routine marketing effort, in contrast to the high-profile partnership signing ceremonies that Yuwell typically holds for significant deals3132. (This is despite Intellego’s arrangement with Likang likely being more financially material than some of Yuwell’s heavily publicized collaborations.)

Source: Intellego Wechat

Formal Yuwell Signing Ceremonies with Inogen and Primedic

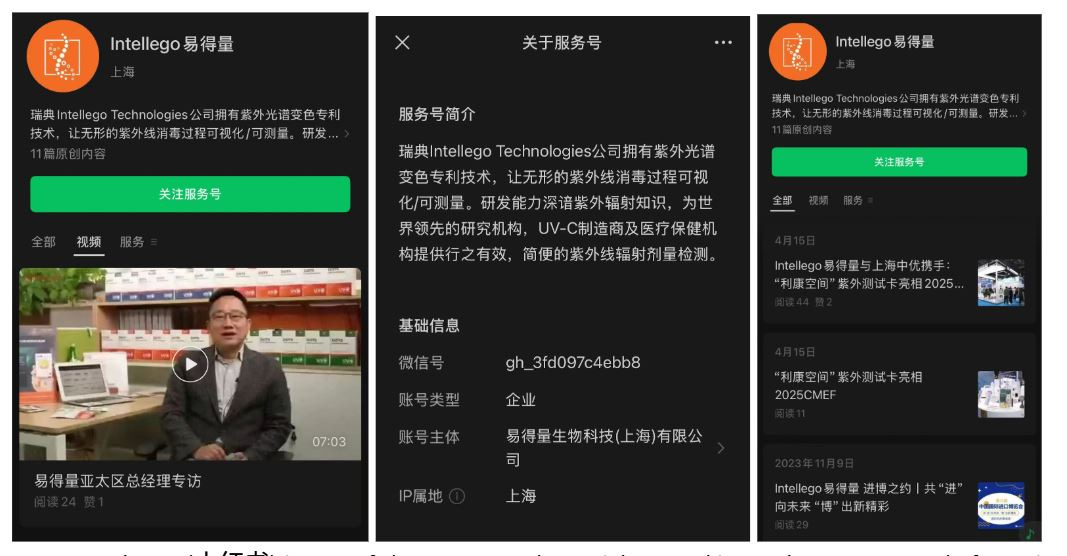

Despite these trade show appearances, Intellego maintains a very low profile in Chinese media and online platforms. Intellego China’s official social media presence is limited to a WeChat account (“Intellego 易得量”) linked to its Shanghai subsidiary (易得量生物科技(上海)有限公司). Notably, none of Intellego China’s 11 WeChat posts have garnered more than 100 views. For example, a seven-minute interview with Intellego’s Asia Managing Director, David Chen, has only about two dozen views since its 2023 release.

We also searched for Intellego on RedNote (小红书, Xiaohongshu), one of China’s most popular social media and e-commerce platforms for user reviews and product discovery. We did not find a single mention of Intellego’s products on RedNote, even though we found numerous reviews for competing UV indicator products.

In terms of e-commerce presence, China’s market is highly digital — nearly 30% of retail sales occur online. While distribution of healthcare equipment into hospitals typically happens offline, Chinese regulation means hospitals are subject to a highly competitive tender process known as “volume-based procurement (VoBP)”, depressing margins and profits for product manufacturers and distributors.

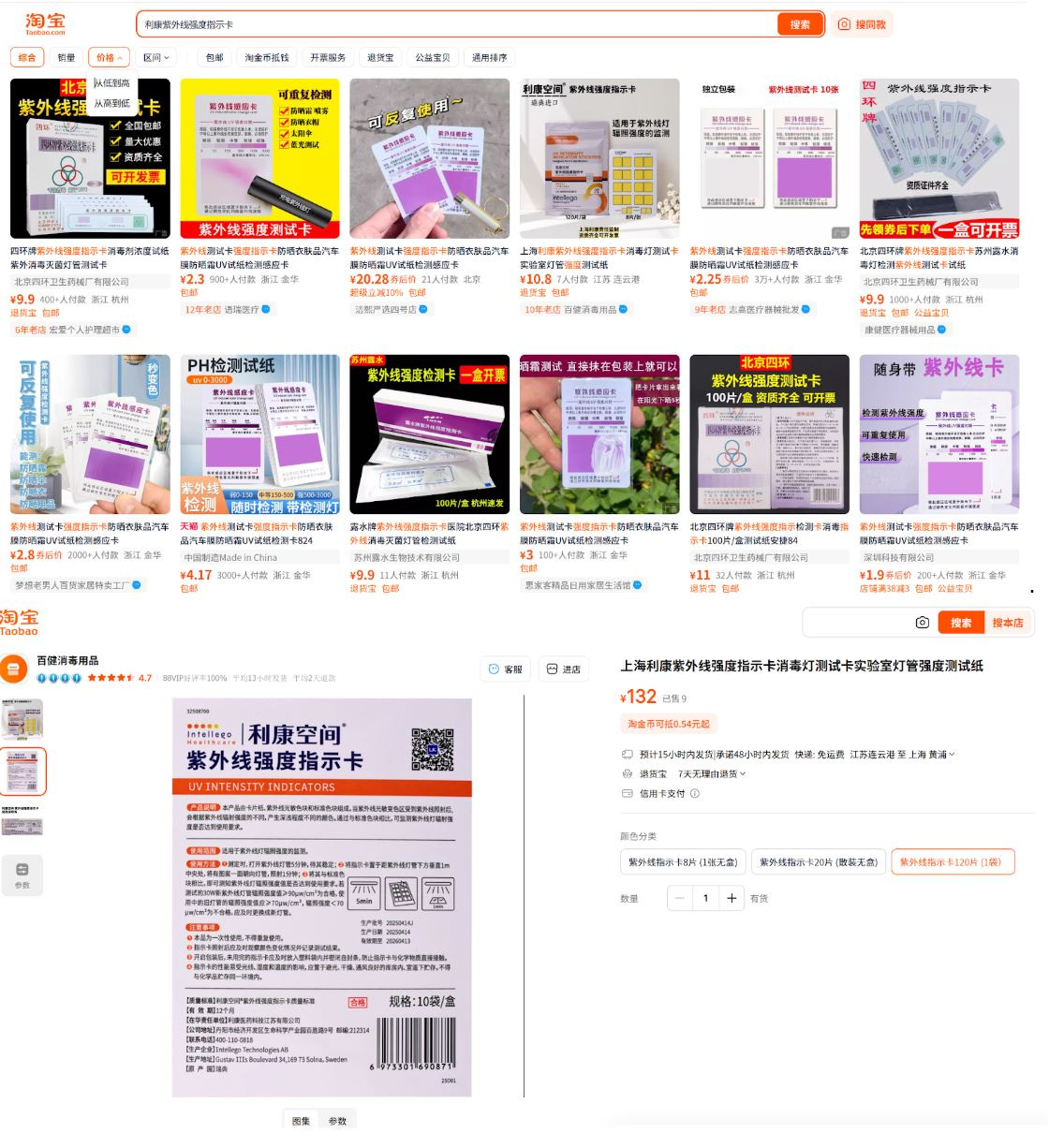

If a product has any traction, it is usually available through online marketplaces. However, among the many UV disinfection indicator products listed on major Chinese e-commerce sites, we found only one online store offering Likang’s UV intensity indicator strips, with a total of just nine recorded sales 33. Furthermore, we found no online listings for Likang-branded 254 nm UVC dosimeter cards.

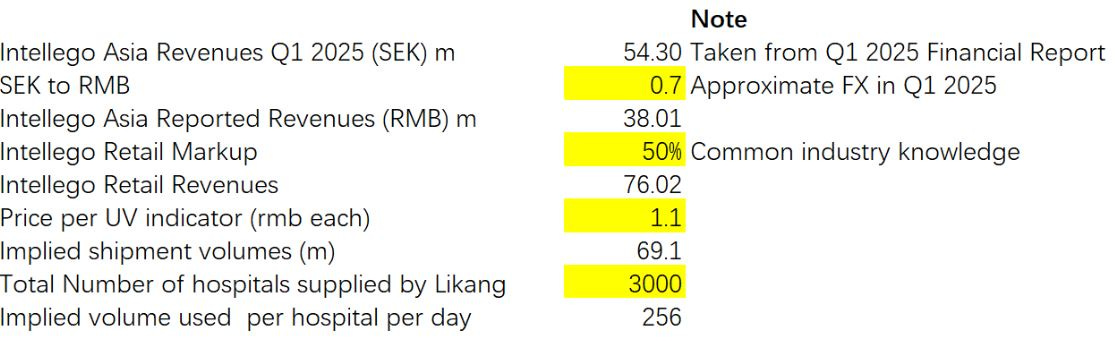

This lone online store listing provided some revealing details. The manufacturing address for the Likang UV intensity indicator is given as “Gustav III:s Boulevard 34” in Sweden — an address we recognize as a shared office space, not a manufacturing facility. (Intellego’s Nasdaq First North listing prospectus 34 notes that Stema Specialtryck AB in Borås produces Intellego’s dosimeters and indicators, while Bio-Hospital AB in Kopparberg produces the chemical indicator ink.) Crucially, the retail price listed for Intellego’s UV intensity indicator in China is about ¥1.1 per strip (approximately US$0.15).

To put Intellego’s reported sales into perspective: the company reported SEK 54.3 million in Asia revenues for Q1 2025. If those revenues came primarily from selling UV indicator strips, it would require an enormous volume of strips to be sold and used. By our estimates, hundreds of indicator strips would have to be consumed per day at each of Likang’s ~3,000 hospital clients to reach that revenue figure. Such usage would make Intellego’s indicators one of the most widely used daily consumables in those hospitals. Yet, tellingly, as of our research, Likang’s own official product webpage35 does not list Intellego’s UV indicators or dosimeters for sale at all.

Product Review and Comparison

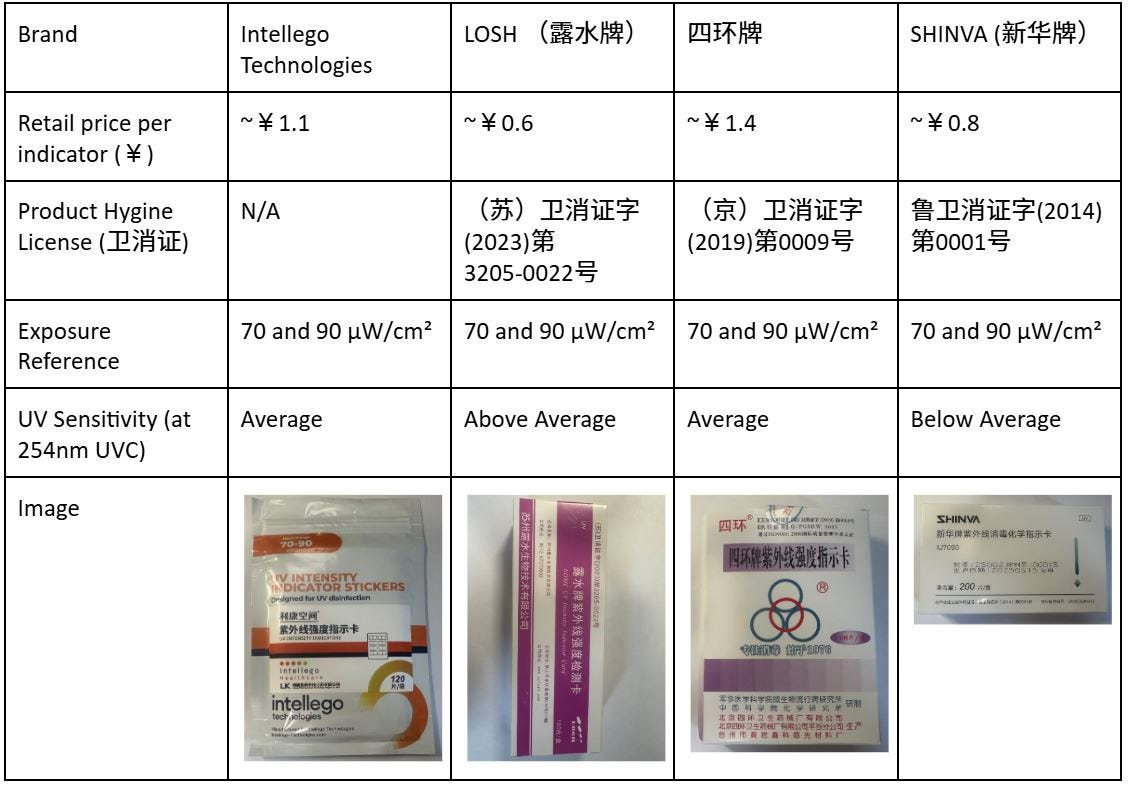

Our investigators obtained multiple single-use UV intensity indicator samples available in the Chinese market and compared them to Intellego’s China-sold UV intensity indicator. The competing products we tested included brands such as LOSH (露水牌), Four Rings (四环牌), and SHINVA (新华牌). Below is a summary of how Intellego’s indicator stacks up:

Our investigators observed that Intellego’s UV indicator (the Likang version we obtained was manufactured in April 2025) lacked a hygiene license number on its packaging. Under China’s disinfection product regulations, a dual-track system exists for product approval36. Historically, all disinfection products needed a Product Hygiene License to be sold. Recent regulations allow that only “new” disinfection products — those using novel materials, technologies, or sterilization methods — must go through the stringent national registration to obtain a license. “Existing” or well-established product types can instead undergo a safety and efficacy evaluation and then simply file the product with provincial authorities.

Further, the sample we obtained was printed in English, with a Chinese Likang sticker overlay on top, contrasting with a publicly rendered image of a fully Chinese product.

Upon our inquiry, Yuwell’s management confirmed that Intellego’s product has a safety and efficacy evaluation on file, instead of a hygiene license 37. In other words, Intellego’s UV intensity indicator is being sold via the filing pathway as an “existing” product, not as a “new” product that requires special approval. This implies that Chinese health regulators do not view Intellego’s UV intensity indicator as a novel technology.

As highlighted earlier, the primary benefit of a dosimeter (which measures accumulated dose) over a simple intensity indicator is greater accuracy in gauging total exposure. We obtained Intellego’s 254 nm UVC dosimeter card (through a non-Likang channel) and tested it against two professional-grade Lishang UVC radiometers38 that are specifically calibrated to Chinese national standards.

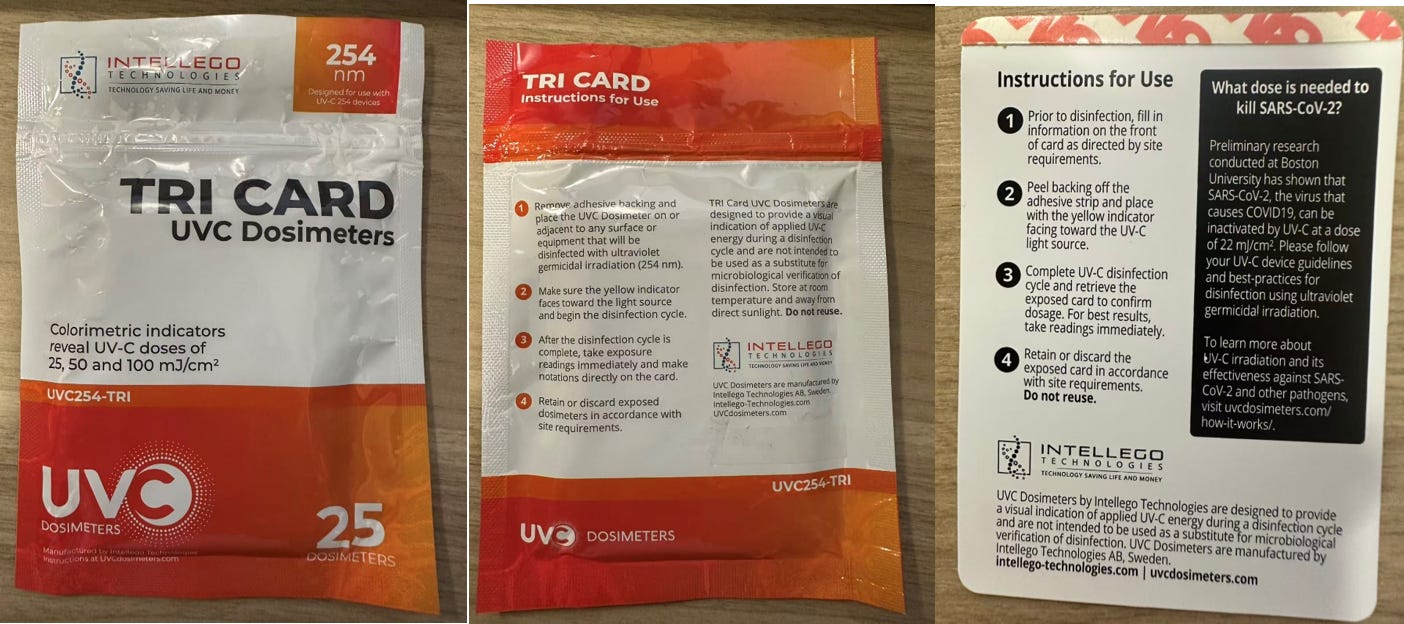

In contrast to the UV intensity indicators, the UVC dosimeters do not list a manufacturing address at all, only stating that the product is manufactured by Intellego Technologies AB. The markings on the back of the dosimeter would suggest one of its key use cases is surrounding disinfection related to COVID.

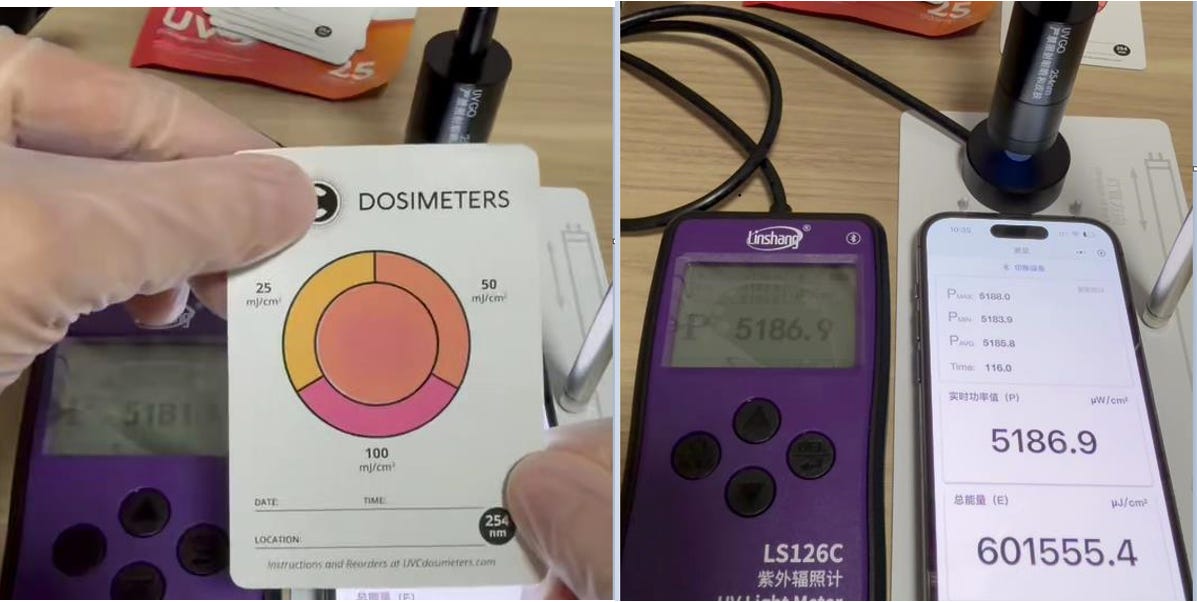

To evaluate the performance of Intellego’s UVC dosimeter, we conducted controlled exposure tests using a calibrated 254 nm UV-C light source. The dosimeters were subjected to two intensity settings — 500 µW/cm² and 1,000 µW/cm² — for 200 and 100 seconds, respectively, corresponding to a total UV dose of approximately 100 mJ/cm². According to Intellego’s own specifications, this dose should trigger a distinct bright pink color change, indicating full saturation.

However, in our trials, the dosimeter turned only orange, not pink, suggesting that it responded as if exposed to less than half the intended dose (~50 mJ/cm²). We repeated the experiment under identical conditions using two independent, calibrated radiometers to verify accuracy, as shown in the videos below. The results were consistent across both devices. Based on this controlled setup and repeated validation, we conclude that the Intellego UVC dosimeters we acquired (packaged June 2025) exhibit significantly lower sensitivity than the company’s stated performance standards.

In a separate observation, we continued exposing the dosimeter until it reached its pink end-point, which according to Intellego’s specifications corresponds to 100 mJ/cm² of UV-C exposure. We recorded the exposure duration and verified the cumulative energy using our radiometer. The radiometer measured a total dose exceeding 600,000 µJ/cm² (≈600 mJ/cm²) — more than five times higher than the level indicated by the dosimeter.

This lack of sensitivity is more than a technical flaw — it carries significant real-world safety implications. In medical environments, overexposure to UV light can be hazardous: many instruments contain plastic or polymer components that degrade (photodegrade) when exposed to excessive UV radiation. If Intellego’s indicators and dosimeters under-report actual UV exposure, users may unknowingly extend sterilization times or increase intensity, risking equipment damage and compromising safety protocols.

The fundamental advantage of using a dosimeter over a cheaper intensity sticker lies in its supposed accuracy — its ability to measure cumulative exposure precisely. But if that accuracy is unreliable, the rationale collapses. In such cases, practitioners would be better served either by using a calibrated radiometer for precision or by approximating exposure through a simple intensity indicator, rendering the dosimeter’s added cost and complexity effectively obsolete.

Questions for Intellego Management

Board and Governance: How does the Intellego China Board assess potential business risks while operating in a high-risk jurisdiction like China? How does having Mr. Per-Ola Helmer Rosenqvist and his close associate, Louisa Lou, on the Intellego China board benefit minority shareholders, given Mr. Rosenqvist’s historical track record and Louisa Lou’s multiple roles?

Partnership Discrepancies: Why is the language publicly used by Yuwell substantially different from the language in Intellego’s press releases? Specifically, why does Yuwell not acknowledge the $360 million minimum commitment or the March 2025 expanded partnership in its public statements about Intellego?

Local Operations: Where is the actual office location of Intellego’s China operations, and how many employees does Intellego actually have on the ground? How does Intellego ensure appropriate compliance with all relevant Chinese law (including social security contributions and all relevant tax withholdings) is being correctly accounted for in these operations?

Product Manufacturing and Quality: Where are Intellego’s UVC dosimeters and UV intensity indicators manufactured, and what quality control processes are in place to ensure these products are correctly calibrated and meet Chinese regulatory standards?

Conclusion: Lessons from the Intellego Case

Our investigation into Intellego’s China operations illustrates a broader truth about investing in cross-border narratives: stories travel faster than facts. What begins as a bold headline — “a billion-dollar China partnership” — can, upon closer inspection, unravel into a web of partial truths, mismatched disclosures, and governance inconsistencies.

We view such discrepancies not as anomalies, but as data points — evidence of how information asymmetry and narrative friction can create both risk and opportunity. This case reinforces the importance of first-hand research, especially for companies that have substantial exposure to opaque markets, where disclosure standards, cultural norms, and regulations vary widely.

Three lessons stand out:

Trust must be earned twice — once through transparent disclosure and again through consistent execution. When partners’ public statements diverge, investors should pause and ask why.

Governance is a leading indicator of durability. The strength of a company’s oversight, incentives, and compliance infrastructure often determines whether its growth is sustainable or fleeting.

Forensic curiosity creates an edge. Sustainable long-term investment edge rarely comes from faster data; it comes from deep insights — from walking factory floors, reading local filings, and asking uncomfortable questions.

In this sense, the Intellego story is less about one company and more about a principle: that sound investing requires alignment between narrative and reality. For long-term investors, the task is not simply to find growth, but to verify it — to seek not the most optimistic story, but the truest one.

At Maius Partners, our mission is to bridge global capital with local insight — to uncover what’s real beneath what’s told.

Like what you read or have a tip? You can contact us at admin@maiuspartners.com

https://file.finance.sina.com.cn/211.154.219.97:9494/MRGG/CNSESZ_STOCK/2025/2025-4/2025-04-26/11007099.PDF

https://www.szse.cn/disclosure/listed/bulletinDetail/index.html?796007a5-7a88-4c89-b20c-c64935b69f9a

https://investor.inogen.com/news-events/press-releases/detail/241/inogen-expands-product-portfolio-global-reach-and

https://www.prnewswire.com/news-releases/yuwell-primedic-global-partners-conference-held-in-germany---signs-strategic-agreement-with-safe-life-to-expand-global-first-aid-market-302473209.html

https://intellego-technologies.com/mfn_news/intellego-and-shanghai-zhongyou-medical-high-tech-co-ltd-likang-expands-collaboration-in-new-360-million-14-billion-usd-deal-over-five-years-in-the-asian-market-outside-of-china/

https://irm.cninfo.com.cn/ircs/question/questionDetail?questionId=2079341339602681856

https://www.yuwell.com/aid?switchover=0

https://www.szse.cn/disclosure/listed/notice/index.html?stock=002223

https://irm.cninfo.com.cn/ircs/company/companyDetail?stockcode=002223&orgId=9900004462

https://stock.finance.sina.com.cn/stock/go.php/vReport_List/kind/search/index.phtml?t1=2&symbol=002223

http://zonyou.cn/#/page/index/index?id=17

https://www.qcc.com/firm/2cd5226ae1aff8b3268d19a2ad8c4e11.html

https://intellego-technologies.com/mfn_news/per-ola-rosenqvist-har-begart-uttrade-fran-intellego-technologies-styrelse-pa-grund-av-personliga-skal/#:~:text=Per,tidigare%20var%20styrelseordf%C3%B6rande%20i%20Intellego

https://www.affarsvarlden.se/artikel/per-ola-rosenqvist-lamnar-plexian-och-intellego-misstankt-for-grovt-insiderbrott-enligt-di

https://www.di.se/live/tidigare-storagare-har-storsalt-i-intellego/

https://intellego-technologies.com/mfn_news/intellego-informerar-om-styrelsemedlems-aktieaffarer/#:~:text=Intellego%20Technologies%20AB%20,i%20Intellegos%20styrelse%20sedan%202020

https://www.qcc.com/pl/p9dd7ce9b22f1f8c8645933c6bd7ed30.html

https://js.cnr.cn/kjjr/20230714/t20230714_526328734.shtml

https://www.qcc.com/firm/8209a15e764db7fa60476b6d5fb782b9.html

https://www.qcc.com/firm/993c43310045faebd6bbd92ab47f5524.html

https://intellego-technologies.com/intellego-technologies-selects-david-chen-to-lead-asia-pacific-operations/

https://www.linkedin.com/in/david-chen-0527b7163/

https://intellego-technologies.com/mfn_news/intellegos-managing-director-asia-pacific-david-chen-exercises-warrants-and-intellego-receives-approximately-sek-2-2-million/

https://us02web.zoom.us/rec/play/vENTq0idPmhEY3ccVN1LEQ3rPxVyJVSBTuA9hM4auOAlsWfPVWGsFNUDd2kxg2usRSE8SHkCTnLk3jew.YSBztV4XTqDhNGQ7?eagerLoadZvaPages=sidemenu.billing.plan_management&accessLevel=meeting&canPlayFromShare=true&from=share_recording_detail&continueMode=true&componentName=rec-play&originRequestUrl=https%3A%2F%2Fus02web.zoom.us%2Frec%2Fshare%2FdnKMBTVn6vpDf-X75Ttw4bt_q_-ncMJbj8Us0mIqLri_TBCVtyQfi2EwTrvfgiIF.Qp5mc8wB2DSfq-58

https://web.archive.org/web/20220112164054/http://eag-metal.com/about-us/index.html

https://haku.vainu.com/company/air0-oy-taloustiedot-ja-liikevaihto/FI25880198/yritystiedot

https://air0.fi/zh/contact-ch/

https://www.prnasia.com/story/406764-1.shtml

https://www.toutiao.com/article/7299771244571247167/?upstream_biz=doubao&source=m_redirect&wid=1757940255470

https://mp.weixin.qq.com/s/B7gU7QTrIR7l7CXBPZxOBA

https://www.primedic.com/en/about-us/news-events/news/details/strategische-partnerschaft/

https://www.prnewswire.com/news-releases/arab-health-2025yuwell-medical-announces-strategic-investment-and-partnership-with-inogen-in-respiratory-health-302360434.html

https://item.taobao.com/item.htm?id=913230454959

https://storage.mfn.se/c998b618-510f-4399-82b4-a989bfab5040/im-intellego-final.pdf

http://zonyou.cn/#/page/index/shop

https://knudsencrc.com/regulatory-analysis/chinas-regulatory-framework-for-disinfection-products/#:~:text=Health%20License%3A%20Issued%20by%20the,Health%20and%20Family%20Planning%20Commission.

https://irm.cninfo.com.cn/ircs/question/questionDetail?questionId=2094918241169592320

https://www.linshangtech.com/product/ls127c-integrated-uv-light-meter.html

Well written. However, the tests in your report were performed totally incorrectly.

You say that you used "a calibrated 254 nm UV-C light source". The videos show that this was a cheap (non-germicidal) LED UVC lamp of the type UVGO that can be bought on eBay: https://www.ebay.com/itm/315790301232

There is no guarantee or proof that this cheap LED was calibrated.

On the other hand, your measuring radiometers were LS126C and LS127C UV Light Meters, calibrated by the manufacturer Linshang specifically for investigation of low-density mercury UV sources, and low-density mercury UV germicidal lamps, respectively: https://www.linshangtech.com/product/LS126C_EN.html

https://www.linshangtech.com/product/ls127c-integrated-uv-light-meter.html

It is known that low-density mercury UV sources have a completely different spectral profile compared to LED UV sources:

https://www.opsytec.com/uv-applications-knowledge/spectral-database-for-uv-lamps-and-uv-leds

Thus their UV intensities/doses must be measured by radiometers calibrated specifically for each type of the lamp.

In summary, your tests performed using Intellego's dosimeters which were previously tested and validated independently by the RISE institute of Sweden, show that indeed, electronic radiometers designed for use with low-density mercury lamps grossly overestimate the dose of UV radiation that LED UV sources produce. This result is not surprising and has nothing to do with the quality of Intellego's dosimeter cards.

Did you contact/listen/read transcripts of recently departed Henkel employees' thoughts on Intellego and its products with which they have firsthand experience?

I realize that Europe (and basically anything non-Asia distribution) isn't the region that you focus on.

China companies violate agreements & contracts oftentimes (and pirating/"fakes" abound), especially with Western companies. This is a sharp contrast to Europe/US contractual norms.