Yonex (TYO:7906) - Playing the Long Game

Japanese Craftsmanship meets American Capitalism

Summary

Yonex Co., Ltd., founded in 1946, has solidified itself as a dominant player in racket sports, particularly in badminton and tennis. Known for its superior craftsmanship, cutting-edge technology, and strategic marketing, Yonex holds a 60%+ global market share in badminton and is rapidly expanding in tennis.

Despite earnings compounding at 40% annually over the past five years, the stock remains undervalued, trading at just 8.5x forward EBITDA. With continued earnings growth projected at ~20% per year, the combination of new leadership with President Mrs. Yoneyama (Founder’s American-educated granddaughter (1)) taking the realms paves the way for improved capital allocation, an activist investor push (2), resulting in recent buybacks (3) and a growing global footprint presents a compelling investment opportunity.

2. Company Overview

Yonex’s history spans over seven decades, during which it has built a robust brand identity associated with excellence in racket sports. The company’s portfolio includes advanced badminton rackets, tennis racket, shuttlecocks, footwear, and sports apparel.

Yonex’s higher purpose mission is to get more people to love sports, which unites people of different ethnicities together and there is no better way than to be in a racket sports game. On the Joe Rogan show, Elon Musk once remarked on the significant health benefits of engaging in racket sports—stating that they can extend life expectancy by up to 9.7 years (4), the longest among any sports.

3. Market Landscape Overview

3.1 Global Market Size and Growth Opportunities

Badminton and Tennis:

The combined market size for both Badminton and Tennis equipment is currently around 5 billion USD and is expected to grow by single digits over the next few years (5) (6). However, in recent decades, Badminton has been increasing faster than Tennis, driven by strong growth out of Asia (China stands out in particular). By contrast, Tennis participation rates have fallen significantly over the decades in the Western world, driven by changes in shifting leisure preferences, albeit this trend appears to have reversed post-COVID as increasingly people focus on health and well-being (7).

While this is not a large total addressable market category like apparel, this also insulates the business from new competition and disruption, as the up-front investment cost required to build a new brand, manufacturing, and distribution capabilities would likely significantly outweigh the benefits when speaking with industry insiders, the only notable new entrant is Apacs in 2002 without much success.

Further, as the cost of a new racket is small relative to the total cost of playing the sport (i.e. $200 racket vs. $40 per hour of court rental or $50 per hour of coaching), the industry has relatively strong pricing power, as evident in Yonex’s nearly 50% gross margins.

3.2 Competitive Landscape and Market Share Insights

Badminton:

Yonex is widely recognized as the dominant player in the badminton market. Other competitors include Victor and Li-Ning. My channel checks suggest Yonex has over 60% market share globally, with Victor having around 20%. At the professional level, it is not uncommon for Yonex to command over 80% market share.

Tennis:

In the tennis segment, the competitive field includes Wilson (~35% market share), Head (~30%), Babolat (~15%), and Yonex. In recent years, Yonex has been gaining significant market share through strategic product launches and increased marketing and collaboration efforts, especially targeting juniors and females.

4. Strategic Analysis: Yonex’s Market Position and Growth Strategy

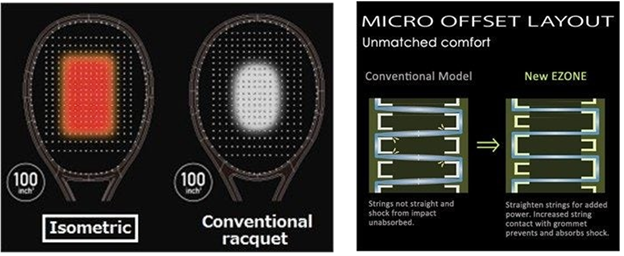

Yonex’s competitive edge lies in its pioneering ISOMETRIC design—which expands the “sweet spot” by 7%, combined with advanced material science, including its integration of advanced materials such as HYPER-MG

and Nanometric composites that enhance power, control, and vibration dampening.

This technological prowess is complemented by its meticulous manufacturing process, with high-end rackets produced in Japan under stringent quality controls and traditional craftsmanship that ensure exceptional consistency and performance. This contrasts with its competitors, who have China-dominated supply chains. On the Q324 Amer results call, Amer Sports highlighted that its Wison business ”segment would be most impacted, predominantly tennis rackets, baseball bats, and basketballs. We have some degree of flexibility to adjust our supply chain, but price increases will be the primary tool we utilize, should tariffs occur.”

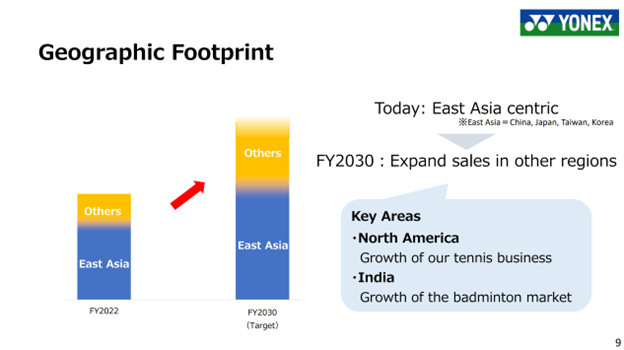

Going forward, the key growth priority will be focused on becoming a more international business, as highlighted in its 2023 strategy day (8), East Asia still dominates its sales, by contrast, the APAC region only accounts for ~13% of Wilson’s revenues (9).

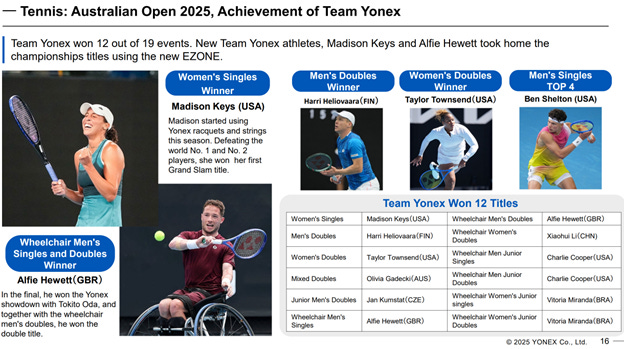

As a testament to Yonex's progress, 19th seed Madison Keys recently won the Australian Open Women’s Singles, defeating both the world No. 1 and No. 2 in back-to-back matches. She had only recently switched to Yonex after her contract with Wilson ended in 2024 (10). Meanwhile, in the Men’s Singles, Ben Shelton reached the semifinals with his Yonex.

Although world No. 1 Novak Djokovic withdrew from the semifinals, it was eye-opening to watch him train with his former rival turned coach, Andy Murray, who had recently retired from professional tennis while sporting a Yonex after claiming “I tried lots of different rackets. I tested them with Hawk-Eye when I was able to and I loved the Yonex (11)”

7. Financial Performance and Outlook

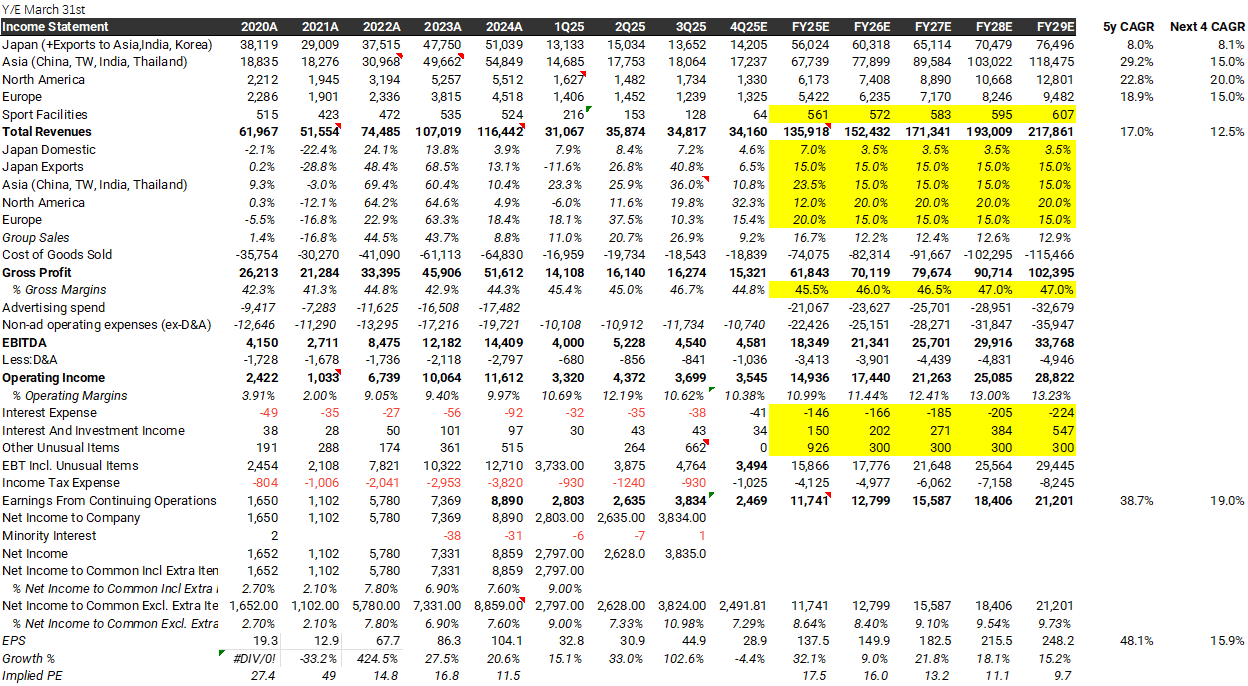

Yonex recently reported its Q325 results (12), with revenues up 27% yoy, including 36% (~30% in RMB terms) in China (~50% of group revenues and ~70% of group profits), this contrasts with Wilsons, reporting only 11% growth for the quarter (13). My channel checks suggest strong sell-through growth in China for Q4 for Yonex.

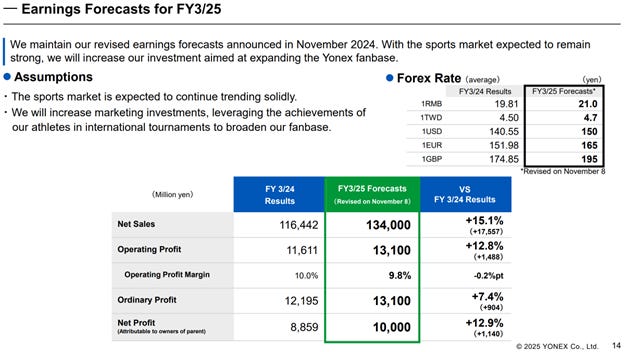

For the full year, Yonex maintained its guidance for 10bn net profit, which was upgraded from 9.3bn at the year half-year result. However, as my modeling below suggests, absent either a disastrous top-line outcome or the company spending significantly more on marketing investments than expected, I believe the company will likely beat earnings by ~10%, paving the way for further upgrades to come.

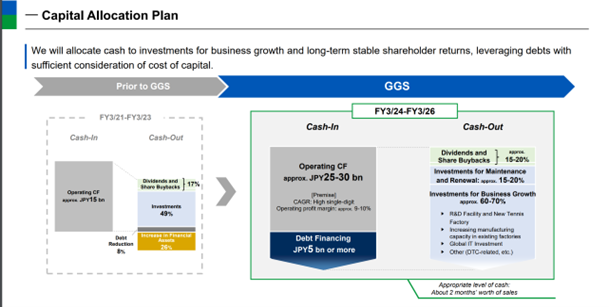

8. Capital Allocation

Being a family-run company, Yonex has historically suffered from poor capital allocation, with a large net cash balance sheet, however more recently the company has made a clear commitment to the market to better return excess cashflows to shareholders, as detailed in its 2023 strategy day.

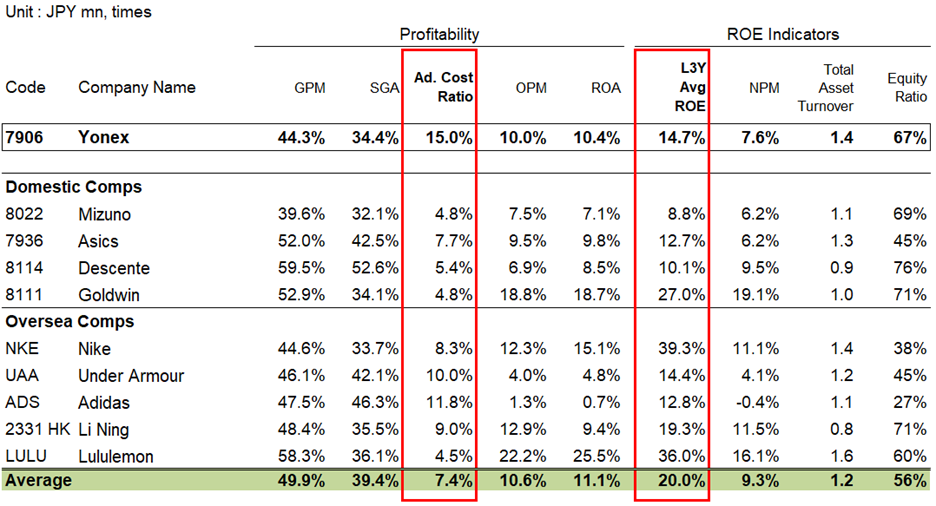

This progress is also carefully being watched by shareholders, with Activist investor Hibiki Path Advisors on board and detailing in its public letter (2) an opportunity to further increase the return on equity, including through the reduction in advertisement cost as a percentage of sales from the current 15% of sales, to peer average of 7.5%.

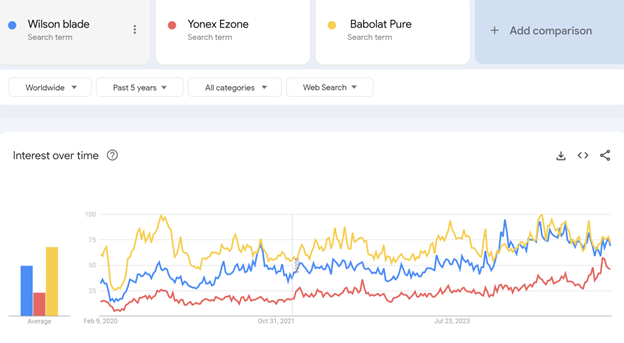

Overall, I believe while there is an opportunity to optimize costs, equally, I agree with management’s view of investing for future growth, especially going after the North American Tennis market, with my analysis suggesting Wilson currently generating over $350m in revenues from Tennis related sales vs. $110m for Yonex. As shown below, Google Trends data suggest there has been a significant recent uptick in interest in Yonex Tennis rackets worldwide.

9. Valuations

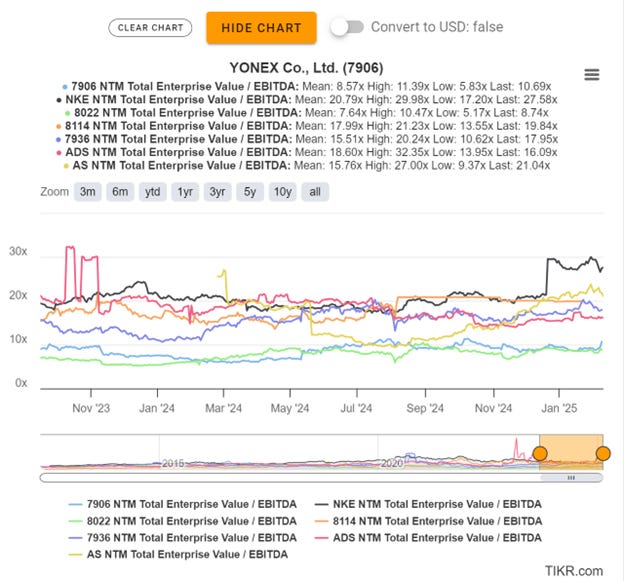

While the valuation in Yonex has increased somewhat recently, I still believe its current forward valuation of ~8.5x my FY26 EBITDA estimate is undemanding relative to peers, which typically trade on 10-20x EBITDA and see significant upside opportunity. With peers trading around 15x+ EBITDA except for 8022 Mizuno, which is a lower gross margin and return business as shown in the comps table below.

Source:

(1)

(2) https://www.hibiki-path-advisors.com/en/engagement/post-7906/

(3) https://www.nasdaq.com/articles/yonex-co-announces-strategic-share-buyback

(4) https://www.instagram.com/crunchtimecoaching/reel/C-ZDLwRAEly/?hl=en

(7) https://www.ustasocal.com/news/surge-in-tennis-participation-led-by-growth-in-diversity/

(8) https://www.yonex.com/media/wysiwyg/07ezone/230517_Global_Growth_Strategy_GGS__240509_.pdf

(9)https://www.sec.gov/Archives/edgar/data/1988894/000110465924001168/tm2322981-10_f1.htm

(10) https://www.benrothenberg.com/p/madison-keys-racket-racquet-yonex-wilson-bjorn-fratangelo-australian-open-max-eisenbud

(11) https://www.theguardian.com/sport/article/2024/may/23/andy-murray-tennis-racket-switch-hunt-for-edge

(12) https://ssl4.eir-parts.net/doc/7906/ir_material_for_fiscal_ym3/172141/00.pdf

(13) https://s203.q4cdn.com/960646696/files/doc_financials/2024/q3/3Q-2024-AS-Slides-FINAL.pdf