The Announcement That Changes Everything

Reassessing China Yuchai Limited from a completely new perspective

Background Intro

Back in February, we first profiled (link) a forgotten China microcap stock: China Yuchai Limited, which was trading well below its intrinsic value. Since then, the stock has doubled, and at its recent highs, tripled. Yet, despite this strong run, we believe the real story is only just beginning.

Successful industrial turnarounds—think Rolls-Royce, which has gone from market pariah to market darling—tend to deliver generational wealth creation. Conveniently, Yuchai is deepening its collaboration with Rolls-Royce via the recently announced mtu Series 2000 engine partnership (link). But the real game-changer emerged yesterday.

The Setup Today:

Yesterday, CYD 0.00%↑ released a seemingly cryptic announcement regarding a potential subsidiary listing. While the market has shrugged, we believe this disclosure fundamentally reshapes the investment case. On the back of this, we have re-established a position in CYD.

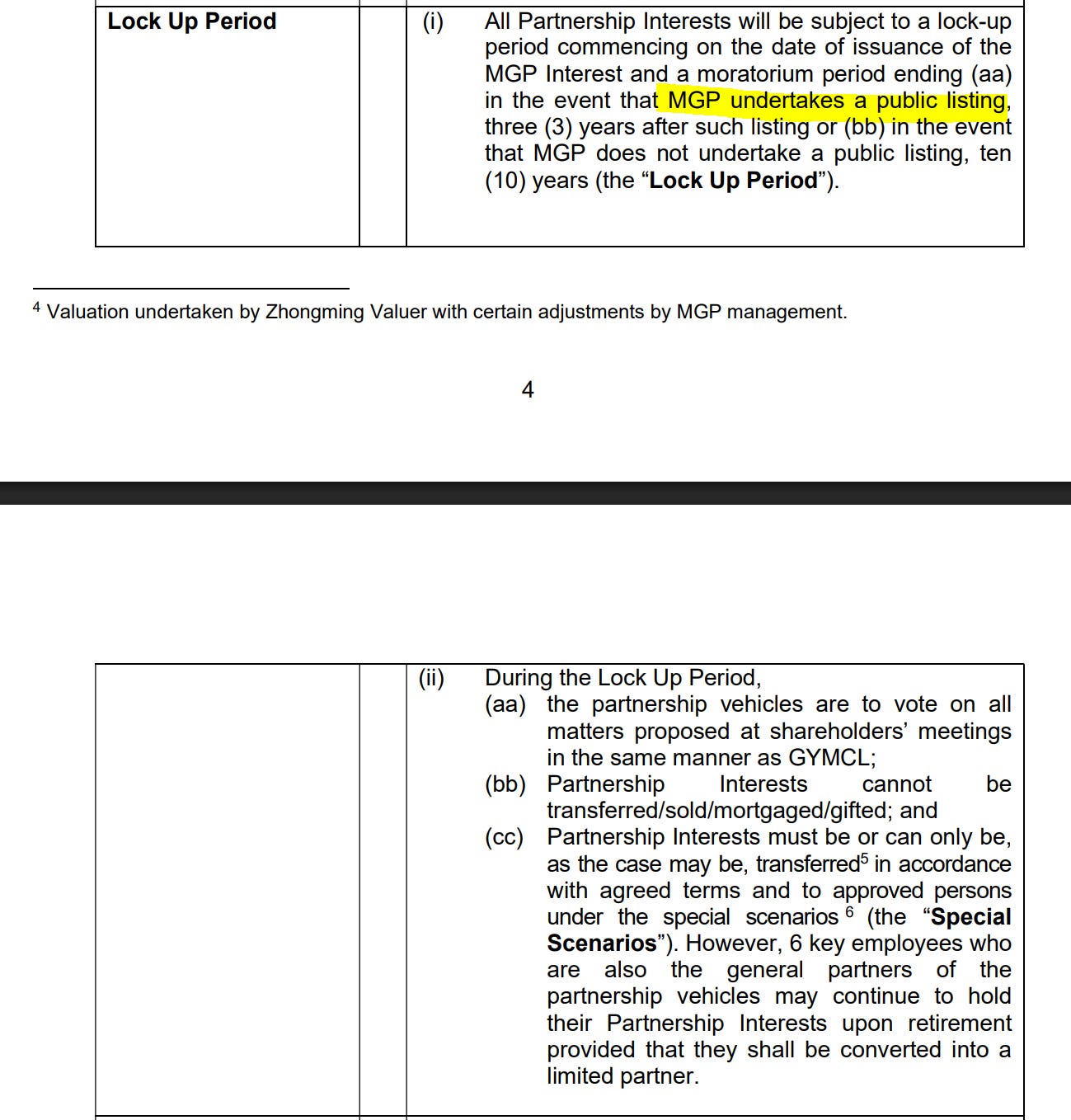

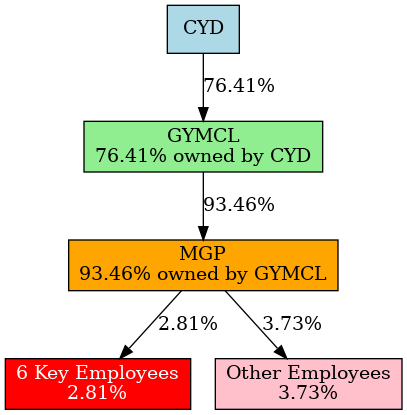

Our analysis suggests the announcement most likely refers to the potential IPO of MGP (Guangxi Yuchai Marine and Genset Power Co., Ltd)—CYD’s fast-growing data centre and genset arm. To recap: CYD owns a 76.41% stake in GYMCL, which historically owned 100% of MGP.

In mid-2024, CYD quietly completed a share incentive scheme for MGP. A 6.54% stake was transferred to employees for ¥82.88m. While absent from U.S. SEC disclosures, the crucial detail is buried in Hong Leong Asia’s SGX filings (link): unlocking of the scheme is contingent on a public listing.

The agreement highlights six key employees, whom our analysis of PRC regulatory filings suggests include both senior management and technical leadership across MGP and GYMCL. Strikingly, these six individuals contributed ~43% of the ¥82.88m capital —an unusually high personal commitment for Chinese SOE employees that signals extreme conviction and alignment.

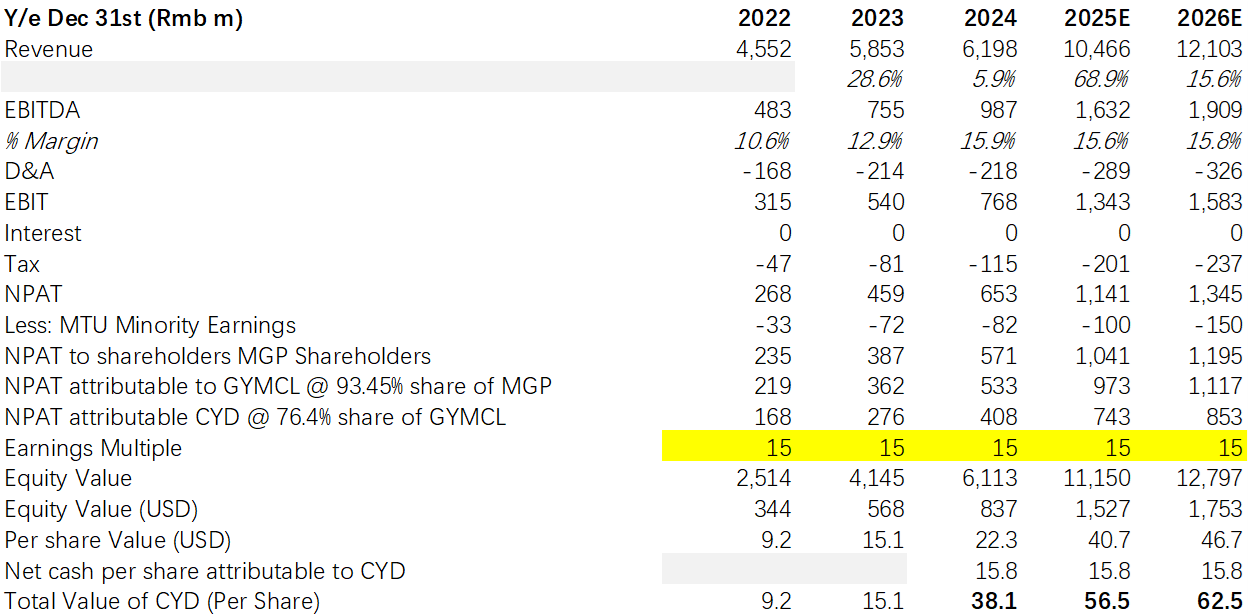

Assessing the Value of MGP

No standalone financials are currently available for MGP. However, using the same first-principles industry framework that led us to call CYD’s earnings inflection back in February, we can begin to outline the potential economics of the business.

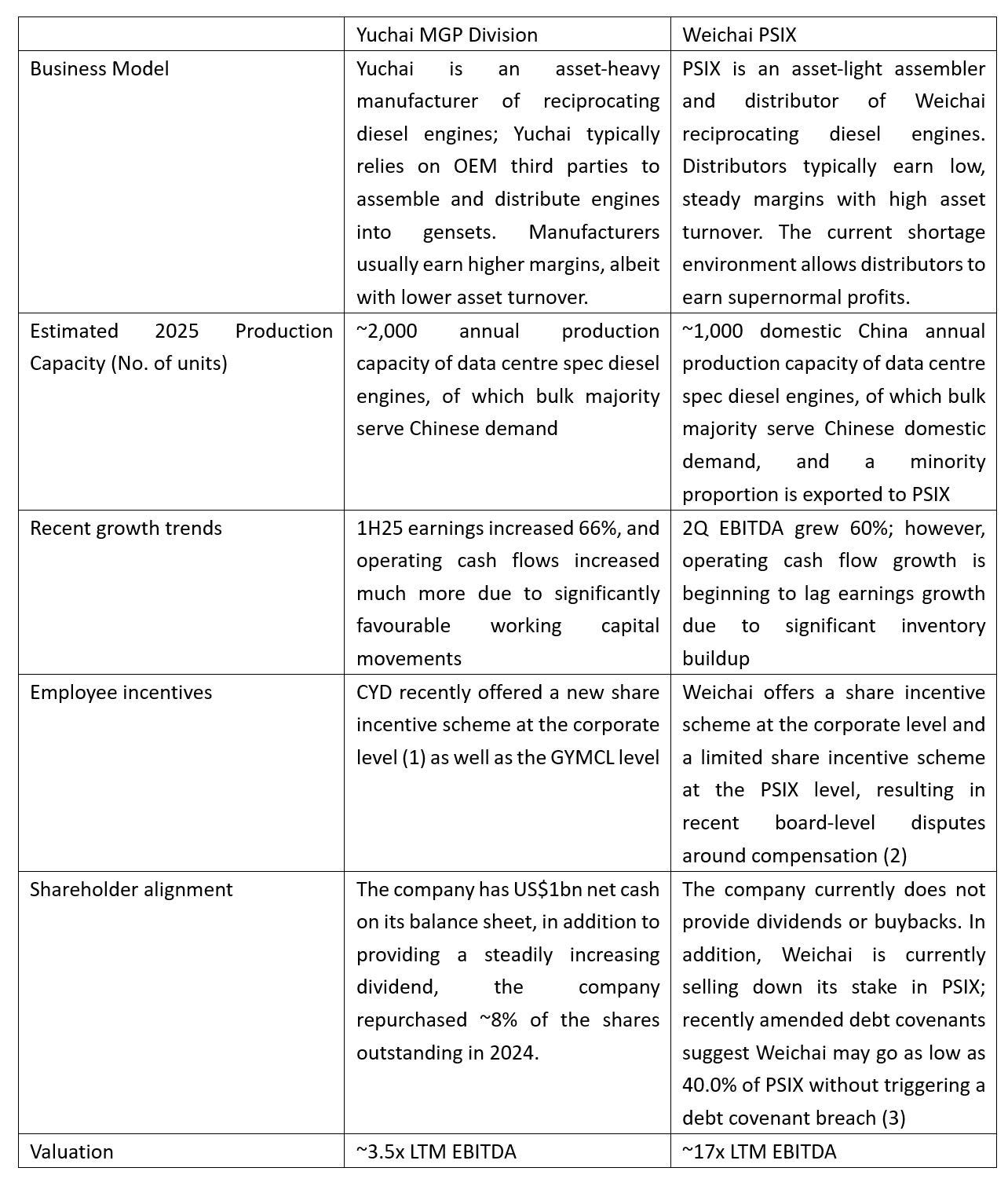

At a minimum, investors would ascribe a 15x earnings to a pure-play MGP listing. This is still a steep discount to Weichai’s China onshore marine & genset exposure (000880.SZ) or Weichai’s offshore exposure PSIX 0.00%↑ —despite MGP’s superior minority-investor alignment and higher optionality.

Peer Comparison between Yuchai MGP and Weichai PSIX

Source links

(1) CHINA YUCHAI INTERNATIONAL LIMITED 2025 EQUITY INCENTIVE PLAN

(3) Entry into a Material Definitive Agreement

Why This Matters

This announcement provides a new valuation anchor for CYD. Instead of being viewed as a commoditized diesel engine business, the market must now grapple with a high-growth subsidiary that could re-rate meaningfully upon IPO.

In short:

MGP carve-out/IPO is real (employee incentive structure confirms it).

Key insiders are aligned (significant personal financial commitment).

Valuation reframe is underway (15x earnings baseline, with upside).

Given this new setup, we view the risk/reward as highly attractive. The market has yet to price in the potential of MGP’s standalone valuation. We are positioned accordingly.

Mainland cooling stocks trade 30-50x

Great take